Innovation or Disruption Ahead for Gov & Mil Markets?

In a few weeks, the satellite industry will gather in Washington DC for the annual Satellite show. Set in the backyard of one of the largest consumers of commercial satellite capacity in the world, the show will focus on the “What’s New and What’s Next” – a constantly changing conversation in the space industry. However, the commercial industry has largely left Government & Military players behind.

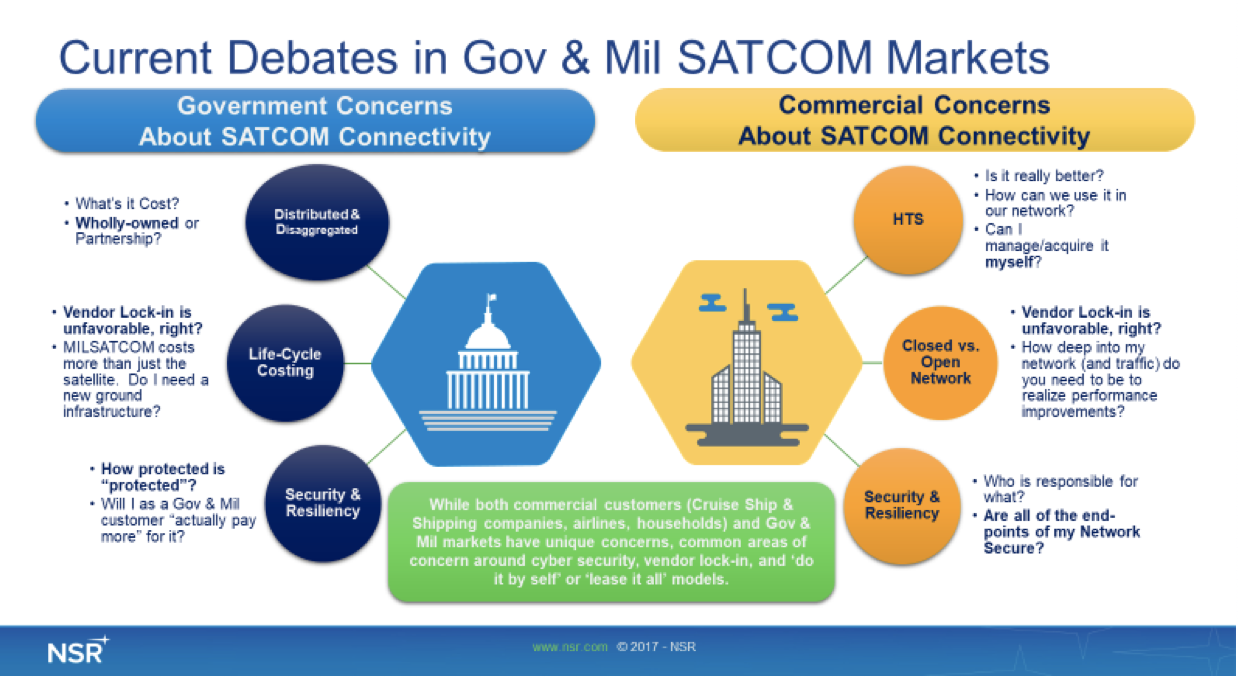

Some of that is for good reason – Gov & Mil customers are hard to do business with. Between a complex set of acquisition rules, unique network or security requirements, an ever-evolving mission set, and uncertain budgets – there are significant differences between solution sets.

Yet, which current or emerging technology can provide some disruption or Innovation to Gov & Mil Markets?

- “___ as a Service”. Be it satellite connectivity or flying government-owned satellites, the service-centric business models adopted by commercial industry will be one of the most significant disruptions. In the satellite connectivity markets, NSR projects that end-to-end managed services will be how the lion’s share of connectivity is delivered to the Gov & Mil markets, almost 2:1 for FSS capacity, and nearly 4:1 for HTS capacity.

- HTS. Almost all of the major players are no longer talking or planning about their HTS strategy – they are executing it. A part of that strategy is tailoring capacity to the needs of customers and end-users – airplanes over the Atlantic, cruise ships in the Caribbean, backhaul customers in Asia-Pacific. When Gov & Mil end-users find themselves in a position to fully leverage HTS, they could be faced with a much more restrictive set of conditions than they are used to – limited choice of ground infrastructure (including the gateways or teleports), or that the “Gbps of capacity” being launched is largely unsuited or unavailable to meet the Gov & Mil mission requirements.

- Non-GEO has (an) answer. In fact, NSR projects that Non-GEO HTS will serve about 20% of the HTS capacity demand by Gov & Mil end-users by 2026. Lower latency, higher throughputs, near global to global coverage, and all of the other boxes checked by these current and emerging solutions sound nice – but they would require a revolutionary change in the pace of technology adoption the likes of which have been unseen in the Gov & Mil markets to become “the solution.” New terminals would need to be acquired and integrated onto platforms, networks likely redesigned, security and operational concerns understood. The Silver Lining – ‘the apps’ are unlikely to need modification.

Today, “Disruption” and “Innovation” are the common bond between incumbents and new entrants. “New Space” players routinely ignore or discount government customers in business cases. Commercial end-users are shifting towards an application-centric view of their network performance – and largely assume that the ‘connectivity part’ just works. Service Providers are diversifying their revenue streams to include non-connectivity services such as hosted media platforms, Big Data analytics portals, and cyber security solutions. Satellite Operators are pushing off GEO investments and shifting towards LEO and MEO strategies. All at a time when Gov & Mil end-users talk of becoming more innovative.

Certainly, innovation is occurring within Gov & Mil SATCOM markets – the Pathfinders from the U.S. Gov are just one example. Changing laws are hard, changing habits harder. “Cloud” models are taking hold in other aspects of Government IT – changing mindsets around what it means to ‘own’ something. Virtualization efforts across the Gov & Mil enterprise are changing technology adoption practices; cheap, flexible, distributed instead of bespoke. Both are strategies publicly discussed when it comes to future space architectures. What is unclear is how much of these discussions will become future programs of record or acquisitions.

Bottom Line

There is no doubt that HTS, cheap(ening) access to space, and the insatiable demand for data have proven serious disruptors to the status quo of commercial space markets. What is unclear is if we are on the cusp of a similar disruption in Gov & Mil markets – or if everyone should be planning for ‘innovation’.