Pumping the Brakes on the Connected Car

The connected car is one of the most talked about opportunities for satellite-based flat panel antennas, yet it remains elusive and still many years away from being realized. With millions of vehicles entering the market every year, the successful deployment of the connected car via satellite could be very lucrative for FPA manufacturers. However, NSR and others remain quite critical and conservative on its potential, viewing the value chain as fragmented, the use-cases poorly defined, and the technology and price points not yet suitable for widespread adoption. These factors have pumped the brakes on the connected car, but the indirect effect of trying to develop this market has developed other uses cases such as connected bus and trains.

Driven by enterprise-focused applications, such as M2M/IoT and passenger connectivity, the last year saw considerable progress for land-mobile FPAs, with announcements from Caterpillar Machines and Penteon (both through hiSky), Satcube, Pivotal Commware, and even Kymeta.. Safety, autonomy, and the need for analytics have driven the successful deployment of commercial land-vehicle FPAs. So, does that mean it could have a positive and shift the satellite connected car market into high gear as well?

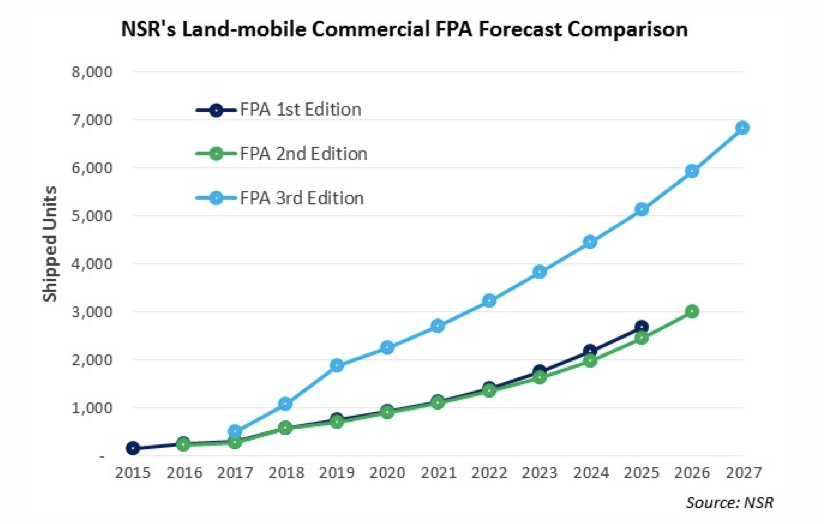

In NSR’s Flat Panel Satellite Antennas, 3rd Edition report, the cumulative equipment revenue opportunity for land-mobile FPA applications is projected to grow to $94 million over the next decade, at a CAGR of 14.8%. North America will take the lead, responsible for 39% of the market opportunity over the next decade, due to an established panoply of FPA manufacturers with a land-mobility focus. Enterprises looking to monitor engines, vehicles, and cargo are turning to flat panel antennas for their low profiles, while equipment manufacturers are finding the generally lower bandwidth requirements an easier means by which to enter this vertical. These factors led NSR to adjust the land-mobility forecasts upwards. However, with only 6,800 units expected to ship by 2027, it is clear the satellite connected car is not expected to drive the land-mobility FPA market.

Several challenges remain for the satellite connected car. Price and performance are key obstacles, compounded by line-of-sight issues and complicated value chain relationships between OEMs, equipment providers, and drivers. More so than any other market, terrestrial competition is of primary concern, as the ubiquity of mobile connectivity detracts from the value proposition of satellite. Indeed, while there is a strong focus for the connected car in China, it is not for the satellite connected car, with many cellular mobile telecoms partnering with Chinese automotive manufacturers.

The Bottom Line

The connected car market is sure to become a reality. From autonomous vehicles, software updates, and passenger connectivity, demand is growing. Partnerships along the value chain are working to meet this demand, by ensuring that the next generation of consumer automobiles comes standard with always-on connectivity. Hybridization is where satellite fits in, a fact recently endorsed by Intelsat. Satellite/cellular hybrid solutions would allow the unique value propositions of both technologies to work together, taking advantage of wide-area coverage, high speed, multicast delivery, everywhere, all the time.

Going forward, land-mobile FPAs will be better suited for the connected bus and train, monitoring fleet operations and providing valuable insights through low bandwidth M2M/IoT solutions as competition, price, and performance will be key challenges stalling the prospects of the satellite connected car.