Gov & Mil Markets: An Evolving Capacity Acquisition Paradigm

As the satellite industry and the U.S. Government start to kick things off for a New Year, planners continue the process of creating the next-generation of Gov & Mil network designs. With a renewed focus on the importance of space to executing the national security missions of countries across the globe – and ‘assured access’ to space-based connectivity not a guarantee, where does that leave the role of industry and commercially-focused offerings?

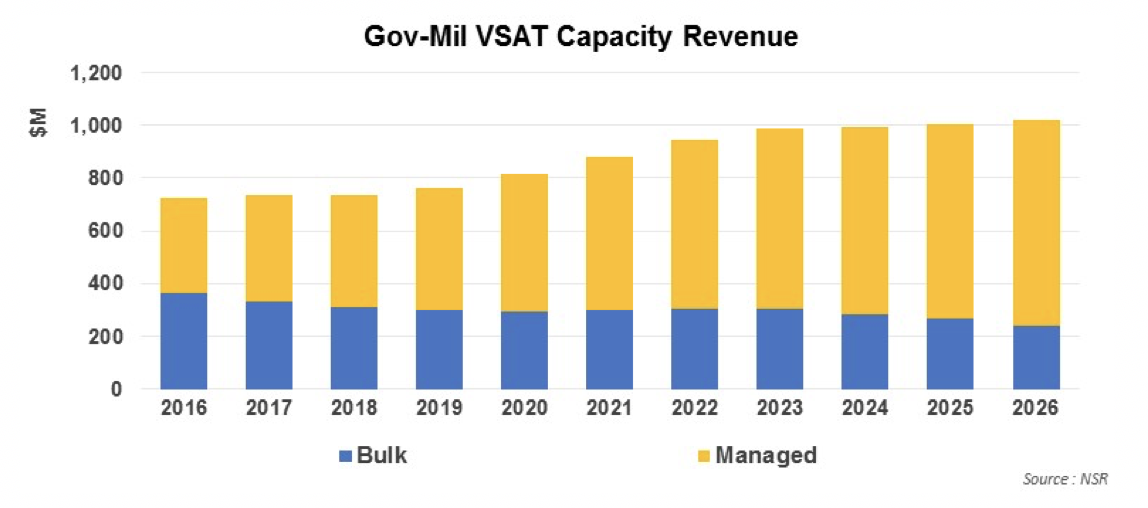

According to NSR’s Government and Military Satellite Communications, 14th Edition report, the satcom industry is entering a period of renewed growth in Gov & Mil Markets. Focused on ‘connecting things that move’, there is a clear path for commercial-sourced offerings to enable the missions of Governments and Militaries across the world such as ViaSat’s award for Air Force One and other Senior Leadership Airframes. With VSAT Capacity Revenues expected to exceed $1 Billion by 2026 for Gov & Mil Markets, HTS on the horizon and an increasingly complex operations environment for Gov & Mil end-users, network designs and operational flexibility/complexity will only increase over the next ten years. Following that growth, new connectivity technologies in GEO and Non-GEO will enter the supply picture and become a (slow) growth factor in an ever-shifting marketplace.

With HTS adoption lagging behind the commercially-equivalent markets, Gov & Mil End-Users remain constrained in deploying new equipment to take advantage of new technologies available in the market today. While those constraints will naturally solve themselves through the evolution of platforms, (especially in the UAS markets where new airframes will be ‘HTS-ready’ from day 1), Gov & Mil users will be strong consumers of legacy FSS capacity – just at a time when satellite operators continue to face monetization strategy questions around ‘still good’ legacy assets. Just how much FSS capacity will be available to Gov & Mil markets remains to be seen, but as hot-spots such as the Korean Peninsula, Southern Africa, or ongoing struggles in the Middle East are any indication, bandwidth demand will continue to be limited almost entirely by budgets and compatibility issues.

Growth is on the horizon for Gov & Mil markets – especially bandwidth demand. Yet, just as FSS connectivity will still remain a core component of the market – acquisition through bulk-leasing of capacity remains a strong segment of the market. Although declining capacity pricing will reduce its overall share in the capacity revenue mix, falling prices will allow end-users to continue to connect legacy or near end-of-life assets with greater capabilities and throughputs – enabling better lifecycle economics as military planners look to acquire next-gen manned and unmanned platforms. Just as Gov & Mil planners in key markets settle on a future architecture for their own proprietary capacity, acquiring ‘raw’ or ‘lightly managed’ capacity from mostly satellite operators will continue to enable a sub-set of demand. These applications will be varied across the spectrum of platforms and applications, whose connectivity requirements continue to increase. With more spending on the horizon for proprietary capacity acquisition programs (‘WGS 2.0’, ‘Skynet 6’, etc.), bulk leasing will continue to fill an important middle ground between terminals and platforms that live within fully government-owned/managed/controlled environments and those fully-outsourced in a managed service model.

Bottom Line

The near-future for Gov & Mil markets is transition – transition from FSS to HTS, legacy MILSATCOM systems to next-gen capabilities, and from ‘business as usual’ to commercial best-practices. Overall, evolving threats are changing the operational landscape. New commercial and proprietary capabilities are helping to meet those challenges – and the acquisition framework linking bespoke military capacity with commercial capabilities continues to evolve.