Maritime Satcom: The Makings of an FPA Case Study

Flat panel antennas have great potential to expand the satcom addressable market but remain one of the least developed aspects of the industry. Despite high demand for low-profile solutions for certain applications, and several hundred million dollars of R&D spent to date without much results, FPAs are still struggling to carve their niche.

Some verticals, such as commercial aeronautical and government mobility, have developed and are growing, competitive ecosystems for FPAs through deep-pocketed investment and key partnerships, but most verticals have not shown such progress.

To examine the obstacles challenging FPAs, one can look at Commercial Maritime as a case study.

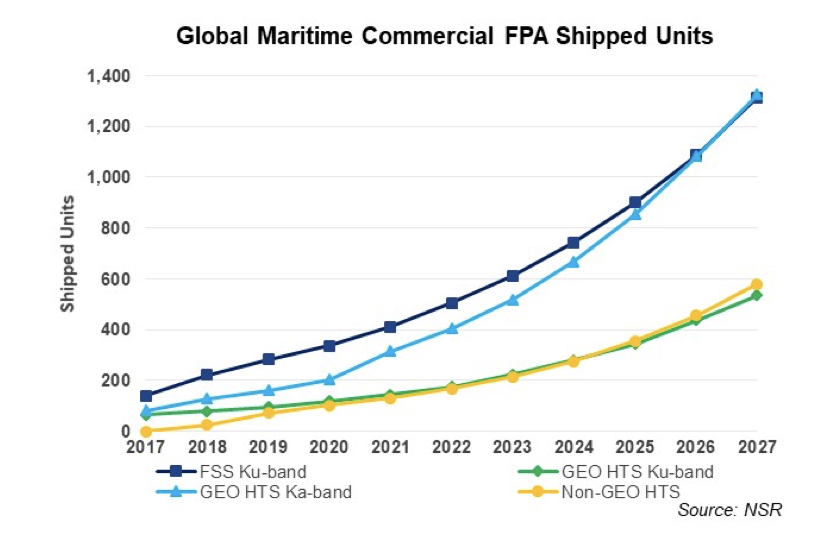

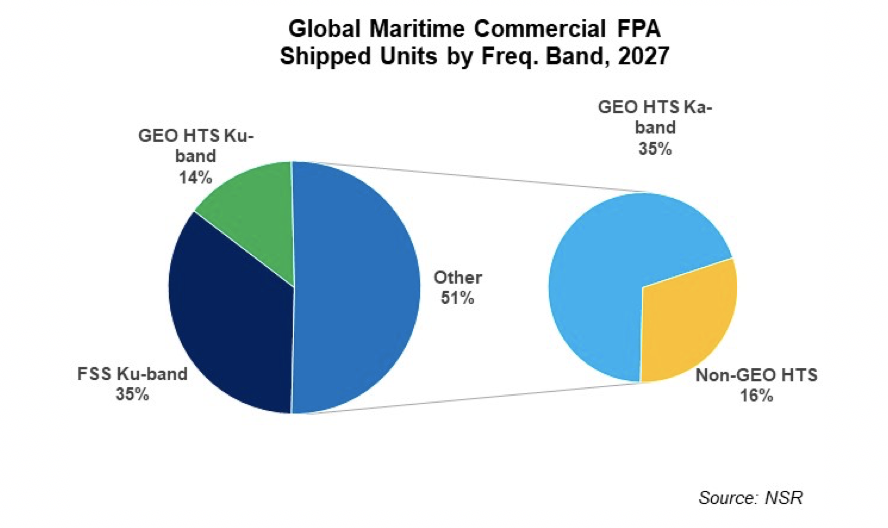

NSR’s Flat Panel Satellite Antennas, 3rd Edition, report forecasts over 2,300 in-service FPAs for Commercial Maritime by 2027, generating cumulative equipment revenues of $280 million. IoT-focused and bandwidth-hungry segments will split the market, with FSS Ku and GEO HTS Ka-band representing 30% and 35% of in-service units, respectively. However, with over 934,000 in-service units expected by the end of NSR’s Maritime Satellite Markets, 5th Edition, report forecast, it is clear FPAs will remain a relatively small part of the Maritime Satcom market.

To better understand why, one must consider maritime satcom technology, competition, and the value chain.

Technology

Flat panel antenna trials for maritime have shown promising results in recent years. However, many remain unsatisfied with the applicability and performance of FPAs at sea. The severe operating environment, need for greater 3-axis stability, and generally low spectrum efficiencies present significant challenges for Maritime FPAs.

Competition

Parabolic equipment for maritime is well-established, in terms of both performance and partnerships. Years of competition have driven down both prices and aperture sizes, with low-profile VSATs cutting into one of the main selling points of FPAs. There has been some progress in launching M2M/IoT FPA solutions, applicable for cargo tracking and vessel operation monitoring; however, despite growing interest in Big Data analytics, FPAs will face competition from new and legacy systems, such as Iridium CERTUS.

Value-Chain

Additionally, the industry (in particular at the service providers’ level) chooses parabolic equipment for each maritime segment and is prepared to cover the cost of the antenna up-front, while recovering that cost through service revenues. While preliminary partnerships have formed between FPA manufacturers and service providers, these relationships have not been well-defined, with FPAs lacking the support of an end-to-end value chain in Maritime.

Hope is on the Horizon

However, several factors may work in FPAs’ favor going forward. Non-GEO HTS capacity will likely necessitate the fast-scanning capability of electronically-steered antennas, and as technology improves, price points are expected to drop. Eventually, SPs may find certain customers more inclined toward a flat panel than a parabolic dish. Finally, the potential for interoperability may allow FPAs to act as the perfect compromise between high and low-bandwidth solutions, adequately serving both, an important factor for Maritime as many fleets seek to diversify, better manage, and secure their networks through separate channels.

Bottom Line

Flat panel antennas are still an emerging product. While the technology has been in use for some time, FPAs have historically been applied only in use-cases that necessitated a low-profile solution. Competition and a lack of value-chain support will be considerable challenges for FPAs to overcome in any market, but especially in Commercial Maritime. However, to meet rising demand, close new non-GEO HTS business cases, and reach under-addressed customers, Maritime SPs should consider the long-range potential of flat panel antennas.