Infrastructure in the Stratosphere

Recent High-Altitude Platforms (HAPs) related development is driving emergent markets in telecom and remote sensing, but such excitement is nothing new. Several programs from the last two decades alone promised the use of stratospheric platforms for comms and observation, most of which fell through in the end. However, recent investments and subsequent mission successes from commercial players such as Alphabet and Airbus have injected a fresh wave of hope. In recent months, HAPSMobile announced a joint research project to provide Internet connectivity in Rwanda, while Near Space Labs ramped up on deployments of its remote sensing platform during the pandemic. Meanwhile, the HAPSAlliance continues to welcome new partners.

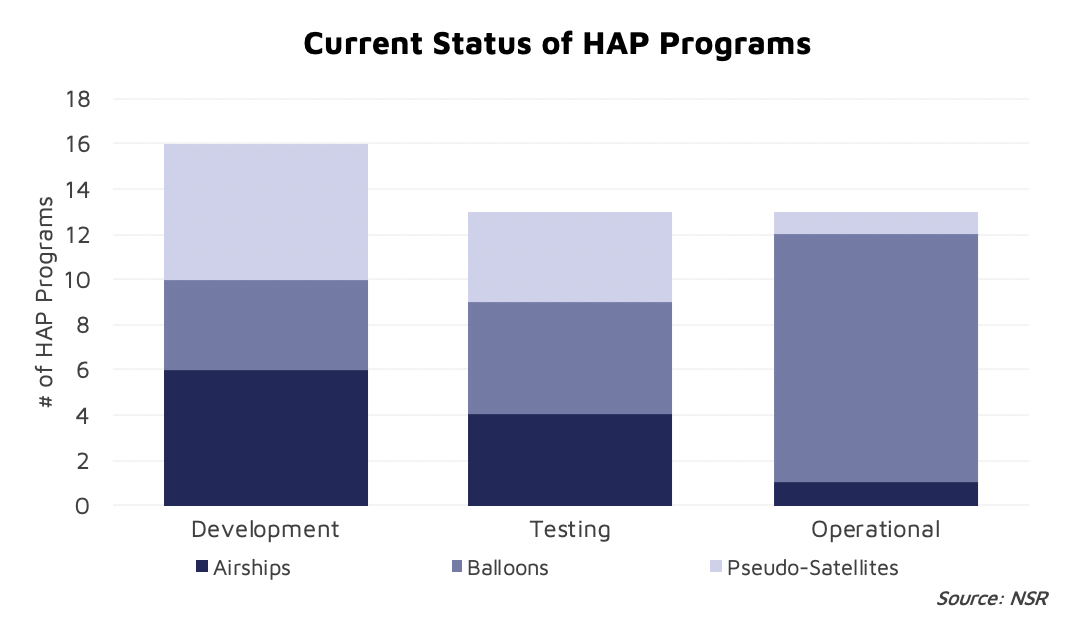

Looking at technology alone, there is quite some overlap between HALE UAS platforms and fixed-wing solar powered pseudo-satellites. It is expected that trends such as the development of Beyond Visual Line of Sight (BVLOS) drone missions and persistent monitoring for ISR in the UAS/aerospace communities are driving such players towards pseudo-satellite-like platforms. Aerovironment (HAPSMobile), BAE Systems (Phasa-35), Airbus (Zephyr) are notable examples here. Such incumbents, with years of legacy R&D, are in some cases the best suited to spearhead initial research on stratospheric platforms now. The high-altitude balloons market is built on a foundation of years of development in the scientific and engineering communities, in addition to current advancements made by players such as Loon and World View. Investments into the technology are likely to continue – that there is interest in the current boom of high altitude platforms is not contested and has been explored already, but how will this market progress in the near-term and what new business models might they bring about?

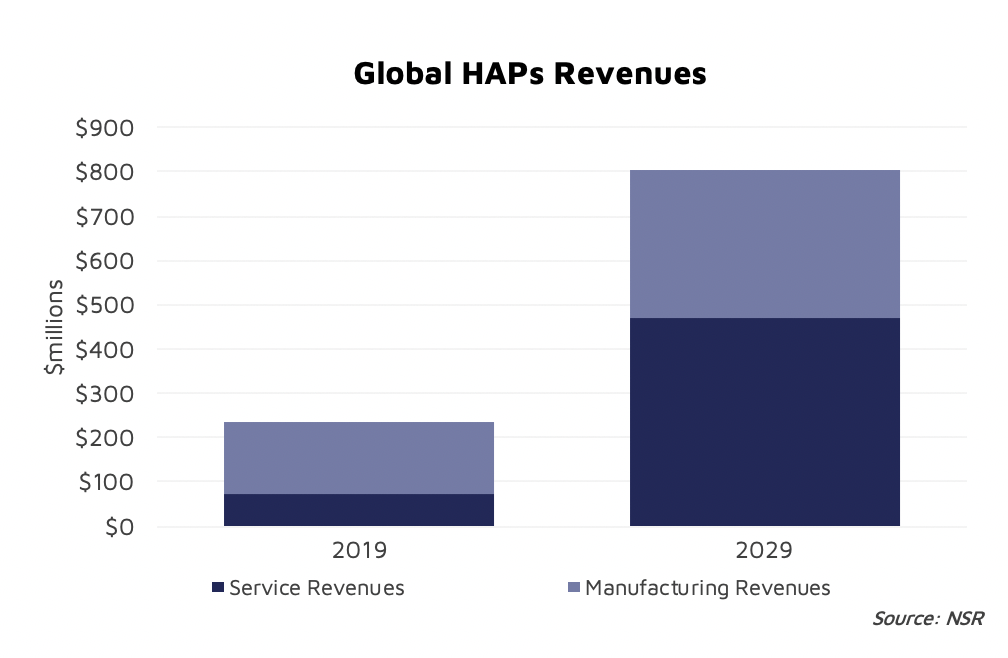

NSR’s High Altitude Platforms, 4th Edition report estimates global HAPS revenue to reach approx. $800 million by 2029, with the bulk of this attributed to manufacturing revenue in the near-term. Service revenue, however, Is forecast to take over in the 2026-2029 time period, as various HAPS programs transition from initial demonstration missions to providing operational services at scale. What were experiments in stratospheric wind-driven dirigibles a few years ago are forecast to present cash flow opportunities within the decade.

While HAPs as a unit product will find immediate applications mostly in the government military and defense markets, the commercial sector drives interest in the X-as-a-Service family of business models, one that has been rampant in recent years across the satellite industry. HAPs are not too dissimilar to satellites from this perspective: a fleet of mobile platforms that a client can lease out / partner with to support their own connectivity networks, or to use as a platform for their remote sensing requirements.

This is particularly true for connectivity applications, where service revenues are forecast to reach upwards of $250 million by 2029. Commercial HAPs services are expected to be rolled out via partnerships with mobile network operators and terrestrial communications providers, utilizing HAPs as a footprint expansion strategy especially in remote and underserved regions.

The HAPs-based remote sensing market is forecast to drive service revenues of approx. $80 million towards the end of this decade. With the right infrastructure in place, high-altitude balloons can provide quicker turnaround times for high resolution imagery, circumventing the orbital schedules and ground station transmission times of satellite data providers. The cost of imagery acquisition is also comparatively lower than that of manned aerial data providers.

The partner ecosystem for HAPs has opened up in the last couple of years, notably with the HAPSAlliance driving industry cross-collaboration initiatives. However, there remain a few key issues to be addressed on the regulatory front to support HAPs market growth: flight and spectrum approvals. The flight profile of HAPs is such that various regulatory approvals need to be had before a platform can be allowed to fly over a certain area of interest. Stratospheric wind patterns dictate the trajectory of a high-altitude balloon across international borders, and the operator will need to have such authorizations in place in each nation for effective platform utilization. Technical conditions regarding HAPs usage of RF communication links and the necessary regulations that govern this usage in a country are also important questions to consider.

The Bottom Line

There remain several challenges to be overcome on the technology front (structural, energy management, system reliability etc.), and regulations are yet to catch up in what is still largely an underdeveloped market. However, recent natural disasters/emergencies and the COVID-19 pandemic have impressed upon the industry the need for alternate data in remote sensing and for backup connectivity networks in remote regions.

This has in turn pushed investments in the HAPs markets, given the unique possibilities and advantages of these platforms over satellites and other alternatives. The need for low latency and increased coverage from downstream service providers also contribute to market demand, leading to a redefinition of the assemblage of sensors and code in the high skies.