Profiling Maritime Customers to Stay Afloat

Maritime markets have long been labelled the ‘sleeping giant’ of mobility satcom. Not as driven as in-flight connectivity, nor as full of potential as the connected car, maritime in years past seemed quite content to stay on its slow and steady growth course.

However, falling capacity prices, new form factors and possibilities from analytics as well as upcoming LEO constellations are making broadband satcom connectivity more and more enticing to maritime fleets. From Navarino and Thuraya, to Zodiac and MSI Ship Management, it seems there is a new VSAT offer or installation announced every day.

A rising tide may raise all ships, but considering the wildly different fleet profiles in maritime, knowing the customers in these market segments is more important than ever before to stay ahead of the game as more VSAT adoption drives revenues growth.

NSR’s Maritime Satcom Markets, 6th Edition report forecasts over 641,000 in-service units generating $4.8 billion in retail revenues, by 2027. More than half of the broadband vessels connected will do so via VSAT, with many using MSS equipment for redundancy and improved global coverage. Merchant and Leisure are expected to be the core gaining markets for VSAT, while Fishing will continue to drive MSS adoption. If we examine each vertical, we see varying degrees of adoption tied to each end-user profile.

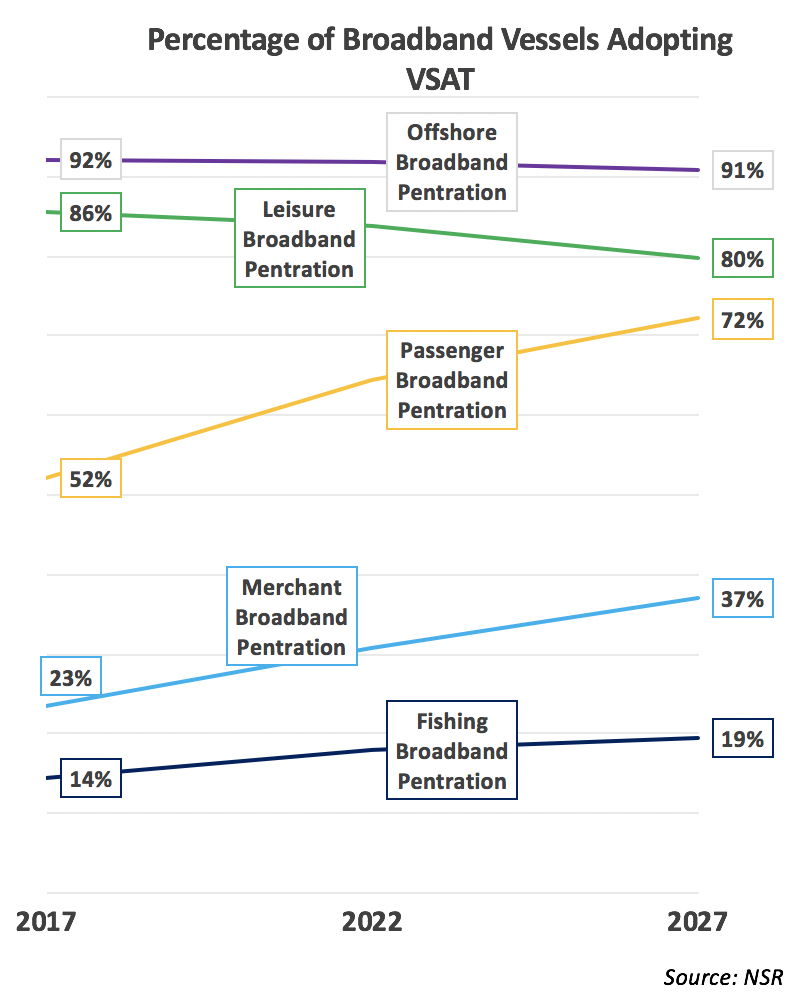

Merchant

With the second-largest addressable market, behind Fishing, the percentage of Merchant broadband vessels adopting VSAT is expected to grow to 37% by 2027. Cheaper capacity will drive VSAT adoption, as fleets can get more while keeping expenses consistent in this cost-conscious vertical. At the same time, new form factors, and data analytic services showing returns are encouraging investment in higher-capacity, more complex VSAT solutions. However, end-user budgets and terminal costs will continue to limit market growth, and trade barriers only look to increase in the near term due to new tariffs and policies, potentially steering fleets away from prime satcom-enabled, oceanic, connectivity to coastal, terrestrially-competitive routes.

Passenger

The fastest-growing segment, Passenger, is also the most complicated to capture. From ferries to ocean cruise vessels, there is a wide spectrum of customer needs. Ocean cruise is extremely competitive, and highly penetrated, with savvy customers demanding the most flexible, data-intensive services on the market. Here, non-GEO HTS services will make the greatest play, growing from niche to necessity, responsible for 54% of retail revenues by 2027 in the Passenger segment. Growth in numbers is expected not on the ocean, but on rivers and ferry routes, where, once again, lower capacity prices and new form factors make a difference. End-user budgets will continue to make it difficult to capture the lower end of the market, and vessel density and contention in high-traffic zones will be an ongoing challenge for GEO-HTS and FSS connectivity.

Offshore

Still in recovery mode, Offshore will remain flat both in terms of addressable market growth and VSAT adoption. Sites are downsizing, cutting costs and inefficiencies, and this is a double-edged sword for satcom; while remaining sites are pushing hard for digitalization and connectivity, the focus on the bottom line constricts on-site investment. Added to this, terrestrial connectivity poses the greatest threat to satcom in this segment, on a pure proximity basis. Satcom-terrestrial hybrid solutions, and those with the highest throughputs and greatest support for digitization will be must-haves for SPs, presenting a high barrier to entry and an increasingly competitive market.

Leisure

Satcom penetration into the Leisure segment is expected to grow, but not at the pace of its addressable market. Similar to Passenger, there is a diverse set of needs in Leisure, between super-yachts and smaller craft, making it challenging to lower prices and standardize solutions. New terminal form factors, such as flat panel antennas, and lower capacity prices, will certainly increase satcom penetration, yet are forecasted to remain too high to unlock smaller coastal cruiser markets effectively. Migration from MSS to VSAT is expected to continue, but MSS remains the key to connecting new customers.

Fishing

Commercial fishing fleets will largely remain on FSS capacity, if they are connected at all. Higher-end fleets, with more data utilization needs for tracking and reporting, will migrate to VSAT solutions, provided the increased terminal cost is offset by falling capacity prices. Similar to Leisure, MSS will be key for connecting new customers, and the highly distributed market with relatively low per-site demand will leave plenty of play for FSS Ku-band solutions.

Bottom Line

Maritime connectivity is growing, but not evenly across all market segments. Falling capacity and terminal prices will help to transition customers from MSS to VSAT services, generating higher ARPUs for service providers, yet MSS connectivity will be key in penetrating addressable markets. End-user budgetary constraints affect all segments, and terrestrial competition will only become a larger problem if not properly incorporated into service provider strategy going forward. The rising tide of innovative technology, capacity, and services will greatly cater to the higher-end fleet enterprises, but knowing better the profile of customers coupled with flexible network design, and competitive terminal prices will be necessary to stay afloat in the years ahead.