Mining Satcom: Jump-Starting a Stalled Market

Mining should be an ideal energy segment for the satellite industry to generate progressing revenues, given the remote nature of operations, the mission-criticality of requirements and the growing digitization activities in the sector as a whole. Yet, historical data points to a stalled market, owing to a variety of factors that need to be quickly addressed in order to fully tap into “low hanging fruit” in terms of opportunities the industry can extract. What efforts can lead the industry to in a sense, bear fruit?

Expand the Market Base

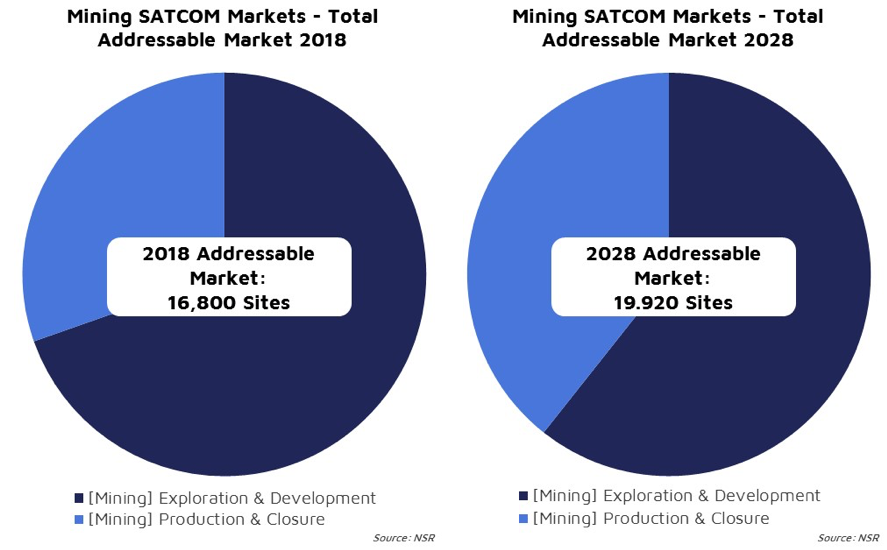

Satcom players have been able to penetrate only a small portion of the total addressable market as the miners’ operational inertia and not-so-targeted-strategy, vectors down the significant adoption rate in this segment. According to the recently published NSR’s Energy Satcom Market, 8th Edition report, the total addressable market in 2018 is 16,800 sites and is estimated to rise to 19,920 sites by 2028.

While the addressable sites are significant, albeit with nominal growth, a common revenue generation strategy does not apply to all the miners due to the varied behavior of mining companies. Mining companies can be categorized as:

Type 1: Incumbents such as Rio Tinto & BHP – The incumbents, i.e. the “top 50” mining companies own/operate 16% of the total globally-distributed mining sites; As stated in the PWC Mining Report 2018, mining companies have ramped-up their exploration expenses by 15% (primarily incumbents), but most of these projects are brownfield explorations – hence not a significant opportunity for the Satcom services. Additionally, terrestrial networks have bridged the connectivity gap in the developed markets, especially in regions such as North America and Australia. For these markets, satellite-based solutions are used typically as a redundant solution. So, where is the gap for Satcom players to fill-in? The opportunity here is in mine digitization and automation, especially in the Latin America and Africa regions. Incumbents are prioritizing the digitization and automation efforts to reduce the production and exploration cost. The growth potential for the Satcom Players (from the Type 1 miners) is not just in the connectivity offerings but in the value-added services such as Cloud computing, Data Security, Process Analytics, IIoT (Industrial IoT), Wi-Fi-hotspots, etc. For example, ITC Global’s solution to the BHP Billiton Mining Operations addresses the real-time automation and network integration requirements.

Type 2: Small mining companies typically operating 1-3 mining sites – These mining companies sum up to greater than 80% of the total (global) addressable sites. The major challenge with these mining companies is the non-affordability of satellite solutions. So, what should be the Satcom players’ growth strategy with this large and untapped addressable market? Clearly, satellite operators/service providers cannot achieve immediate profitability with these players, but these Type 2 miners are significant for the long-term sustainable Mining Satcom Market growth. The key revenue growth strategy for Satcom players has to be – “Grow-as-the-miner-grows”. A hypothetical but executable path would be to enter into a long-term contract with dynamic service pricing and gradually bundle add-on services.

Lower Pricing Expands Market Base and Usage

As detailed above, 80% of the addressable mining sites fall on the critical band of price sensitivity. Can falling capacity prices turn the table around for the Satcom Mining Segment? NSR predicts that the Satcom mining market will witness a significant rise in the number of in-service units and bandwidth demand, jump-started by falling capacity pricing. By 2024, additional competition from non-GEO offerings will push prices further down, resulting in tapping the larger market base in this segment.

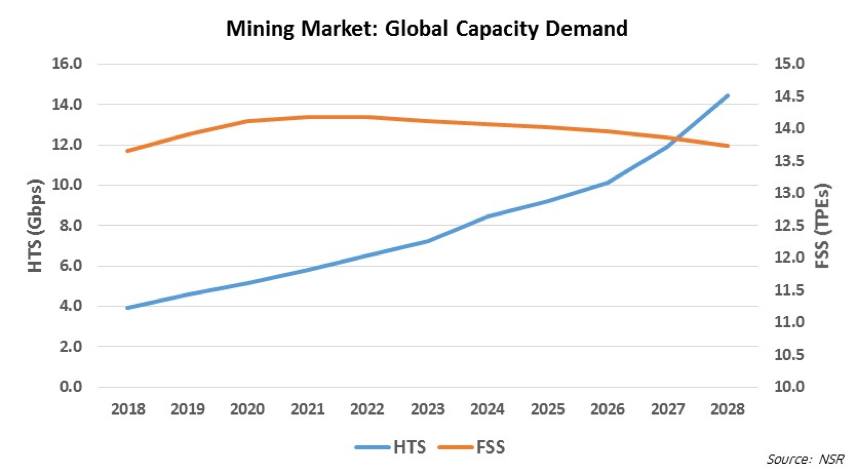

According to the NSR’s Energy Market, 8th Edition Report, the Gbps demand for High Throughput Satellites (HTS), both GEO & Non-GEO, is projected to ramp up by greater than 3.5x during the forecast period 2018-2028. The accelerated growth in HTS bandwidth demand is attributed to competitive pricing, flexible solutions, mine digitization, implementation of automation solutions and inclusion of the new customer base; i.e. the untapped 80% of the market. Conventional Fixed Satellite Services (FSS) will decline slightly but hold their ground at around 14 TPEs/year as the effect of dropping in-service units will be compensated by increased bandwidth demand per service units.

Mining Segment: Revenue Opportunity

NSR forecasts cumulative global revenues of $1.04 Billion for the mining segment during the period of 2018-2028. The greater growth opportunity will be for equipment suppliers, as equipment revenues are projected to grow at a double-digit CAGR for Production & Closure sites to capture the transition from legacy FSS to emerging HTS offerings and extended customer sites. A way to manage slow, steady revenue growth from capacity contracts in the short term is to bundle in other elements in the value chain such as equipment sales, managed services, and other value-added features that boost contract values.

Bottom Line

Dropping capacity pricing may not be a positive (typically) for the Space Industry, but it is the primary variable that will keep the Satcom Mining Market afloat. The key to sustainability is addressing the unaddressed as that constitutes >80% of the total sites. For the core 16%, SATCOM operators and service providers need to push for additional value-added service avenues including Cloud computing, Data Security, process analytics, Wi-Fi-hotspots, etc. for steady topline segment growth. Put simply, downward pricing unleashes demand elasticity for 80% of the market, while value-added services provide a premium to negate price degradation to large incumbents.