The “Other” Energy Satcom Markets

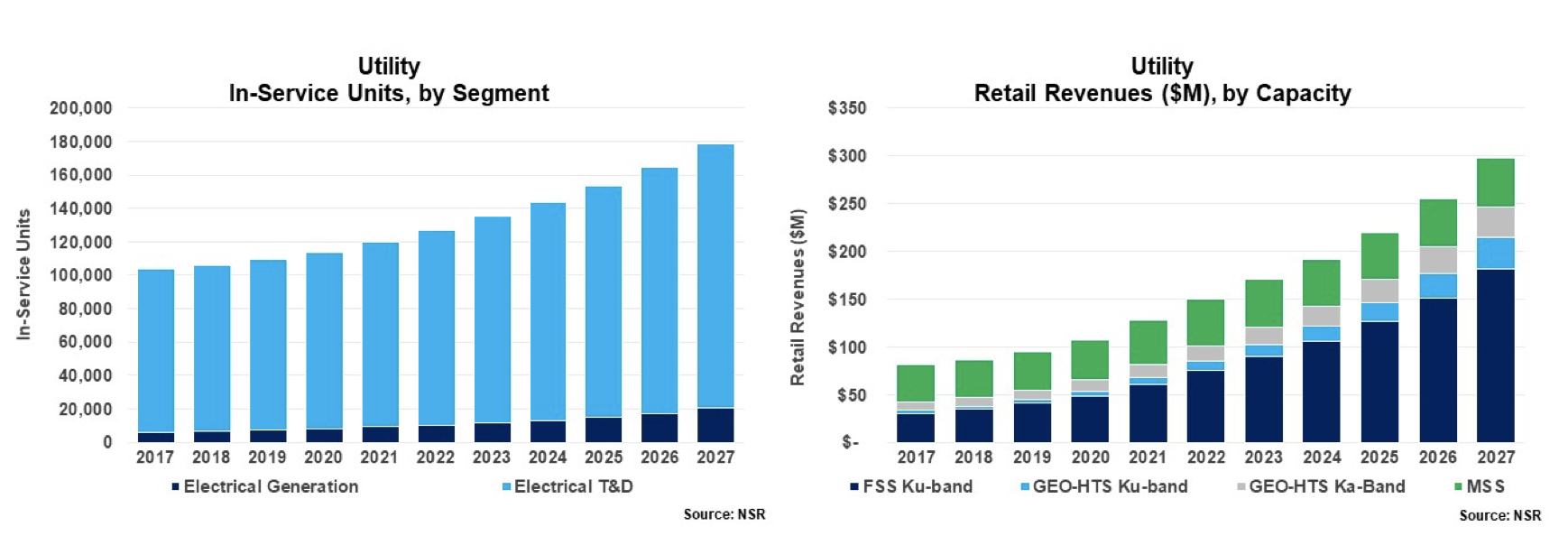

With attention in the Energy Industry typically focused on the Oil & Gas sector, it is sometimes easy to forget how satcom connectivity is shaping up in other sectors, such as Electrical Utilities. Utilizing 6 out of every 10 in-service units within the Energy satcom sector, the Electrical Utility segment continues to show signs of growth. While most of the market is focused on the Transmission & Distribution side of the Utility sector (enabling “smart grid” applications), there is a growing opportunity to connect Generation assets via satcom.

Marlink’s recent announcement of connecting a hybrid wind, storage, and conventional generation facility in Chad is one such example. The project aims to enable Amdjarass, Chad to become the first city in Chad to be powered by 100% renewable energy – a growing trend in cities across the developed and developing world. Working with the Vergent Group (who is a wind turbine manufacturer), the connection will help enable the advanced real-time analytics and other data-centric processes being implemented at the location. Continuing the trend of greater integration of renewable energy into electrical grids, robust and reliable data connectivity will continue to be a significant enabler.

In NSR’s Energy Markets via Satellite, 7th Edition, we found that overall, the opportunity for satellite connectivity in the Electrical Utility sector will rise from approx. $80M in retail revenues in 2017 to nearly $300M by 2027 – at a time when many other segments of the Energy sector struggle to find growth. Approaching or exceeding double-digit growth rates over the next ten years, increased bandwidth will be a key factor in driving additional revenue growth. Not only providing mission-critical connectivity for monitoring and control, but as with the case in Chad, enabling email/voice/Internet connectivity for workers at the site will be another key driver of bandwidth and revenues.

While still mostly an FSS Ku-band play, supporting low data-rate applications in Electrical Transmission & Distribution segment, the growing need for higher bandwidth services at small and large sites alike opens doors for GEO-HTS options. Everything from real-time video conferencing to email/voice/Internet connectivity at remote sites is driving bandwidth demand. Yet, the big question remains – why are locations that are obviously connected to cities and other large population centers looking at satellite services in the first place?

The short answer is satellite technology is becoming cheaper and simpler. Kymeta has expanded relationships with FMC GlobalSat specifically targeting the renewable resource industry. With longer distances between the Generation location and the consumer with larger renewable resource projects, and an increasing reliance on data for reliable operations, the costs of satellite vs. terrestrial increasingly leans towards satellite. Simply, there is an increasing pressure on development costs for renewable resource projects and running fiber or terrestrial microwave can be expensive. It can also be unreliable. While there are some arguable security advantages that come with using satellite, improved reliability and cost are oftentimes the deciding factor.

Bottom Line

Although it will take almost 75,000 new units to reach $300M in retail revenues by 2027, opportunities such as the one in Chad are only expanding. As other renewable and non-renewable resource generation projects come online in the developed and developing world, the role for satellite connectivity in the electrical generation markets will only expand. The higher utilization of intermittent renewable resources in electrical grids pushes increased data and insights along the entire Utility chain – from generation to consumption. In all, with other segments of the Energy Satcom sector slowly recovering from a prolonged slump brought on by depressed commodity prices, Electrical Utilities provide a bright, growing satcom market to consider.