Services Drive Space Economy Growth

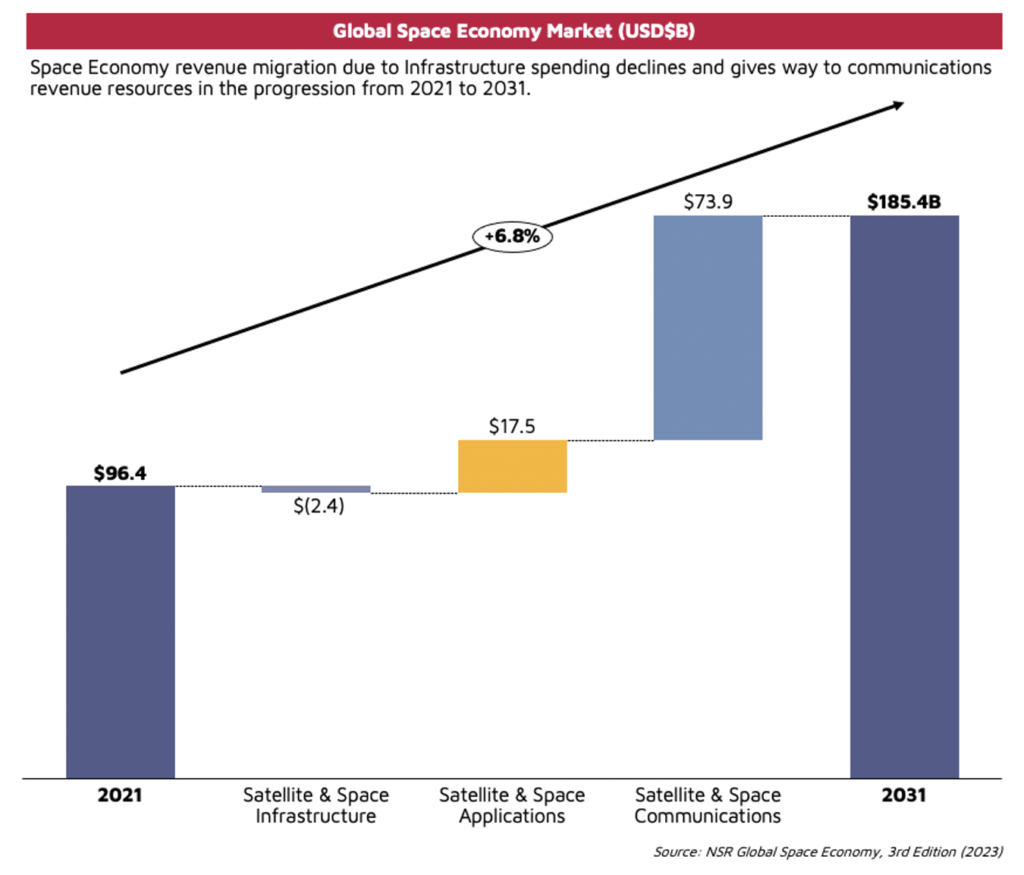

According to NSR’s latest Global Space Economy (GSE) 3rd Edition report, the Space Economy is poised to generate USD$ 1.4 trillion over the period of ’21 to ’31, with a growth rate of 6.8%. Service revenue is the key driver of future revenues as infrastructure investments today move to service revenues tomorrow.

With services largely split between Connectivity services (selling Mbit/s to enterprise, homes, and government customers) and Earth Observation within Satellite & Space Applications (turning pictures of the Earth into actionable insights on the ground), the market is poised to move from an infrastructure-heavy investment cycle towards a service-focused recurring revenue business model.

Earth Observation Remains a Bright Spot

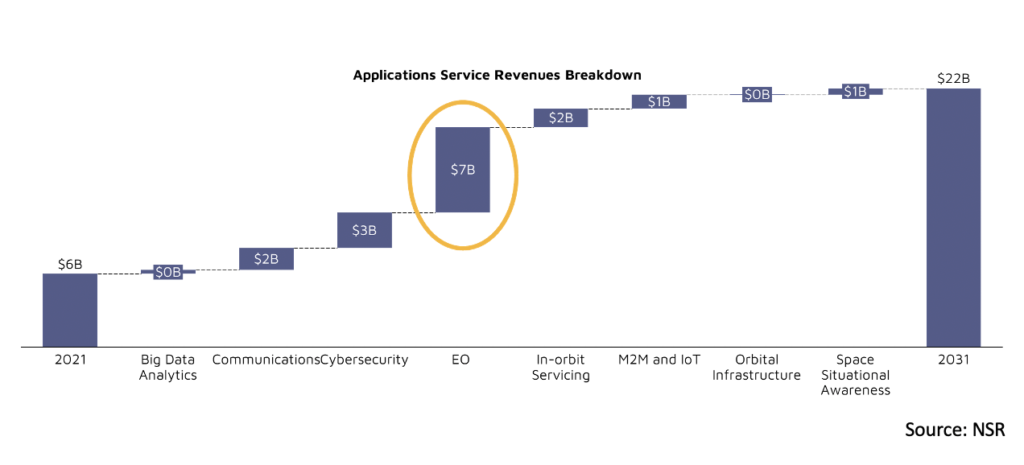

There are two verticals that underwrite the growth in service-centric revenue models:Earth Observation (EO) and Direct Satellite to Device/Smartphone (D2D). Space Applications, ranging from M2M/IoT to Earth Observation use-cases, will reach more than $22 Billion in service revenues by 2031. Earth Observation will drive $7 Billion, or more than 30% of that growth. While emerging plays focused on delivering space situational awareness grab attention and headlines, delivering insights for actions on Earth continues as the leading driver of application revenue growth.

Future growth in EO service revenues depends on the integration of cloud activities within the ground segment. As space data becomes more available, a noticeable increase in activity in direct cloud connectivity via satellite is on the rise. Overall, as more uses for Earth Observation expand and utilization of this information in data processing pipelines increases, these ‘mass market’ plays will drive revenues into the space economy.

Direct-to-Device is a “Pie Growth” Opportunity within Mobility Markets

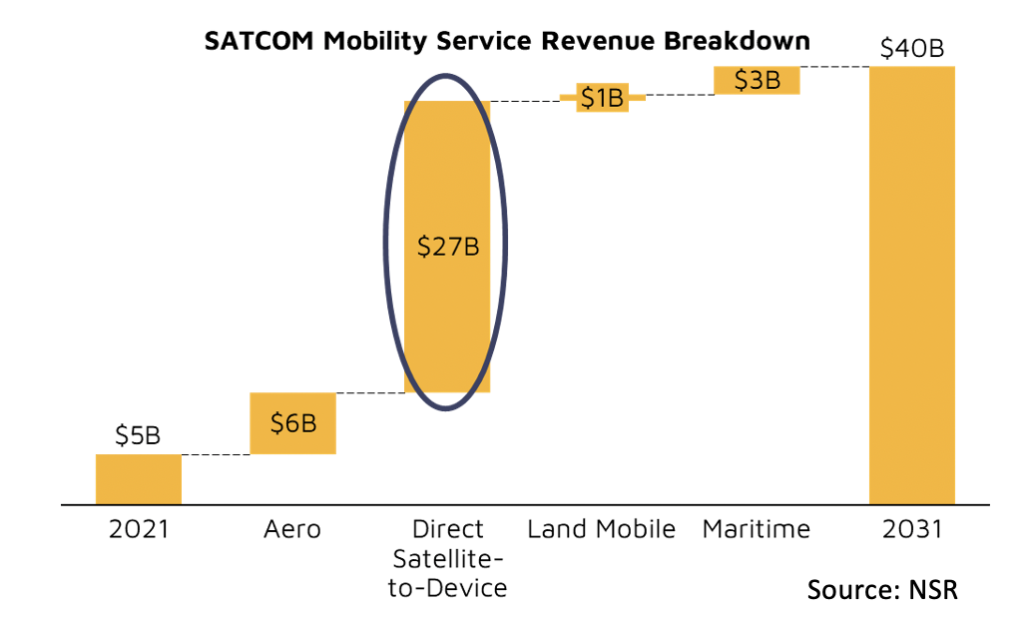

The Satellite Connectivity (SATCOM) market stretches from broadband access, enterprise data, and mobility, with mobility holding most SATCOM service revenues. Mobility is a highly attractive SATCOM market for the next decade, which by 2031 will be a source of USD$ 40B. The main driver behind mobility is D2D, contributing USD$ 27B, with a downstream market growing to 374 million average monthly users by 2031. Telecom and prime space companies have taken note, forming partnerships with companies such as Lynk, AST Space Mobile, Apple/Globalstar, and SpaceX/T-Mobile.

Changing infrastructure investments are altering the next generation of connectivity services. Services within D2D are growing rapidly through virtualization and cloud, as mainstream devices will incorporate the capacity to communicate with satellites. D2D emerging markets are in Asia and MEA, as they are underdeveloped in terrestrial infrastructure, but will soon have constellations offering capacity.

The Bottom Line

Investments towards cloud services and space data traffic efficiency is showing return and is driving partnerships for the mobility and EO ecosystems. Service providers will need to position their infrastructure investments today to capture these services-centric business models tomorrow. In short, service revenue streams will see the largest jump in revenue over the coming decade as more partnerships and product launches occur in D2D, and space data demand grows in EO.