Emerging Opportunities in an Emerging Sector

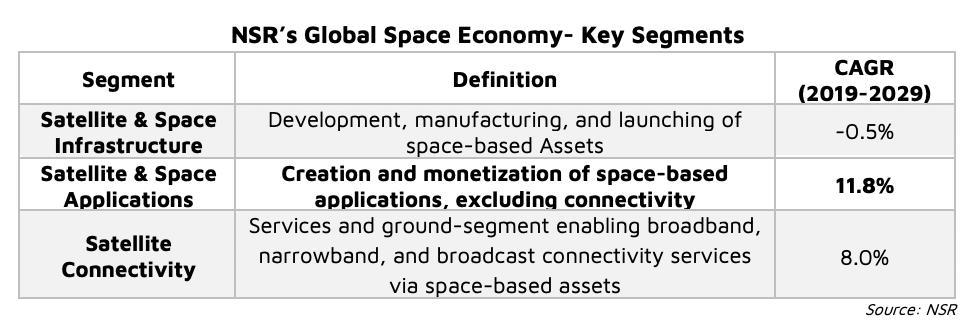

The space industry is in a period of rapid transformation, with the largest growth rates occurring in the Satellite and Space Applications segment. The recently released, NSR Global Space Economy report forecasts significant growth within this segment, representing the highest annual growth market within the decade. Albeit much smaller on an absolute revenue basis, when compared to the other segments within NSR’s report, it is easy to see the growth potential for this emerging sector.

Of particular note are emerging services-based opportunities for Big Data Analytics where new technologies are unlocking new markets. These technologies are allowing industry players access to additional use-cases, and new end-user bases thus the developing “_____ as-a-service” business models represent a significant opportunity for all.

With the present increase in satellite capacity supply and cloudification, the expanding computing capacity of the cloud has brought about numerous changes in the value and supply chains. Information and insight extraction becomes less expensive for end users, and focus shifts from building the required underlying infrastructure. Opportunity now exists to deal with the influx of Big Data and solving actual business problems. There are frequently greenfield opportunities here with little or no history of monetization in the sector. The NSR Global Space Economy report forecasts a cumulative opportunity for Satellite and Space Applications of $103B from 2020 to 2029, most of which are greenfield opportunities.

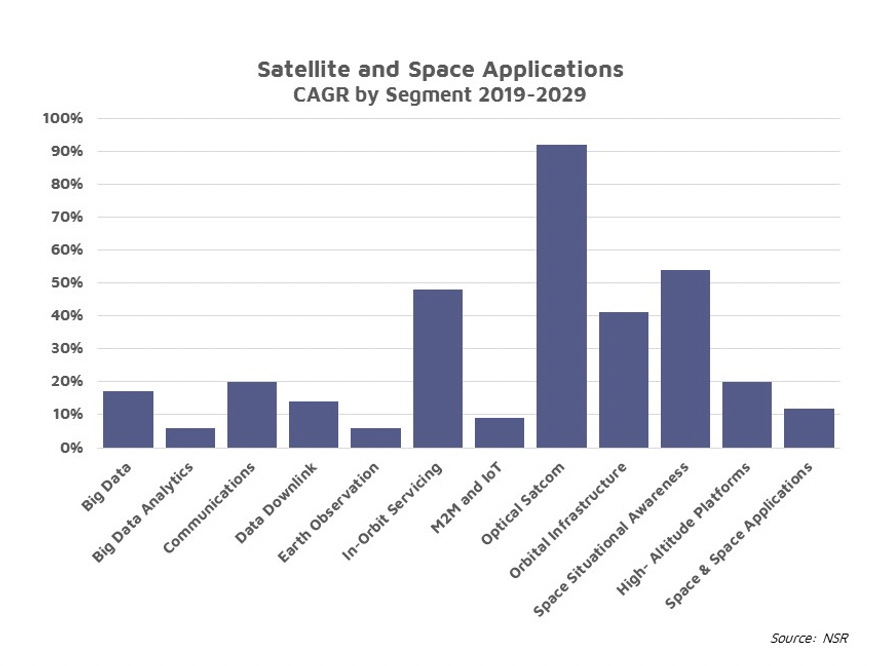

Emerging opportunities are those that, from an end user perspective, some level of uncertainty exists in the configurability of business cases, thus certain sector sub- segments represent stronger revenue opportunities in the near and medium term for new market entrants. Players must be mindful of where in the market is best to maximize ROI, and significant variance is forecast through 2029. For example, NSR projects the cumulative revenue opportunity for Optical Satcom to represent just .3% of the market’s decade-end total, while Space Situational Awareness is expected to take 4.6% of Market revenues. Recently Bluestaq announced a $280 million contract from the U.S. Space Force that will see it expand a current library of space objects, which integrates data from both commercial and government sources. Hailed as a services breakthrough, it will allow commercial space data to be made available to government/military users. The cloud-based platform offers a new integrated sourcing model by providing access to Space Situational Awareness data from multiple commercial, academic, and government groups.

These emerging opportunities for commercial engagement with government/military partners have huge potential benefits by cost sharing and decreasing the resource burden for the end user. There is a huge burden of ownership involved in completing the Big Data Analytics via satellite value chain. The move towards utilizing Non-GEO lower orbits requires the management of a significantly more complex ground infrastructure for commission and operation. With the focus placed solely on the use of cloud computing to aid customer operations, this emerging business model will reduce the CAPEX required to deploy applications. Presently, investment and increases in supply are pushing down costs and de-risking engagement with the emerging “_____ as-a-service” sector, thus increasing commercial appeal to potential government/ military end users.

Even outside the Satellite and Space Applications segment, we are seeing a proliferation of services-based business models across the technology stack. In February, this year, the Air Force Research Laboratory signed a seven-year $50.8 million contract with global Satcom company ViaSat, looking for ways to remove segment collaboration challenges and create a hybrid architecture allowing usage of commercial constellations and technologies by military customers Further to this, “_____ as-a-service” language has also become noticeably visible in recent RFIs such as the Space Force’s Proliferated LEO RFI. If potential vendors wish to tap this emerging opportunity, an in-depth understanding of customer needs is required. Security has historically been a primary concern for government/military end users wishing to engage with the commercial sector. Decreasing CAPEX and the impact of managing resource heavy ground segments are also strong motivators within this customer base. Emerging technologies such as software- defined satellites may support opportunity development in offering the ability to adjust satellites to changing needs in this rapidly evolving environment.

Bottom Line

From software-defined infrastructures to “_____ as-a-service” applications, the way humans interact with space is changing. In the next decade, the Satellite and Space Applications segment shall see the highest annual growth in the market with both technological and business innovations. Now is the time to act and adapt.

The appeal of commercial and government/military engagement is increasing as organizations work to reduce use- case challenges, thus meaning all resources become accessible. The emerging “_____ as-a-service” business model represents a significant opportunity for commercial and Gov/Mil collaboration, both vendor and end-user alike.

# # #

NSR supports equipment vendors, service providers, satellite operators, end-users, public agencies and financial institutions in their technology and business strategy assessment and planning. Please contact info@nsr.com for more information.