Space to Bridge Digital Divide in Middle East and Africa

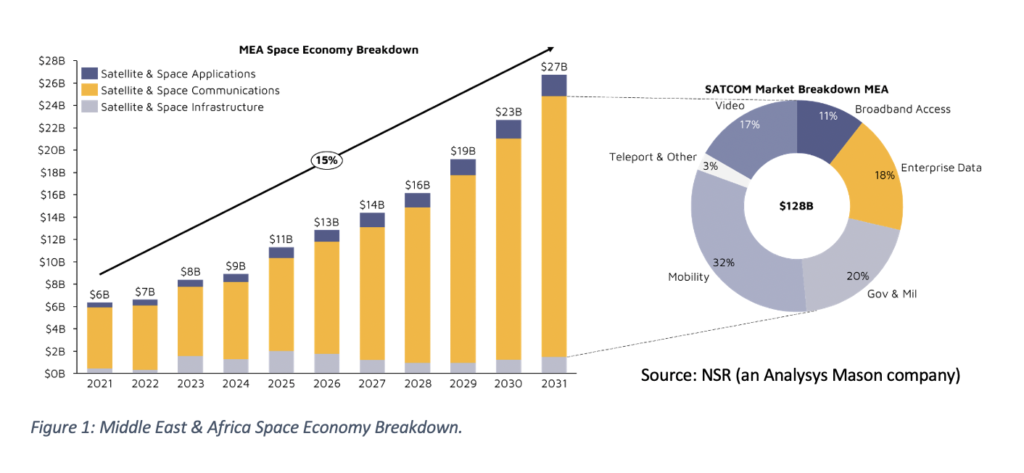

Government spending and partnerships in space have helped to decrease the digital divide within Middle East & Africa (MEA). Despite those efforts, according to the ITU, only 13% of Africa’s population has connectivity. In reaching the other 87% in Africa and the Middle East, the region will see a 4.5x growth in annual revenues from 2021 to 2031. The growth is driven by a combination of government-focused investments and private industry businesses almost exclusively focused on the satellite connectivity markets. Overall, satellite connectivity will account for more than 80% of the region’s revenue opportunities, and the MEA region overall will exceed $ 150 Billion in cumulative revenues from 2021 to 2031.

A SATCOM-centric Opportunity in Region

As highlighted in NSR’s Global Space Economy, 3rd Edition report, 5G and the direct to device (D2D) market will push growth in the region. Connectivity is key for any growing economy, and reducing barriers in connecting the last-mile across a range of traditional or novel use-cases drives these opportunities. With D2D a core component of the Mobility SATCOM segment, other connectivity opportunities will come from ongoing government and military connectivity focused on security missions. Overall, the D2D play will connect 39k handhelds in 2023 when services are expected to begin and grow to over 209 Million devices by 2031.

Key Opportunities

An underdeveloped ground segment needs to be addressed as it will slow the emergence of connectivity. Data demand has risen as mobile data usage has increased since smartphones penetrated the market. Terminal vendors must produce cheap and sustainable satellite ground segment packages to suit this region. As the market is largely focused on connecting previously unconnected, these are largely ‘net new’ opportunities for terminal and ground segment providers.

Ongoing government investments to help bridge the digital divide. Investment towards the ground segment and partnerships with SATCOM providers are key opportunities for the satellite sector to help meet ESG goals within the region. This will lead to the decrease of the digital divide, as remote locations can access online education, and enterprise connectivity to improve local economic opportunities. Local and foreign government partnerships are already investing in Middle East and Africa’s SATCOM markets such as Algeria – ALCOMSAT1, Angola – AngoSat1&2, and Togo – Vizocom satellite support, amongst others. Commercial bodies such as Microsoft is partnering with Liquid Intelligent Technologies to provide Internet through its “Airband Initiative” to breakdown the digital divide for 20 million people in Africa.

Key Recommendation

A Cost-first approach – The industry needs to address the cost of ground segment through both new technology and tried and true infrastructure. Ground segment development is slow, but cloud architectures can lower the total cost of ground infrastructure. GEO solutions such as parabolic VSAT antennas will continue to be a key technology over the next few years combined with GEO-based connectivity infrastructure. While emerging technologies such as Flat Panel Antennas can bring game-changing capabilities or shift installation CAPEX into OPEX budgets, they are still maturing technology. For details and dynamics read NSR’s Flat Panel Antenna report.

The Bottom Line

Government investment in both SATCOM coverage and ground segment is key to MEA’s flourishing space economy. Breaking down the digital divide in the region will lead to significant economic prosperity, and it is only through the partnerships of telecoms and SATCOM service providers together that such opportunities can come to fruition.