Scaling Up FPAs

The satellite communications industry faces a considerable challenge ahead: deploying the ground segment to tap into the huge bandwidth coming from future systems. So much so that many of the discussions at the Satellite 2018 conference underway in Washington, D.C. center on the ground segment with announcements from ViaSat, GetSAT, Kymeta, and other manufacturers. While satellite operators are shifting their focus to LEO constellations, ground equipment vendors are working to develop “next generation” terminals, aiming to unlock the “other 3 billion” and those seeking higher-performance solutions.

Fast-tracking, multi-beam systems, required for LEO-HTS, will arguably require an electronically-steered antenna, possibly a phased array via a low profile. However, the complexity involved with such a design, naturally driving up costs, makes it seem unlikely FPAs will soon unlock the large, mostly unaddressed, price-sensitive markets, such as the connected car and consumer broadband.

How then, does the path look for flat panel antennas? Will the market ever feature the economies of scale needed to unlock those hard-to-reach customers?

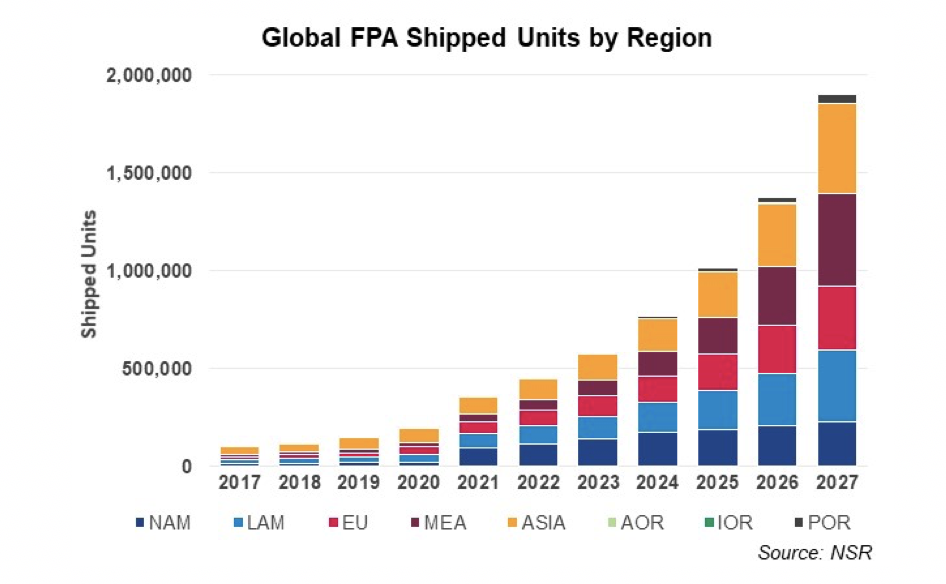

NSR’s Flat Panel Satellite Antennas (FPA), 3rd Edition report forecasts cumulative equipment revenues to exceed $8 billion by 2027, growing at a CAGR of 34.1%. Mobility applications will lead the way, responsible for 91% of equipment revenues, driven by expensive, high-performing systems providing connectivity over air, land, and sea.

Growing demand for “at-home” levels of connectivity while abroad has led to sizeable uptake in satcom adoption for In-Flight Connectivity. This demand, combined with air-drag and fuselage-mounting concerns, necessitated the development of low-profile, flat panel antennas. As such, the Commercial Aeronautical market is expected to continue to grow, dominating Mobility revenues with a forecasted 19,800 FPA units shipped by 2027.

The battle to serve this lucrative market has led to improvements elsewhere, with FPA adoption expected to grow substantially in land-mobile and maritime markets over the next few years.

However, despite this growing success, flat panel antennas currently serve only a small part of suitable markets, leading in aeronautical, government, and military mobility, where price is less of a concern. Until now, necessity has been the driver for FPA growth, and NSR expects this to continue once LEO constellations are deployed, especially given growing interest from Militaries and Enterprise Broadband users for high-bandwidth, low latency connectivity.

Penetrating the connected car and consumer broadband markets will not be easy. While NSR found that 75% of FPA-suitable markets exhibit moderate to high market price elasticity, prices are not expected to drop enough for the commercial connected car, growing more successfully with enterprise passenger vehicles and M2M/IoT purposes on trains and buses.

To reach the economies of scale for lower-priced terminals requires investment and partnership along the value chain. Improvements in modem, terminal, and network design must be complementary to antenna improvements, and only through large numbers will price points drop low enough to be adopted.

However, with the majority of current investment focused on the space sector, ground systems are seemingly forgotten. The battle for non-GEO HTS will be won or lost on the ground, with ground equipment performance and price points acting as the main bottleneck for transformational growth. As such, NSR assumes late investment and focus on the ground sector, and forecasts only 1 million FPA units to be shipped for Consumer Broadband by 2027.

Bottom Line

Flat panel antennas are only now beginning to see success, but due to current conditions and lack of support across the industry, are expected to follow the needs of the few, rather than the demand of the many. Commercial airlines, government and military, and Enterprise Broadband customers will continue to show willingness to pay for the low profiles and unique capabilities FPAs offer. Yet, if operators and providers wish to grow their revenue pie and tackle the large addressable market opportunities with LEO-HTS, much work will need to be done to ensure price-performance curves are suitable for the end customer so that FPAs face less struggle to scale.