Pitching Satellite Backhaul

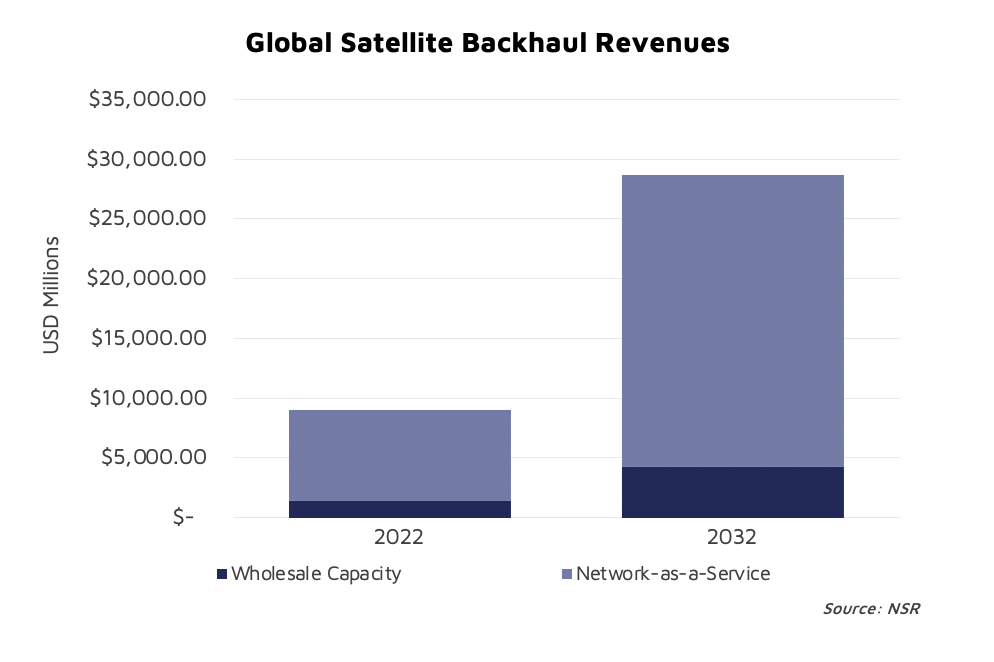

Backhaul is one of the key verticals driving growth for the Satellite industry. What challenges can Satellite solve for the Mobile industry? There is a big potential to be realized by expanding Mobile coverage: attracting new subscribers; enabling new services; or optimizing investments. As the industry heads to Barcelona for the MWC, what should be Satcom’s “pitch” to capture a portion of the $210.8B 2022-32 cumulative revenue opportunity in Satellite Backhaul (Wireless Backhaul via Satellite, 17th Edition)?

What’s on MNOs’ minds?

The Satellite industry is probably too “self-centered” so to speak. Actors in Satcom should put more effort into understanding customers’ needs and be less centered on ‘how cool’ Space and its technologies is.

MNOs are worried about finding new sources of differentiation and new growth drivers as their core telecoms revenues suffer from stagnation (<2% global revenue growth according to GSMA). Hence, Satcom’s pitch must provide an answer to these needs:

- improving customer experience by extending Broadband coverage and ultimately becoming a driver for subscriber retention and ARPU growth;

- unlocking new revenue streams through offering connectivity beyond MNOs’ current footprint capturing new subscribers and offering new services on Cloud, Enterprise, IoT and critical connectivity such as First Responders;

- optimizing MNOs’ investments by cutting CAPEX and OPEX expenditures on rural deployments while still meeting regulators’ coverage obligations. Solving the challenges of network resiliency reducing MNOs’ need to invest on multi-path fiber deployments.

Building assurance and facilitating adoption

The good news is that MNOs are now listening to the Satellite industry after years of struggling to get their attention. However, there are still a few fundamental doubts deterring adoption of satellite. Satellite must do a better job in building the trust and assurance that it can meet MNOs’ network requirements such as allaying doubts among MNOs in terms of consistency of SLAs. Additionally, satellite continues to require very specific know-how, and it is not always easy to integrate under the MNO core including OSS/BSS integration, network functions orchestration, and many others. Furthermore, MNOs prioritize their investments and focus their skills on their core business – the urban areas. Consequently, MNOs’ risk appetite for ultra-rural deployments is much lower, and their operations are optimized for urban locations.

Adoption of Telco-driven standards such as MEF, 5G orchestration; demonstrating experiences in past (and critical) deployments; and development of turnkey offers requiring very little deviation from MNOs’ standard operations; combined with the willingness by Satcom integrators to share the risk via revenue share, linking revenues to SLAs, and other business models could help MNOs feel more reassured and trigger higher adoption of satellite.

The Bottom Line

The satellite industry must do a better job in approaching MNOs. It is fundamental to identify the needs of Telco operators – differentiation from competition, activating new growth drivers and optimizing investments – and develop the appropriate offers accordingly.

NSR supports vendors, service providers, satellite operators, end-users, public agencies, financial institutions and the Telco ecosystem in their Satellite technology and business strategy assessment and planning.

Please contact info@nsr.com for more information.