Impact of Economic Slowdown on VSAT Market

2022 had been a difficult year for the world owing to the geopolitical challenges such as the Russia-Ukraine conflict, U.S.-China relationship, increase in food and energy prices, continued increase in bank interest rates, and others. It is estimated that the global inflation rate grew by ~ 8.8% in the year 2022. These have led to massive layoffs across the globe. Major ones include Meta reducing its manpower strength by 13%, Amazon cutting down 18,000 jobs, Google firing 10,000 employees, and Microsoft to lay off 11,000 employees.

So, does the scenario change in 2023? Will 2023 be a better year than 2022? The answer is NO. 2023 is expected to witness further economic slowdown across the globe. According to the International Monetary Fund, global growth is estimated to decline from 3.2% in 2022 to 2.7% in 2023. How do these macroeconomic factors impact the Enterprise VSAT, and the Consumer Broadband markets, as estimated in the NSR’s VSAT & Broadband Satellite Markets, 21st Edition report?

Resistance to Market Forces

The Space and Satellite Communication (Satcom) industry is uniquely positioned and hence has relatively different or resistive impact, primarily due to three factors –

- longer product development & service roll-out lead time,

- wide range of target markets, and

- significant financing or business from government institutions.

However, it would be incorrect to say that the Satcom and the Fixed VSAT market will be completely immune to the ongoing economic slowdown. As new capacity in Non-GEO and GEO are entering the market to target new geographies and customer groups, these macro-economic factors will be a key constraint or driver depending on the application.

If we look at the industry’s behavior during COVID-19, on one hand there was a steep decline in demand in mobility market segments but at the same time, industry stakeholders witnessed demand ramp-up in Backhaul and Social Inclusion. And this led to the overall industry resistance to revenue decline as the industry reported only a low single-digit overall decline. Hence, it becomes critical to analyze the market by applications as the Fixed VSAT market covers a wide range of Enterprise and Consumer class end users.

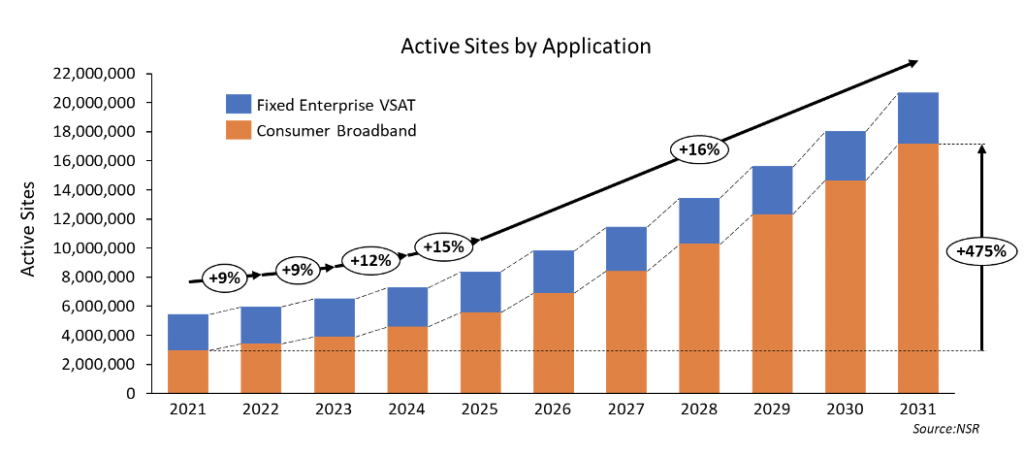

According to NSR’s VSAT & Broadband Satellite Market, 21st Edition report, the Enterprise segment is estimated to witness moderate 3.6% CAGR growth in in-service units, whereas the Consumer Broadband use case is forecasted to grow at an astounding 19% CAGR, during 2021-2031. However, the projected growth is not expected to be linear throughout the decade. In the near term, clearly macroeconomic factors among many other factors, such as capacity supply, competition, regulatory challenges, pricing, etc. will play important roles in determining the future of the satcom fixed VSAT market. To understand the detailed impact of the economic slowdown, it is important to analyze the market from both end-user and industry stakeholders’ perspectives.

Impact of End-User Behavior

On the Enterprise VSAT side, end users will look for reducing their spending and, there will be some of the sites that will witness closure. This will result in an increase in churn. The positive of this slowdown is that end-users will look for the most cost-effective and efficient processes resulting in increased capacity demand for the enterprise customers.

Government programs focusing on bridging the digital divide will continue to remain the key market driver for both addition of sites and revenues. On the consumer broadband side, with rising inflation and massive lay-offs – the average disposable income of the addressable market will take a hit. However, the demand sphere for the segment is so large that it is currently supply constrained.

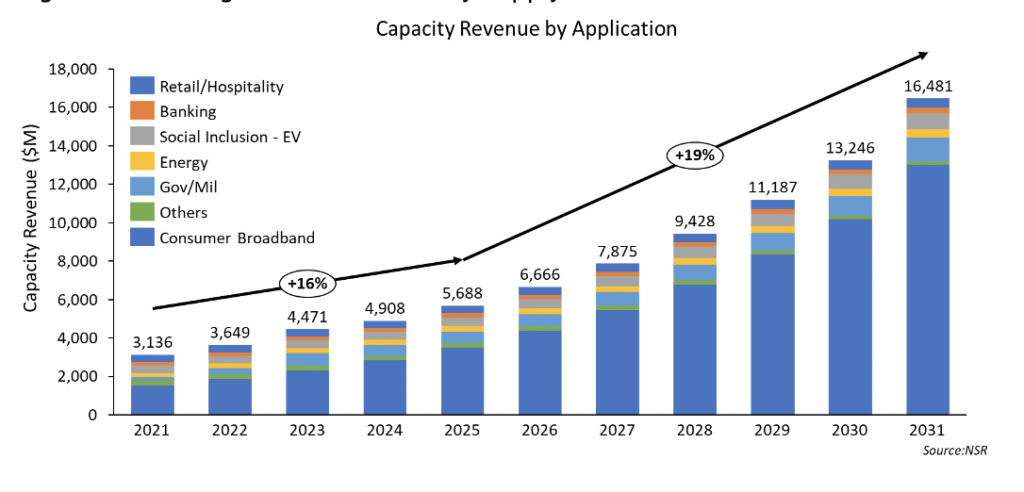

The economic impact on the segment is estimated not to be very significant in the near term, from the end user perspective. NSR estimates the cumulative 10-year capacity revenue opportunity for the Fixed VSAT market is $86.7 Billion. Consumer Broadband will be the major contributor to this revenue opportunity with a 69% revenue share.

Starlink, ViaSat and Hughes will be the major players in the segment. Despite the flat number of in-service units, the Gov/Mil segment is expected to witness an accelerated ramp-up in bandwidth per site demand. As a result, the segment is expected to witness an astounding 24.3% growth during 2021-2031. Also, the segment will show relative resistance to the ongoing economic slowdown in the near-term.

Impact on Industry Stakeholders

Supply is one of the top variables that will determine pricing, demand capture and overall revenue generation. Most stakeholders have invested in HTS capacity to target a varied range of end-users and difficult geographies. As an impact of COVID-19, key players such as ViaSat, Telesat, Hughes, etc. witnessed delays in their program schedule. Significant portions of these programs are funded by investors or financial institutions’ capital either in exchange of equity or as debt. In the ongoing economic scenarios, the programs will become more costly as interest rates increase and/or programs get delayed. Also, equity valuation and access to investors’ capital will also not be at attractive or most favorable terms, especially in the near-term.

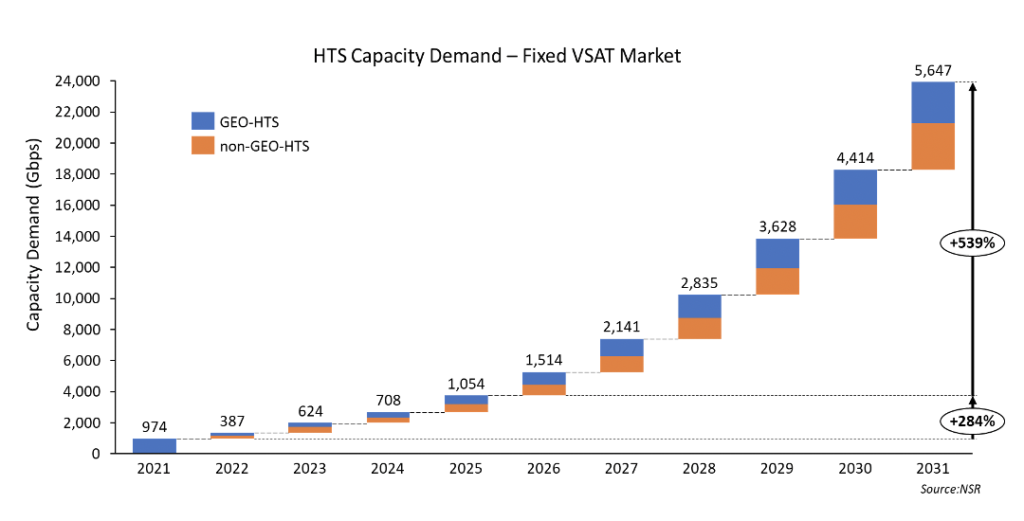

Despite massive demand across applications such as Social Inclusion, Consumer Broadband and Gov/Mil segments, demand capture growth will be restricted in the near future. However, long term as greater price control over the product and services is achieved in the ecosystem, the unlocking of demand elasticities will be greater. The estimated capacity price for applications such as Consumer Broadband will reach close to $50/Mbps/Month in the latter part of the ongoing decade. Despite the massive buzz for Non-GEO services, demand capture by GEO capacity will be in sync with the Non-GEO capture. The total HTS demand capture will reach close to 24 Tbps by 2031.

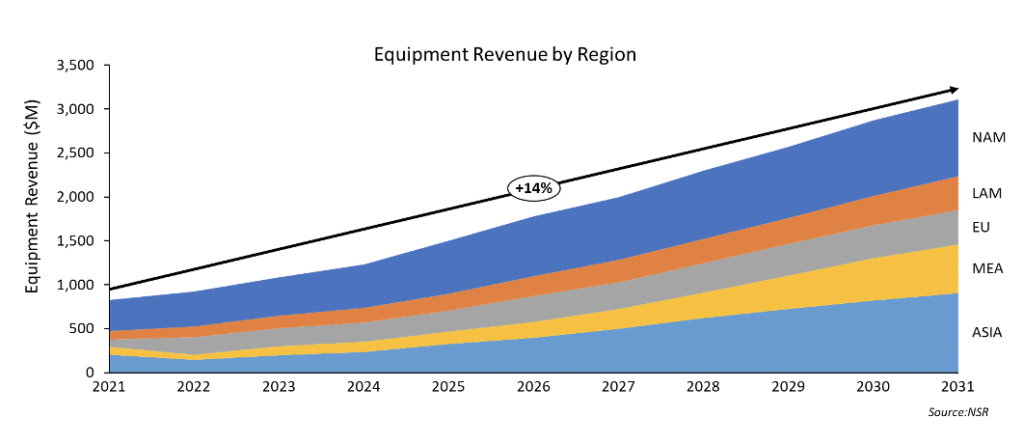

Equipment shipments and revenues are likewise key variables that will determine industry growth. Major players are working on the advancements of ground systems to target future markets. Players such as Gilat, ST Engineering and Hughes have partnered with various GEO and Non-GEO players. The key focus is to improve bandwidth capability and enable multi-orbit solutions. Typically, the R&D budget is one of the first to witness reductions during constrained financial situations. NSR expects the economic slowdown to decelerate some of the R&D pace, especially for flat panel antennas. NSR estimates equipment revenues to grow at CAGR 14% during 2021-2031. Clearly, the growth slope will remain flatter in the near-term, owing to economic challenges as one of the major governing factors. Regionally, NAM (North America) will remain the major market, but Asia will evolve as the fastest growing market during the assessment period. For the economic slowdown and the critical impact on the Fixed VSAT market, NAM (North America) & Europe will be the two epicenters and impacts will gradually propagate to other regions.

The Bottom Line

Continued economic slowdown is inevitable. As per industry economists, the ongoing slowdown may lead to recession as well. Undoubtedly, the Space & Satcom industry is not to remain immune to this macroeconomic situation. But as compared to other industries, the Satcom & Fixed VSAT market is well positioned to navigate through this challenging environment. This is as a result of the last decade where space stakeholders focused on improving cost per Mbps, expanding to new geographies, and becoming leaner by consolidating vertically and horizontally. Considering key performance indicators, such as in-service units, capacity demand, capacity revenues and equipment revenues, overall, the industry will continue on the growth track in the near and long term. However, the growth pace will be restricted for the next 2 years. This analysis does not ascertain that all the industry stakeholders will do well, but yes, some will if they focus on the following key areas:

- cost optimization,

- revenue growth of the top products & services in their portfolio,

- achieving timely supply,

- building robust supply chain,

- targeting government driven programs, and

- executing strategies to a healthier bottom line – not just the top line.