EO SAR Imagery Prices Limit Opportunity

In theory, radar imagery for Earth Observation is far superior to optical. With imagery capable of capturing scenes at night and penetrating clouds, SAR overcomes many challenges inherent to imaging the Earth with passive optical sensors.

It would seem that investors are banking on these capabilities for increased coverage and insights from SAR imagery given recent funding announcements from Iceye, and Ursa Space. Revisit and analytics are cited as key drivers, with many working to develop algorithms for analyzing and monitoring assets, even across traditional vertical markets.

However, in practice, SAR revenues and market penetration remain relatively low, and NSR does not expect radar to overtake or greatly outpace the optical opportunity anytime soon.

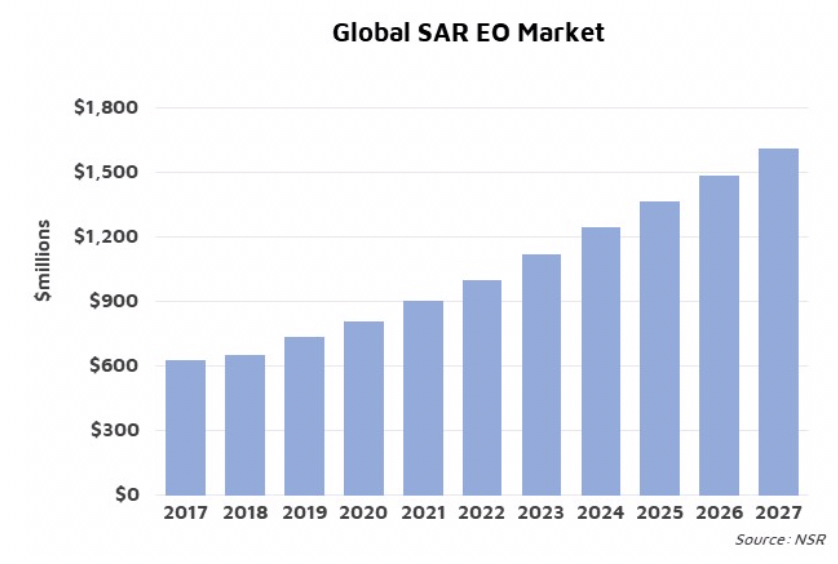

NSR’s Satellite-Based Earth Observation, 10th Edition report forecasts revenues from the sale of SAR products to grow to over $1.6B by 2027, at a CAGR of 9.8%. However, given that optical revenues are expected to exceed $5B in the same timeframe, one must ask what is restraining SAR markets?

Primarily, optical imagery is highly competitive, with more supply, lower prices, and more options available. Furthermore, the human eye and subsequent imagery processing were developed for optical scenes, with most finding SAR imagery too complicated or expensive to consider.

When examining EO data adoption, one must consider resolution, revisit, and pricing as key customer-decision factors.

Resolution

Most of the current demand for SAR imagery lies in applications for wide-area monitoring or highly-precise interferometry, both of which can be accommodated by medium resolution (MR) SAR data. Freely available data from the Copernicus program undercuts the commercial opportunity here, as customers remain satisfied with the quality, resolution, and revisit of the EC Sentinel satellites that are offered through this program. This has lowered the barrier to entry for downstream (Information Products, Big Data analytics) players, creating more opportunity, yet at the expense of revenues generated from SAR data sales.

Revisit

Current SAR use cases do not necessitate a high revisit rate. While the industry has become increasingly interested in high revisit, several technological and economical factors have limited the SAR commercial opportunity. As such, most customers remain satisfied with Sentinel’s 6 to 12-day revisit. Data analytics may eventually require higher revisit SAR data, such as Ursa Space’s oil manufacturing index, but for now, this opportunity remains small.

Pricing

The high costs associated with the procurement and processing of SAR imagery have long restrained the market, leaving Defense & Intelligence, Public Authorities, and high-end Energy customers as those most able to afford it. SAR payloads are generally more expensive and drive higher pricing for tasked imagery to provide reasonable returns on the satellite investment. High resolution imagery, growing in demand, will remain expensive, especially when next generation systems come online to compete with incumbent SAR constellations.

Bottom Line

There is great opportunity for SAR data and services on the market; the key is knowing your customers. Players in this space must be mindful of free MR SAR data, and the fewer use cases associated with radar imagery. Revisit and resolution are growing in importance, but not dramatically, for niche customers in few market applications. In the end, price is the factor influencing SAR decision-making, and customers will trade off against resolution and revisit to meet their budgets, thus putting a cap on the opportunity going forward.