High Altitude Platforms: Loony No More?

Earlier this month, Loon announced the start of commercial use of its balloon infrastructure to provide communications service in Kenya. This comes fast on the heels of a spell of announcements through the year, from the formation of an alliance dedicated to the development of the HAPS ecosystem to partnerships between stratospheric players and major telecom operators. Notwithstanding project failures and major mishaps in recent years, High Altitude Platforms have remained an emerging market even in the wake of the COVID-19 pandemic. What is driving this interest, and why might the current wave of HAPs-related activity be any different from those of previous decades?

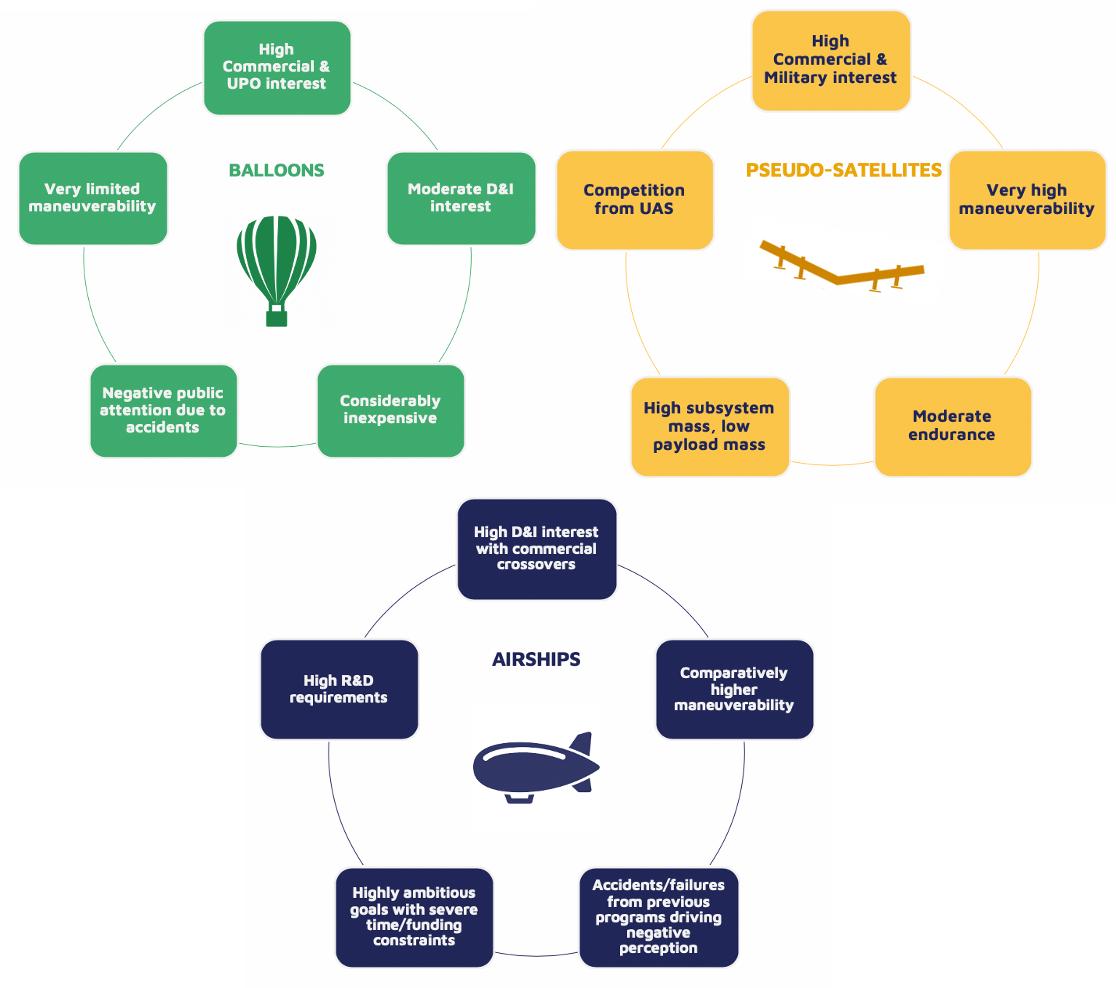

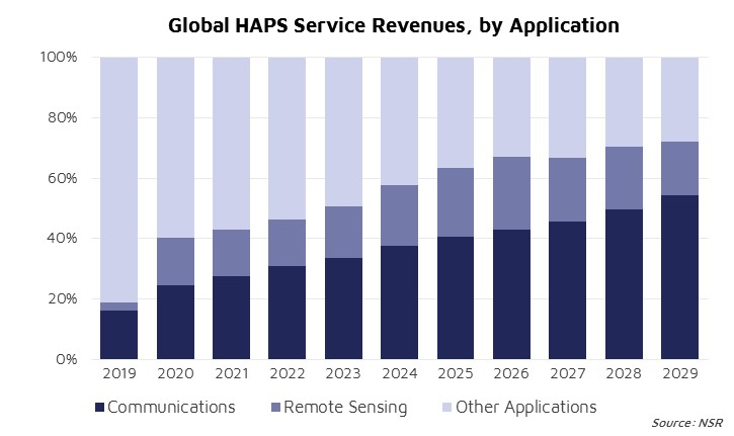

NSR’s High Altitude Platforms (HAPs), 4th Edition report estimates just over 40 HAPs programs presently active at various stages of development, and forecasts a service revenue opportunity of nearly US $470 million by 2029. Stratospheric balloons are the most mature market and a major driver here, given their long history of success in the science and research communities and the involvement of major commercial players. Meanwhile, investments and resources from aerospace incumbents and innovations in the UAS segment have spearheaded developments in fixed-wing solar powered pseudo-satellites. The comparatively more expensive and R&D intensive airships are seen to be largely in the developmental/testing phase.

Despite a dip in 2020 due to COVID-19 related restrictions, the global HAPs industry is expected to grow steadily. Funding and logistics-related issues are key areas impacted by the pandemic, leading to launch delays and increased lead times. The market is expected to recover in the near-term, as supply chains of HAPs manufacturers and launch plans of HAPs operators catch up to pre-COVID schedules. In the longer run, technological transformation is projected to drive growth and eventually accelerate the revenue opportunity. This will be driven by the need for improved station-keeping for balloons, longer dwell times for pseudo-satellites and the development of cost-effective airship prototypes.

Various stakeholders in the industry are fast recognizing the potential for HAPs as a quickly deployable alternative/complement to existing satellite and terrestrial networks for communications. While a few telecom players continue to remain skeptical about the effectiveness of such projects (and rightly so), achieving buy-in for the infrastructure-as-a-service model from other major traditional telcos lays a foundation for HAPs players to focus efforts on developing new business models for the future. Services are forecast to be rolled out in partnership with mobile network operators, with balloons and pseudo-satellite platforms being utilized as mobile cell-towers in the sky in support of MNO network expansion strategies.

We may also see the lease of HAPs to potential remote sensing/ISR service providers/payload manufacturers. HAPs are generally well suited for intelligence and reconnaissance, characterized by persistent, long-term surveillance over an area of interest. However, a robust regulatory environment and partner ecosystem will be critical if progress is to be made, and project closures are to be avoided.

The Bottom Line

The December 2015 landing of a Falcon 9 booster stage marked a turning point in the commercial space launch industry, considering that such landings are now nearly par for the course. Perhaps it is a little too early yet to report a similar evolution in the HAPs industry: from outrageous and “loony” at the outset to an industry standard in a few years’ time.

Nevertheless, chasing the dream of Internet and data from the stratosphere now does not sound as outlandish as it once was. Given the right moves (addressing standardization and regulatory concerns in particular), newer business models are expected to be introduced into the market in the growth phase. Market adoption across comms, remote sensing and other applications in the long run will then accelerate development, driving both the HAPs manufacturing and service revenue prospects.