The Changing Satellite Supply Chain

The COVID-19 pandemic triggered a slowdown of most operational activities along the satellite manufacturing value chain. In the early pandemic days, manufacturing facilities had to put their activities on hold, and launches were delayed due to the interdependence of actors in the supply chain from both sides and the restraints put on personnel movement.

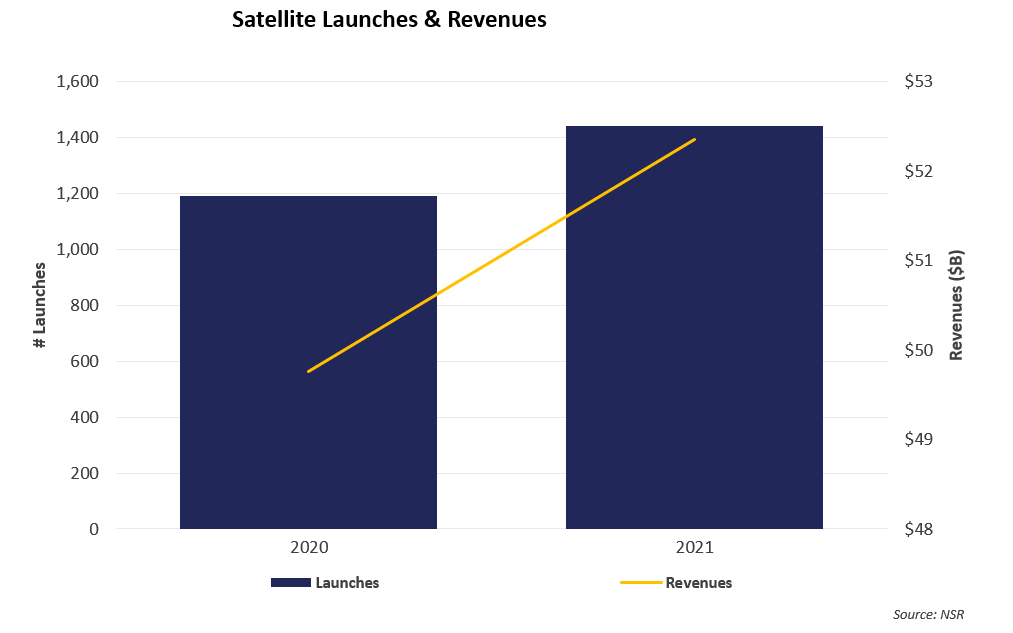

This had an impact on revenues, and NSR Global Satellite Manufacturing and Launch Market, 11th Edition report shows that 2020 orders and launches were pushed to 2021 and potentially beyond. Indeed, an increase ~250 more satellites to be launched this year (vs. 2020) is expected, with overall revenues associated with the Launch and Manufacturing Markets expected to rise by $2.4B. The gaps in commercial revenues created throughout the pandemic are expected to be filled via government and military orders and via operators getting ahead of expected delays by pulling forward project planning cycles.

For many organizations in the value chain, starting at the component supplier level, reaching all the way to satellite & launch operators, they continue to suffer the rolling effects. With launches delayed due to shortage in liquid nitrogen, and SpaceX and other launch players experiencing propellant diversion from launch pads to hospitals, there are now concerns as to whether the supply chain has been robust, financially secure, and ready to mitigate risks under uncertain circumstances.

In-House Model

Despite this, there is sustained demand for satellite services, and mission operations have been preserved and facilitated through remote working and workaround with split teams onsite. The market saw a large uptake in funding due to renewed financing vehicles such as SPACs and extensive venture capital invested that strengthened the space value chain. And this extra liquidity created a new path to innovation that many manufacturers have taken in-house. Some satellite operators (especially new entrants) have improved their skills on advanced manufacturing techniques, and taken the leap to move their manufacturing operations in-house and cut out the middleman.

This new operational mechanics have transformed the demand expected to be serviced by major component suppliers. With the sheer demand by new operators set to increase, capacity has led to an overburdened supply chain.

The ambitions of manufacturers have also created a gap in the launch market – with the pandemic continuing in some places and unavailability of key components increasing risk in matching the launch cadence required in the coming quarters. Due to continued obstacles in the supply chain – companies like SpaceX, Arianespace, ULA, Rocket lab, and others are undertaking new business models to stay above deep waters by building new relationships with suppliers directly, while simultaneously focusing on acquisitions to reduce disruptions and fasten the revenue generation. In simple terms, the value chain is already undergoing a consolidation cycle, which will continue in the coming years.

Bottom Line

The rise of satellite order and launch demand, for the sheer numbers in Non-GEO alone, has led to new cracks in the industrial supply chain. The COVID-19 pandemic revealed issues in the supply chain: at the beginning, it was the extensive use of teleworking, industrial and launch site shutdowns, lower-level disruptions both in supply chain and in working, payment delays and orders between customers and companies.

However, as the pandemic continues – the layers of issues continue to unfold with many delaying launches by several months, leading to reduction and in some instances a halt in earnings for major companies.

NSR supports equipment vendors, service providers, satellite operators, end-users, public agencies and financial institutions in their technology and business strategy assessment and planning. Please contact info@nsr.com for more information