In-Orbit Servicing: Stepping up to the Challenge?

Last month, Spaceflight Inc. launched 16 payloads on board its Orbital Transfer Vehicle (OTV), Sherpa-FX-1 on a SpaceX rocket to deliver them to a precise orbits, a first in LEO SSO orbit. And soon, a 2nd MEV from Northrop Grumman will latch on the Intelsat 10-02, solidifying the In-Orbit Servicing Market for Life Extension missions so operators can continue utilizing their assets longer than the planned 15 years lifetime.

These are a few examples of the budding In-Orbit Servicing (IoS) market dynamics taking hold. However, as launch and manufacturing continues to improve in capability, the satellite industry remains torn between investment in replacements, flying them longer in inclined orbit versus improved flexibility once on-orbit. With NSR forecasting over 12,000 satellites to be launched in the next decade, it begs the question, “Is there room for in-orbit services, and if so, where?”

Positioning IoS for the Future

The inflection point as to the number of satellites reaching end-of-life is likely to increase the demand for IoS services over the next decade, as many customers in GEO need to decide to either replace or extend the life of their satellites. Furthermore, the need for insertion of constellations into their proper orbit is seeing increased interest, as these to go up in record numbers on low-cost rideshare to a non-optimized orbit, and offer a new breed of players an opportunity to offer ‘last-mile’ solutions, especially in Low Earth Orbit.

And COVID-19 disruptions generally did not influence this new and emerging space activity. Indeed, many of the missions from players are still scheduled to go ahead in 2021 and many will be first movers in the IoS market.

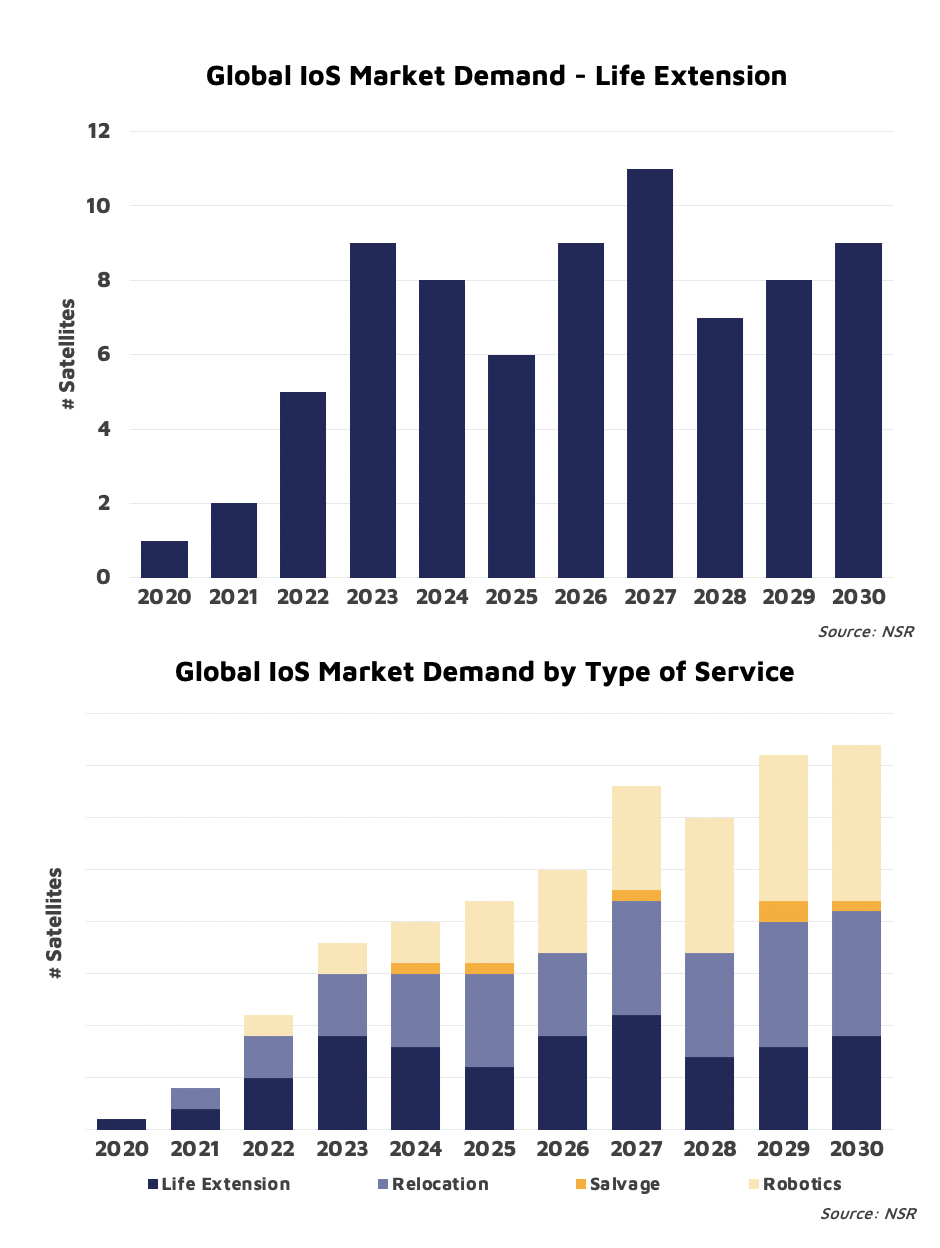

NSR’s In-orbit Servicing & Space Situational Awareness Markets, 4th Edition report forecasts demand for GEO Life Extension mission to grow to 75 by 2030, representing a cumulative market opportunity of $3.2B. This is the single largest revenue generating IoS activity in the next decade. Continued demonstrations through missions such as MEV support the premise of extending revenues through in-orbit services, offering the flexibility for deferring CAPEX and ensuring customer retention through continued service. Indeed, these demonstrations have attracted a positive response and has been a morale-booster to the more than 50 players active in the market.

Over 230 satellites are expected to be serviced during the forecast period, with government & military customers favoring robotics & relocation for both GEO & Non-GEO. Life extension currently leads but, as the market diversifies, we will see more demand for relocation, and robotics over the forecast period.

Bullish with Gaps

The IoS value proposition continues to develop, offering operators a CAPEX holiday on satellite reorders, provide customers with precision orbital insertion, and eventually, robotic missions to inspect, assist, and eventually modify assets. Technological advances are helping the IoS servicing market grow, but these efforts are facing bottlenecks with advancements and competition from improving launch and manufacturing services, and lack of clear technical and safe operation standards.

So for IoS services to overcome this hurdle, many players are working with governments to establish standards, and offer competitive prices through diversified services and products. Additionally, IoS providers are working to establish framework for safe operations, developing hardware standards utilized throughout the value chain. However, the unknown remains whether service providers are open to flexible business cases with drivers like decreasing cost per mission, flexible mission architectures, successful mission guarantee, pivoting from service driven business model, and further expanding it to end-to-end services.

NSR forecasts IoS players will only be able to serve 9% of the addressable market over the next decade, as restraints on the market are expected to be the slow technology development, and the confidence in capabilities with much of the focus concentrating on GEO and government/military customers. As technology and service offering develop, in-orbit services are expected to cater to the market more competitively, growing quickly and resulting in a $6.2 billion cumulative revenue opportunity by 2030.

Bottom Line

With the industry moving towards addressing demand of custom services at a competitive price, IoS service providers must find new ways to attract clients. It is becoming vital to diversify the IoS applications offerings and to collaborate on sharing best practices, developing technical and safety standards, and establishing clear expectations of outer-space operations for this market.

However, just like any new market, there remain gaps in the industry, from the technological feasibility and safety standards to the service offering’s marketability, while remaining competitive and, ultimately, becoming a cost-and-effort saving part of the value chain.