Retail or Wholesale – What is the Right VSAT Strategy?

It is an indisputable fact that capacity pricing is falling year-on-year, and satellite operators are feeling the pressure to ascertain how to achieve consistent capacity revenue growth. The trend is likely to continue with dropping upstream asset cost per Gbps and the rise in in-orbit competition. Satellite operators moving down the value chain, telco players diversifying their service portfolio, satellite operators partnering with service providers or other regional satellite operators, service providers partnering with regional telco players and service providers partnering with equipment manufacturers/distributors/service distributors are some key strategies industry stakeholders are employing to achieve growth in the fixed VSAT market.

Typically, upstream players arrived at the conclusion that the downward focus with diversified products/services (i.e. managed) at affordable pricing specific to the industry segment, is the only solution for sustained growth in the long term. Almost all satellite operators, including the Big 4 – SES, Intelsat, Eutelsat, Telesat – now have parallel retail/managed offerings for different customer segments in addition to their wholesale business. In recent news, EchoStar is selling 90% of its broadcast – leasing business, owing to the pressure from dropping capacity prices, and will henceforth primarily focus on retail segments. Does this mean the line between a retail and wholesale player is fading with upstream players competing with their own customers? Is this the right strategy for the Fixed VSAT ecosystem?

What is attracting upstream players towards the downstream market segment?

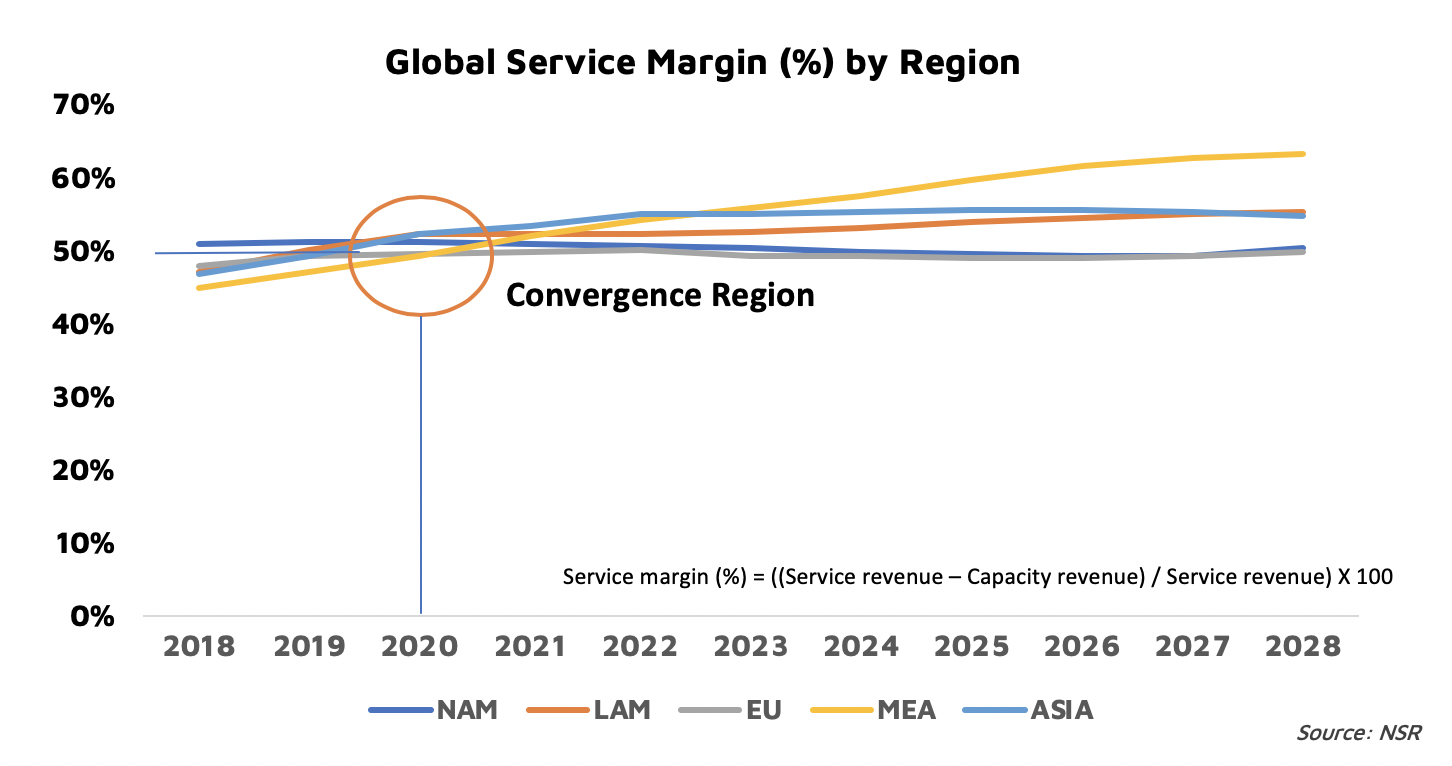

In a word, margins. Downstream service margin is one of the key variables pulling the ecosystem closer to end users. According to NSR’s VSAT and Broadband Satellite Market 18th Edition report, average service margin for the fixed VSAT market will range from 45% to 63% during 2018-2028 across all regions.

The service margin variance for the base year, i.e. 2018, is smaller; however, as we move further in time, the service margin variance diverges. It is due to regional behavior and the likely entry of new players (Non-GEO) and solutions (HTS, VHTS). SpaceX, OneWeb and Amazon are among the top Non-GEO players planning to install mega constellations, while Jupiter-3 & ViaSat-3 are upcoming GEOs likely to be fully operational in 3-5 years.

NAM and EU are mature and the most competitive markets, hence margins are likely to decline. Whereas developing regions including LAM, MEA & ASIA are more likely to witness growth across applications, and due to service scale-up, overall margins are also likely to grow. As a result of this dual nature across different regions, the analysis has an intersection point at around 50% service margin in 2020. 50% signifies the convergence of service margins for different regions as a result of the drop in capacity pricing and the rise in competition. The drop in capacity pricing will ensure better margins for service providers, especially in the LAM, MEA & ASIA regions. Looking at capacity pricing, prices closer to USD $200/Mbps/month are the new HTS Ka-band standard, and deals on competitive regions for wideband have reached a low of USD $300/MHz/month. Prices are likely to fall even further, with the influx of VHTS and non-GEO HTS platforms, during the period 2021-2022 – unlocking price elasticity across different applications and further improving bandwidth for downstream players.

So, price drops, which are “bad” for the wholesale business lead to volumes, which are “good” for the retail business. What’s the net result for margins? Good…very good!

Wholesale or Retail

NSR’s aggregated service margins per region clearly suggest the downward movement of players for stronger bottom line; i.e. the retail play for satellite operators becoming a preferred strategy. But it is key to note or assess when and how the different aspects of the downward transition needs to play out. Clearly, existing/regional downstream service providers or managed network providers better understand downstream customers and have been the connecting link between end-users and satellite operators. The current market dynamics create a dilemma among downstream players about their role in the value chain. Understanding customer demographics and behavior is a time intensive process and hence, the downstream transition of satellite operators ignoring existing service providers is not likely to be successful for all segments of Fixed VSAT and in all the regions. A recent example – Kconnect Africa, launched in 2017, performance is still below expectation where Eutelsat is strategizing to the ramp-up quickly throughout 2020 and the next few years. So, while retail is the preferred option for satellite operators, they must still contend with and follow the wholesale play in regions and applications where they lack expertise. And building expertise is a bit tricky, where choices include developing it in-house, buying players with expertise or through partnerships.

Bottom Line

Downward transition is key for releasing the mounting revenue growth pressure among satellite operators. But the path towards the end user has greater challenges in terms of execution. Clearly, retail service margin shows an overall larger bottom line opportunity, but the other variables governing the transition such as downstream infrastructure, supply chain, understanding of customer segments, partnerships, in-house capabilities, regulatory approvals, etc. cannot be overlooked. Nevertheless, the trend and the strategy going forward is clearly to get closer to the end user whatever shape or form that takes.

Recently, satellite operators poaching customers from service providers, i.e. their own customers, has been the exception and not the rule. Over time, the reverse may take hold and it will be interesting to watch how the wholesale-retail dynamic, as well as the relationship between satellite operators and service providers, equipment manufacturers and other players in the value chain/ecosystem unfolds.