Faster Flow for Satellite Big Data Pipes

The global satellite big data industry has come a long way during the latest wave in the emerging space industry. More than 180 EO companies have been founded over the last 20 years, with a majority of them being downstream software and platform providers. Close to $700 million has been invested in this analytics segment over the same time frame, particularly in emerging space companies.

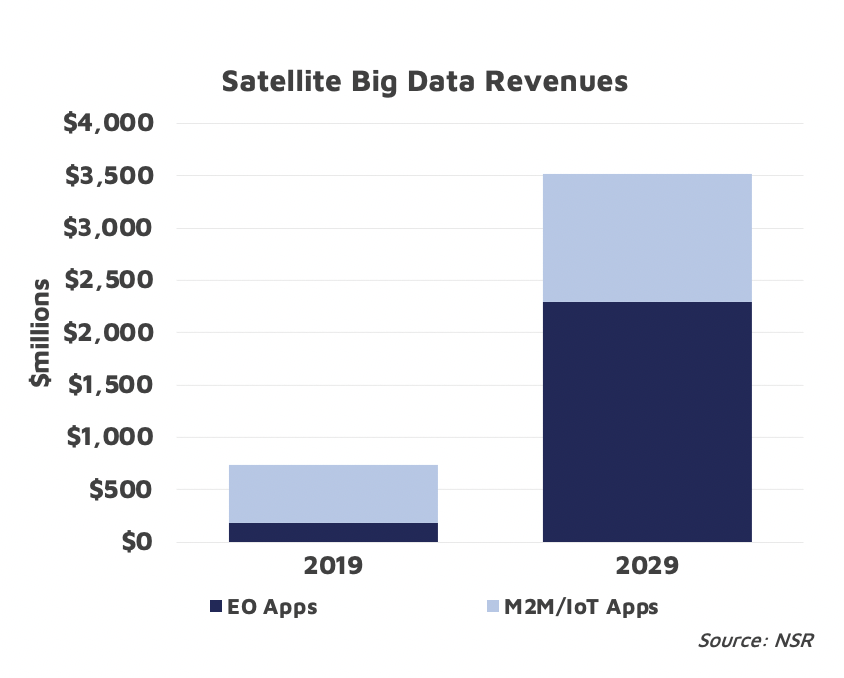

This is a growing sector: we have seen M&As and exits in recent years, while others have moved towards vertical/horizontal integration. NSR’s Big Data via Satellite, 4th Edition research report forecasts a cumulative opportunity of over $20.7 billion through the 2019-2029 period for satellite big data. Yet, the market remains constrained, and bottlenecks remain to be solved. Challenges need to be overcome before the market can flow freely to deliver on its promise.

Ease of Use: Standards & ARD

Standards in an industry validate the capabilities of a product and establish its processes and systems across providers. With the use of satellite big data increasing rapidly, and moreover, a growing supply dynamic as more EO satellites are planned to go into orbit, there are a number of derived datasets from various sources made available. Additionally, cloud-based API access, web-based applications and user platforms for EO have been developed by numerous public organizations and commercial companies, leading to data storage and inconsistency problems that further add a layer of complexity in the data preparation stage.

Allowing users to analyze data without worrying about pre-processing will be a key development across the industry going forward. Multiple satellite operators already provide Analysis Ready Data (ARD) specific to their sensors, but normalizing cross-sensor ARD is essential for greater adoption.

As higher volume datasets such as SAR and hyperspectral make their foray into the satellite industry, it becomes imperative for larger data pipes (via high frequency RF/optical links) and timely, autonomously scheduled links (via SDN, relay systems, virtualized ground etc.) at low latency. Such data then needs to be made shareable and interoperable, for real ease of use by the end customer.

Ease of Access: Marketplaces & Platforms

In addition to ease of use, another traditional bottleneck is the accessibility to data. Satellite operators and service providers are now shifting away from a low-volume transactional mode of operations into high volume subscriptions via platform-access to satellite data.

With the high growth in analytics providers, there is a growing middle layer in the satellite data value chain, that of marketplaces and platforms that collate various sources of satellite data and processing algorithms. They enable users by hiding complex data sourcing processes behind a single access API. By integrating continuous satellite monitoring and a pay-as-you-use model similar to that of cloud providers, such platforms help to unlock a larger addressable market looking to use high quality satellite data at scale.

The Bottom Line

The satellite big data sector is on the cusp of historical growth – the adoption of cloud-native geoprocessing, web-based tools, the promise of high-volume data subscriptions (à la Netflix), increasing interest in low latency data downlink and greater digitalization in its target markets.

However, growth as promised will depend on ensuring ease of use and access of this data: whether by establishing cross-industry standards, providing on-demand ARD, or by simplifying the downstream satellite data toolchain so that big data flows faster.