Satcom Mobility Takes the Wheel in Cloud Demand

The satellite communication industry is undergoing a significant transformation, due in no small part to the advent of software defined networks, ground segment virtualization, private 5G, and digital transformation across various industries. And to drive this change, cloud computing has emerged as a crucial enabler for driving innovation, improving performance and facilitating new use-cases. As these applications continue to gain momentum, it raises the following questions: Which verticals drive the majority of satcom cloud service demand, and what are the implications of cloud adoption?

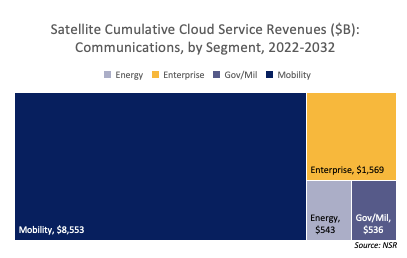

NSR’s Space Cloud Computing, 4th edition report forecasts a cumulative opportunity of $11.2 billion for satellite communications from a cloud data traffic demand of 350.4 EB in the next ten years. Underpinning this growth is satcom mobility, which drives 76% of cloud services revenues generated.

Hyperscalers Make Moves

With hyperscalers increasingly investing in new deployment for satcom applications, they provide the impetus for future growth across verticals such as mobility, energy, government/military, and enterprise. Satellite operators such as Intelsat are working with Cloud Service Providers (CSP) like Microsoft Azure to provide fast, reliable and cost-effective network connectivity to their enterprise customers. Similarly, CSPs like AWS are combining forces with non-GEO operators, in this case OneWeb to offer next-gen virtual network functions to its customers. These increasing partnerships to offer cloud and IoT options, coupled with the ability of non-GEO HTS systems to fulfill low latency requirements, will propel the adoption of cloud services.

Furthermore, the perpetual growth in space data collection, its processing at the edge, and the need to integrate it to generate meta data with more useful geospatial information for effective analysis and insights that facilitate decision-making, are driving the expansion of the cloud computing market.

There are various approaches and methods that improving the operations and performances of satellite communications in the mobility markets. These are driving applications as sectors are moving towards digitization.

Clouds Over Seas

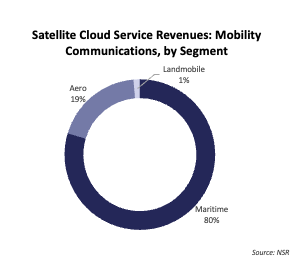

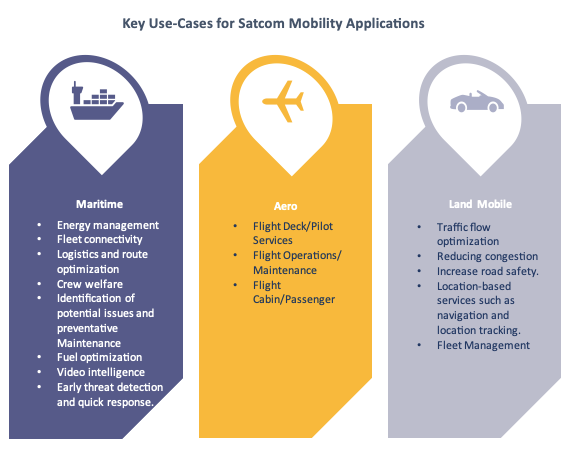

The maritime sector has conventionally relied upon manual systems and processes, which are time-consuming and error prone. These legacy systems lack flexibility, scalability and are ridden with connectivity disruptions. In contrast, digital systems enabled by cloud computing can enable improved efficiency, accuracy, and safety in maritime operations. Container giants such as MSC are adopting vessel-to-cloud digital data infrastructure for increasing sustainability, route optimization, increasing fuel efficiency, automated reporting and crew welfare. Cloud to vessel applications can boost vessel security by early threat detection and quick response. Also, minimal physical intervention due to ability to troubleshoot and resolve issues remotely will reduce costs of sending personnel for maintenance and repair. The ability to seamlessly communicate leveraging smart networks with onshore personnel with real-time updates has enabled wider cloud adoption, such that NSR expects maritime to drive 80% of cloud services revenue for mobility applications over the next decade.

Clouds in the Sky

In the aeronautical connectivity markets, NSR has seen many airlines enhancing their digital system landscape and leveraging cloud expertise to optimize flight operations, maintenance, enhance customer experience and engagement to minimize risk of errors and delays caused by manual processes.

Passengers and business jets are leading the way in adopting cloud services, with applications such as health monitoring, predictive maintenance, tracking, and flight operations management driving increased data traffic and cloud service revenues.

On land, while the addressable market remains the highest, satcom mobility solutions on Earth drive the smallest portion of satellite-enabled cloud services for mobility due to widespread availability of terrestrial connectivity. Still there have been several agreements signed between CSPs and satellite operators to leverage the Cloud to benefit their customers, due to the higher level of software usage expected in the connected car market.

The Bottom Line

Mobility, spearheaded by maritime, is fueling the demand for flexible, scalable, and efficient cloud-based solutions. Satellite operators are forging partnerships with CSPs, and Non-GEO HTS systems are aiming to fulfill low-latency requirements for mobility, driving substantial growth in capacity demand and the associated use of cloud services in the mid- to long-term. As CSPs continue working with satellite operators to tailor their services to industry, mobility will be at the wheel of cloud computing in the satellite market.