Is Non-GEO a Real Threat to Incumbents?

In a word, Yes! However, market dynamics and the interplay of both are not as simple as they seem.

For a while now, Non-GEO players have been the locus of mixed viewpoints in the Satellite Communication ecosystem due to market forces resulting into success, failure, delays and challenging scenarios. Despite all odds, the momentum for Non-GEOs cannot be ignored. NSR’s Global Satellite Capacity Supply & Demand, 19th Edition, reported ~10% of global HTS capacity demand & revenues were captured by Non-GEO players in 2021, and the market share pie for Non-GEO is expanding rapidly into 2022. What does this mean for the incumbent GEO players? Is the ecosystem transforming towards a competitive, collaborative or expansion environment? Are satellite stakeholders reacting or adapting to the changing landscape?

Positioning and Market Trends

Among many, Starlink has been ahead the most in deployment plans and has achieved close to half a million subscribers as reported recently. Additionally, Starlink is looking to expand the industry peripheries by targeting direct-to-devices as the company has partnered with T-Mobile to fill the cellular bandwidth gaps in remote areas. AST Spacemobile and Lynk Global are also working on this technology development and if successful, this can unlock a massive opportunity for the Satcom industry. OneWeb, on the other hand, is targeting the Enterprise and Backhaul markets via the downstream partnership route. With Bharti as a stakeholder, they have lower entry barriers in massive opportunity markets such as India. Kuiper is another major Non-GEO player which is expected to create turbulence across industry dynamics in the latter half of the decade. While there is clear progression in Non-GEO plans, for some if not all, GEO players are also moving ahead (or have moved ahead) in their plans of owning high density satellites with better cost economics – such as Viasat, Hughes, SES, Intelsat, Eutelsat and others.

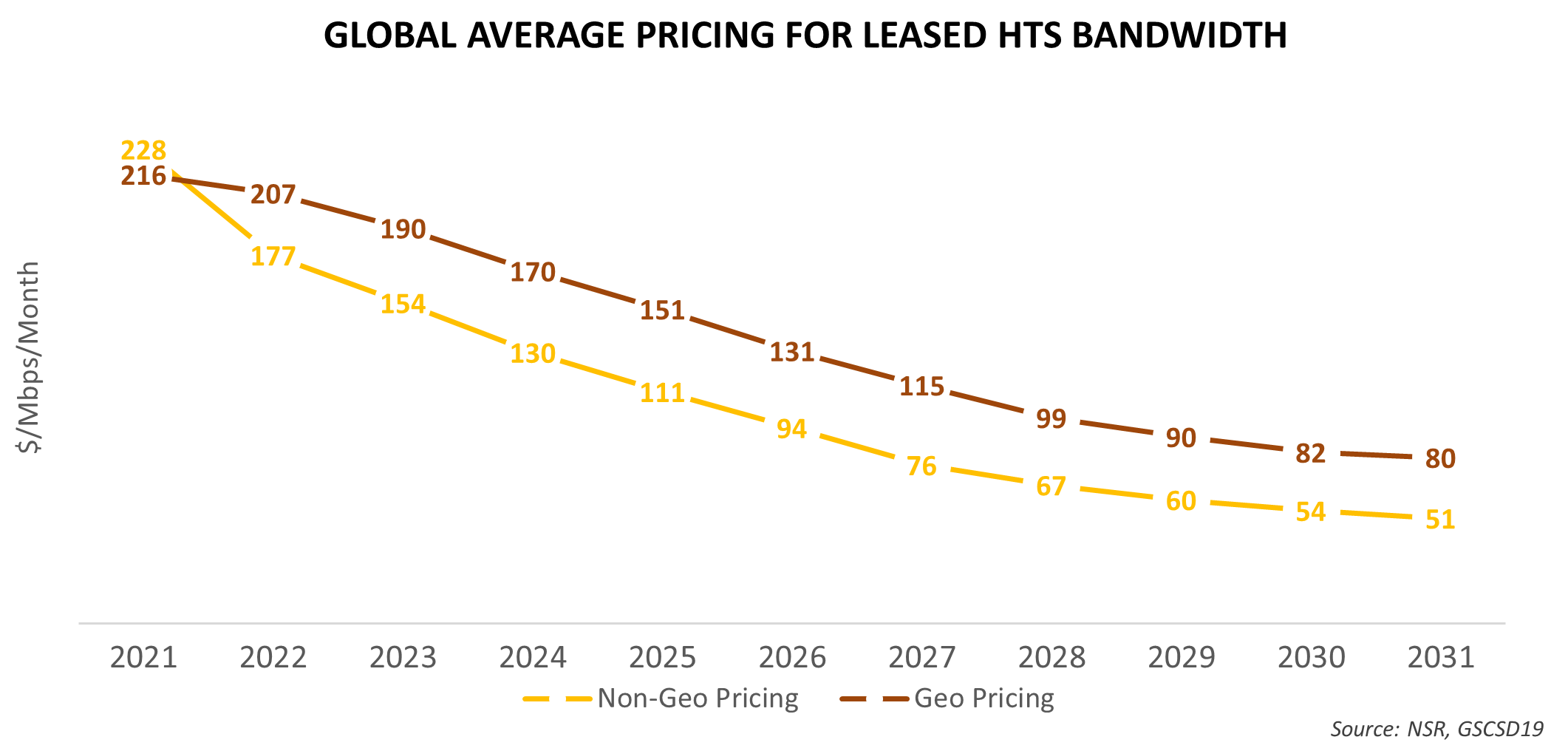

The Price War

NSR’s Global Satellite Capacity Supply & Demand, 19th Edition estimates Global GEO HTS supply to reach 24.5 Tbps and Non-GEO technical supply adding a massive 380.8 Tbps by 2031. With this quantum of supply in the ongoing decade, most certainly there will be steep price erosion across applications and regions.

NAM & EU will witness faster erosion in the near term, however, as more capacity is deployed and regulatory barriers are lowered in the ASIA, MEA & LAM regions – the gaps between the regional lease pricing for HTS will converge. The average price decline for both GEO and Non-GEO capacity is estimated to decline at similar trajectories, reaching $50-$80/Mbps/Month. The average pricing for GEO-HTS is projected to be higher throughout the forecast period, driven by higher pricing for more SLA-based contracts in Enterprise, Mobility and Gov/Mil use cases. These overall price reductions across applications and regions will result in the addition of new users, especially in the Backhaul & Broadband access segments. It is important to analyse the implications on demand and revenues for both GEO & Non-GEO to get a better handle on future industry scenarios.

Demand & Revenue implications

The top trends across applications driving long-term growth are:

- Broadband Access: Massive opportunity exists as close to 50% of the global population still lacks a reliable and suitable bandwidth connection. Demand is ramping up rapidly and with price erosion, it will be on a sustained growth track. The challenges are achieving suitable service & equipment pricing, building robust supply chain, and addressing regulatory challenges.

- Backhaul and Trunking: Telcos are investing in network upgrades, and users’ bandwidth demand is increasing consistently.

- Enterprise Market: Companies are investing in automation and digital transformation, resulting in sustained growth. Governments are investing in digital inclusion programs connecting educational, health, welfare, and other related institutions to the Internet. This is generating and will continue to generate Satcom demand for remote areas.

- Mobility: The segment is on the rebound curve and increasing bandwidth demand is driving market growth.

- Government/Military: Geopolitical scenarios in regions such as Ukraine, Indian Ocean, South China Sea, etc. are driving growth. Military welfare will be a key driving use case for the segment.

The cons for growth are economic slowdown, fear of recession, Russia-Ukraine conflict, program delays, regulatory approvals, equipment pricing for Non-GEO, lack of Satcom awareness in underdeveloped economies and fibre network expansion.

NSR expects the above challenges to be short term and the revenue growth trajectory for Satcom for both GEO & Non-GEO will be achievable, given that stakeholders align their strategies specific to the region and applications.

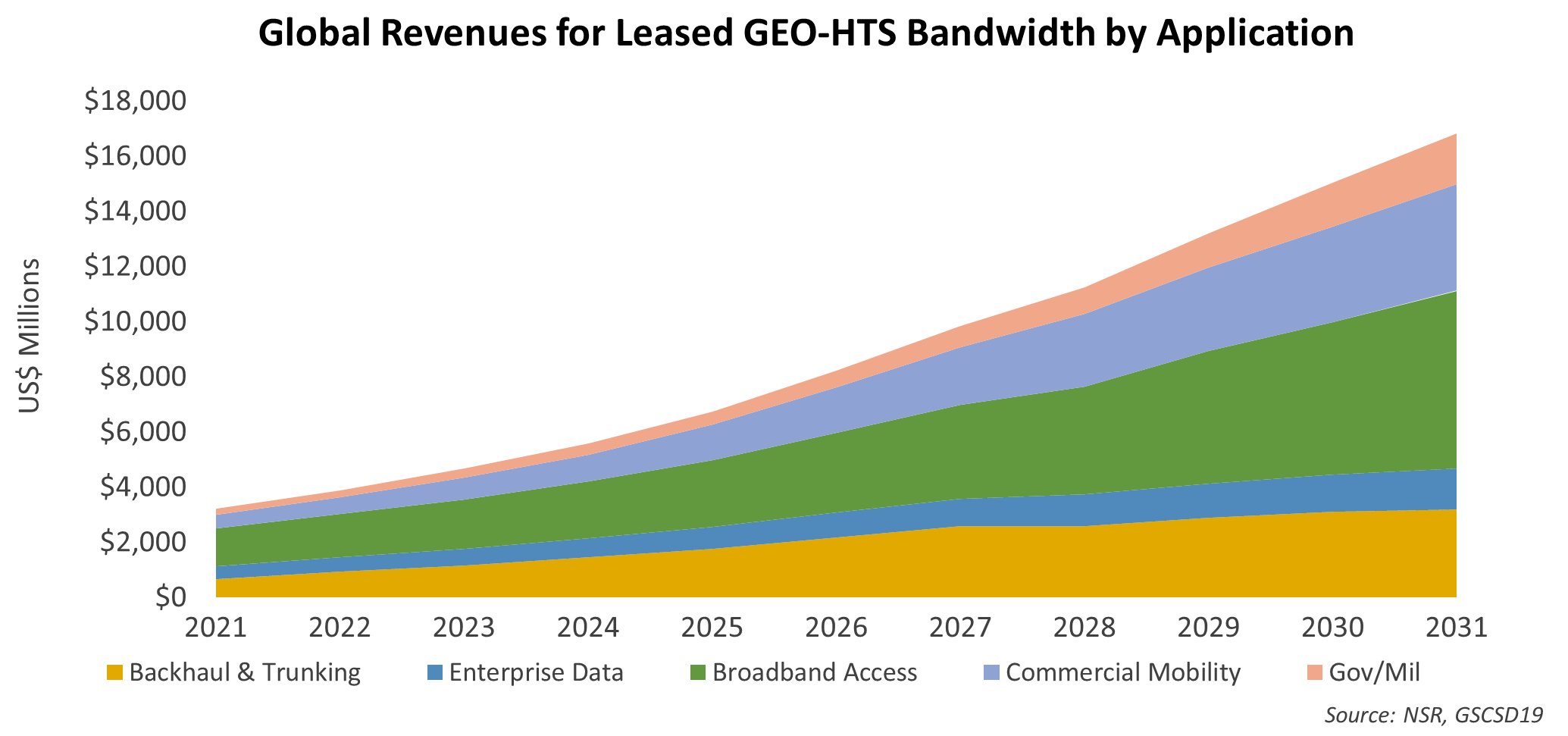

GEO-HTS bandwidth demand is projected to grow from 1.2 Tbps in 2021 to 17.6 Tbps in 2031, aggregating to $98.5 Billion in capacity revenues at CAGR 18%. Broadband access including Direct-to-Premises, Wi-Fi Hotspots and Social Inclusion (RDOF type) will contribute 37% of total revenues. The major growth regions for the segment will be Asia, Latin America, and Africa. Backhaul & Trunking and Commercial Mobility revenues are forecasted to reach ~$3.2 billion and ~$3.9 billion respectively by 2031. Although the Gov/Mil segment will contribute only 9% of the total revenue, it will witness the highest CAGR, i.e., 24.5%. Programs such as BAKTI and BharatNet will drive long-term growth in the Enterprise Segment.

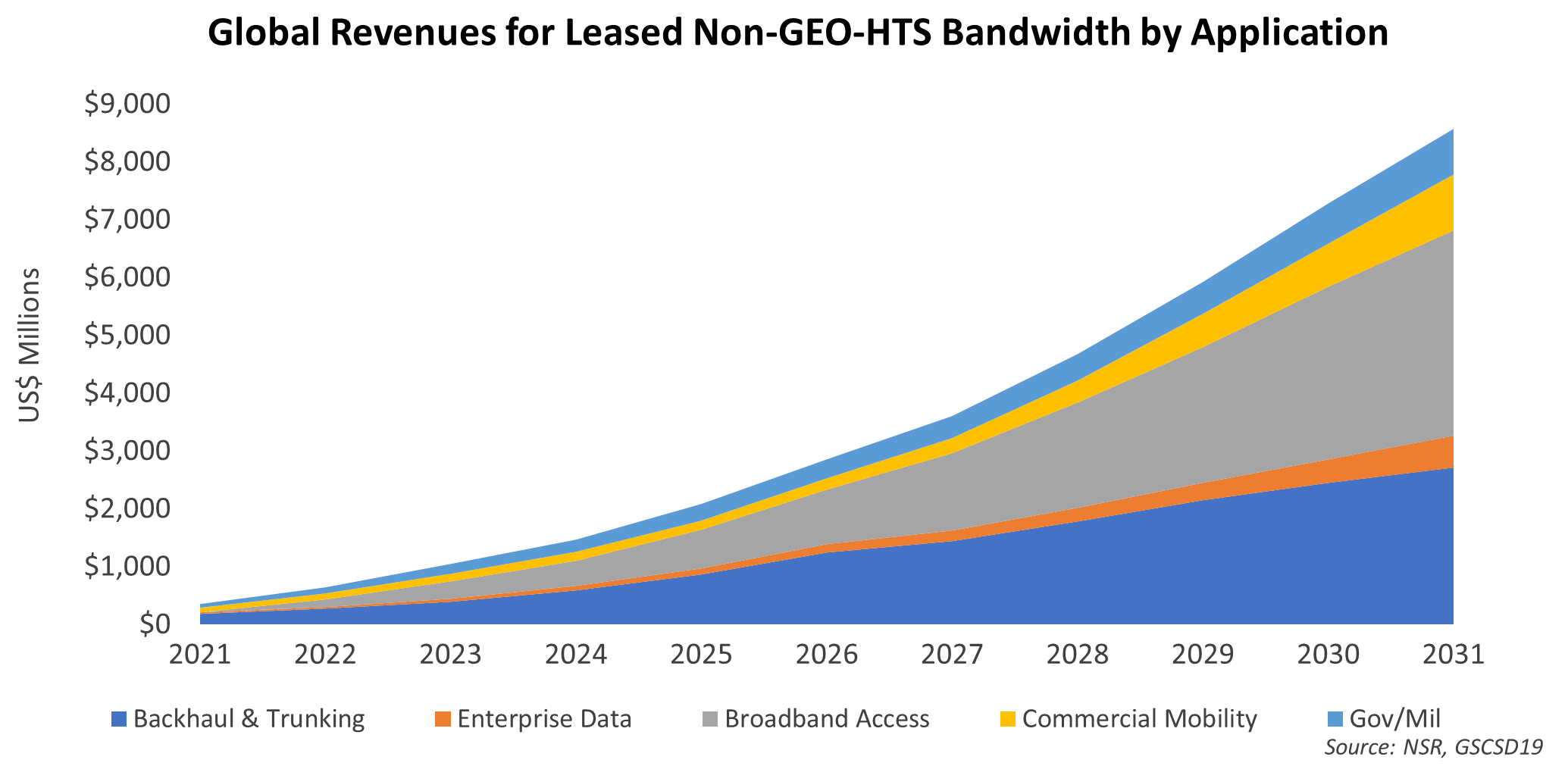

Comparing the GEO Versus Non-GEO HTS revenue curves, clearly the Non-GEO growth trajectory is relatively delayed, as at present only Starlink & OneWeb have their constellations (partly) in orbit. Starlink is focused on a vertically integrated strategy targeting broadband access customers, while OneWeb is taking the partnership route targeting Enterprise & Backhaul customers in high latitude areas such as Alaska. OneWeb has also partnered with Hughes (distribution partner) to further target Enterprise & Backhaul customers.

NSR projects the capacity demand for Non-GEO to grow from 132 Gbps in 2021 to 14.1 Tbps in 2031, resulting in $38.5 Billion in cumulative revenues. Backhaul & Broadband access are the two top growth segments for Non-GEO players. Broadband Access segment will contribute 38% of the cumulative capacity revenue at CAGR 43.9%, primarily driven by Starlink sites. Backhaul & Trunking, driven by Telco partnerships, will aggregate to $14.1 billion during 2021-2031.

Bottom Line

Non-GEO HTS demand capture is projected to increase from 9.6% in 2021 to 44.5% in 2031. Revenue-wise, it will grow from 10.1% to 33.7%. From growth in market share, it is clear that Non-GEO is a major threat to the existing GEO players. But this does not state the true picture. Yes, there are scenarios where GEO players are witnessing churn due the competition from Non-GEO, such as in the Broadband access segment in NAM markets. Also, there will be cases where GEO & Non-GEO capacity will experience head-on competition for the same contracts resulting in a higher bandwidth provisioning and accompanying price wars. But at the same time, the overall addressable market is expected to increase consistently as prices drop, resulting in the opportunity for both Non-GEO players and incumbent players. Additionally, the competitive environment and technology advancements will warrant new opportunities such as Direct-to-devices.

So, what does these mean for industry stakeholders? There are two schools of thought. One, Non-GEO is both an opportunity & threat and hence, incumbent GEO players must build or invest into multi-orbit strategies. SES was the first with O3b mPower, now the Eutelsat-OneWeb merger is another example. The Hughes-OneWeb partnership is also in sync with this thought process. NSR predicts more such partnerships as new constellations are added into the ecosystem.

The other school of thought is that the Non-GEO business case will not close as it will need continuous infusion of capital to replace satellites and most of the capacity is wasted over ocean regions. Whether or not the Non-GEO business case closes is another topic of assessment & discussion. But to exemplify and provide evidence in support of the second school of thought, Starlink lost the RDOF subsidy where GEO players can perhaps fill this gap.

Bottom line is that, although Non-GEO is a threat, GEO HTS will continue to remain the market leader in terms of capacity demand and revenue during 2021-2031 with the consistent expansion of market opportunity. The question then for an industry that looks at a 15-20-year horizon for GEOs is – what happens beyond 2031?