GHG on the Minds of Space Sector ESG Strategies

While achieving ESG goals offer potential benefits for Space & Satellite organizations, the required data key to meeting ESG goals also represents a substantial revenue opportunity for the space industry. This last year saw a number of ESG and satellite related partnerships such as Planet Labs partnership with Moody’s ESG work or ICEYE’s work towards Insurance industry ESG risk activity as ESG based regulatory activity rose. More importantly, as the march towards mandatory Greenhouse Gas (GHG) emission reporting continues across the world, how should space sector players consider their own roles or market opportunities? In short, as the space industry focuses on the benefits their products and services can provide across various industries, it should look at itself as a valid (and growing) part of the total addressable market opportunity.

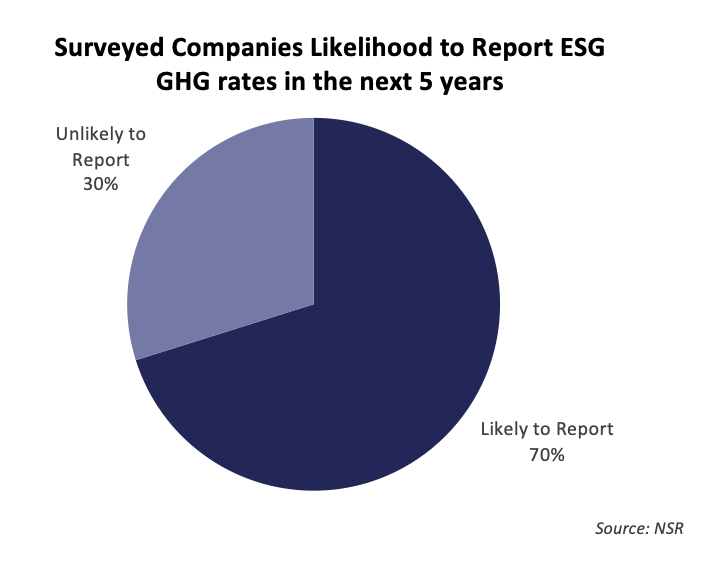

An analysis of NSR’s Space ESG Assessment surveyed companies sees at least 70% of organizations positioned to likely need to meet at least one regulatory requirement to report GHG levels within the next 5 years. With the right impact and price-point, NSR’s Space ESG Assessment notes Earth Observation is positioned for significant revenue capture potential as the Space & Satellite industry takes its place in the emission ESG TAM. As part of this study, NSR explored the various published ESG strategies across a group of space industry players. Within these companies, Environmental-focused ESG objectives were identified. Most focused on meeting regulatory or social pressures for carbon-neutrality, but all could leverage advances in space-based analytics to help measure and monitor these goals.

Already a core component of ESG framework development and standards reporting, global emissions monitoring is moving passed being a recommendation into the mandatory reporting field. Reporting requires data and the Space & Satellite industry is well situated to benefit from this opportunity, both as a service provider and end-user.

The Opportunity

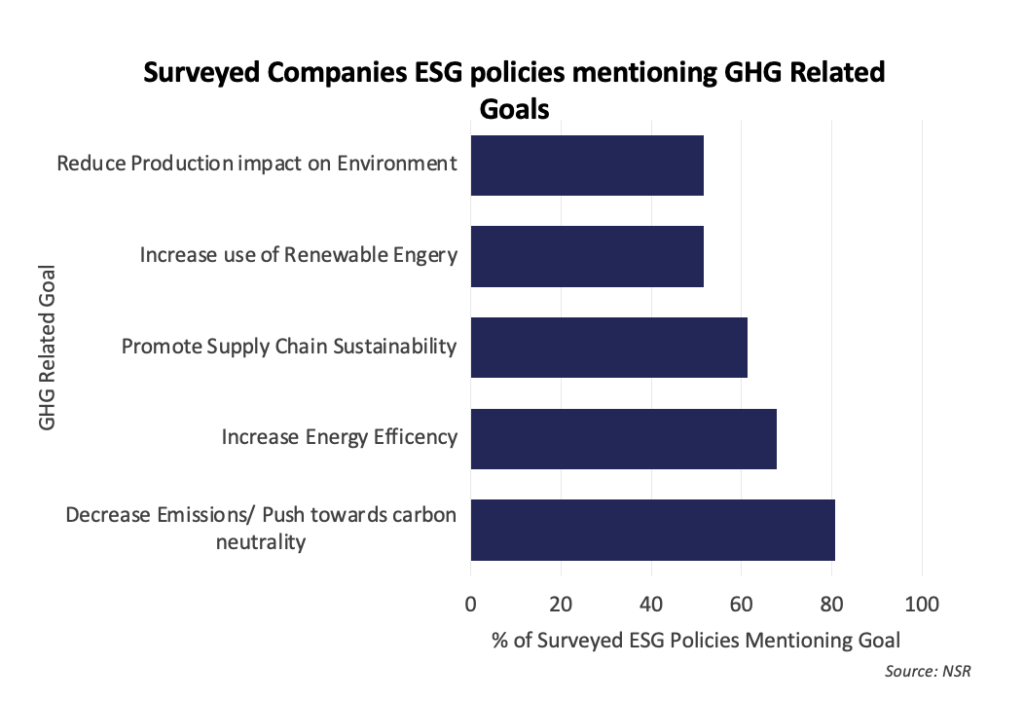

While current reporting has utilized known standards, reported emission statistics, and historic data- a market is now forming for satellites to step in. With the recent Earth Observation data supply expansion pushing depreciation in pricing (see NSR’s Satellite-Based Earth Observation, 14th Edition for further information on EO activity), satellite data is becoming more accessible to newer and smaller players. Players are already looking at strategies to address GHG risks (see below chart of surveyed company current activity).

Expect interest in this field to continue to rise. As EO proves its use, providers should ready themselves to communicate and demonstrate the full spectrum of satellite offerings. For at least some players, this will be a new area of industrial engagement and service provider advocacy will be key. Promotion of services such as the ability to validate technological emissions calculations, hone seasonal variations numbers (particularly useful for energy and land use) and provide precision information as newer technology come online will be essential. Companies need to know about new service options if they are to purchase them.

The Bottom Line

EO service providers are about to see a total addressable market growth spurt as the Space & Satellite sector moves to respond to ESG regulatory developments. As more space-focused companies fall under reporting requirements, EO providers should also look within the value-chain for opportunities to offer products and services.