Unlocking Satellite Connectivity in Asia

The Satellite Communications market is at a critical stage with the change in dynamics across the value chain. Major changes driving the markets include massive capacity supply, horizontal and vertical industry consolidations, increased need of connectivity post COVID-19 and relative reduction in regulatory barriers. With the evolving industry dynamics, stakeholders are looking for new opportunities for growth. Fixed VSAT opportunities, i.e., Enterprise and Consumer Broadband, in the Asia region is the major target that most industry players are strategizing to capture.

According to NSR’s VSAT & Broadband Satellite Markets, 21st Edition report, >25% of the total fixed VSAT service revenue opportunity will come from the Asia region, growing at CAGR 20.2% during the ongoing decade. But entering or expanding businesses in Asia will not be a laminar process due to varied country and sub-country level variables and challenges such as competition from regional players, regulatory barriers, political scenarios, lack of awareness, price sensitivity and unique customer needs & behaviours.

Country Level Trends

To arrive at the success factors for the Asia Fixed VSAT market, it’s important to analyse top country level trends in the region. Below are some of the major trends and expectations:

- India has been a tough market for entry and growth for a long time, primarily due to the regulations prioritizing national satellite capacity. But the country is one of the most attractive markets due to the addressability and quantum of unconnected population. Around 65% of the total population in the country lives in rural & remote areas, and 63% of the rural population are still unconnected. This translates into massive opportunity as the country’s total population is 1.38 billion. On the Enterprise VSAT side, the number of sites remained flat for some time but in recent trends, demand growth is witnessed for retail, banking and social inclusion use cases. Most players in the value chain are positive about the opportunities in India as regulatory change is expected around Q1 2023 that will most likely lower the entry or expansion barriers in the country by providing a level-playing field for private players.

- China is another massive market with 1.41 billion population. Internet penetration in the country is growing rapidly and is approx. 75% of the total population. As China is investing in its own capacity, the Satcom demand or the opportunity most likely will not be available for global industry players.

- Australia is a key market in the region, and NBN has been one of the major Satcom growth drivers in the country, especially for consumer broadband applications. Starlink has recently entered the market offering its product and services at subsidized prices as a customer acquisition strategy. On the Enterprise side, the market is witnessing increasing competition from terrestrial networks resulting in the churn of VSAT sites. The major positive factor about the country is relatively lower price sensitivity, if compared to other Asian countries.

- Indonesia has been the top growth market in the region driven by the BAKTI program. The major growth is witnessed on Social Inclusion sites such as connecting schools, health centres, etc. The country’s geography is well suited for the deployment of Satcom services, and with government programs driving deployments, demand is growing rapidly. But the expectation in the country is to increase the bandwidth provisioning per site and reduce prices significantly in the coming years (in some cases up to 50% of existing $/Mbps/Month). One major challenge that NSR foresees is the launch of the Satria satellites, as this capacity will be prioritized and hence the private players such as SES, Kacific, etc. may face some challenges in the long term.

- Philippines – 1 million people who live in The Philippines’ islands are either not connected by submarine fiber or are outside the range of a microwave connectivity link. Also, the digital divide program is one of the primary reasons driving VSAT growth in the country. Incumbents are partnering with regional players targeting social inclusion sites. For example – SES partners with ComClark Network and Technology Corporation to deliver educational content via Satellite to over 2,000 Schools. Also, in a recent development, Starlink announced its intent to deploy services in 2023. The political and regulatory environment are the major hurdles in the country that is limiting growth in the near term.

- New Zealand is a small market in terms of addressability with >90% internet penetration. Despite a relatively small opportunity, Starlink entered the market due to the ubiquitous nature of capacity deployment. Also, the other driving factor is higher ARPU ($159) and equipment price ($1040)

Other key markets in the region are Japan, Thailand and Malaysia. The growth in the region is restricted now due to capacity constraints in the HTS bands. As more capacity is added and pricing moves closer to $50/Mbps/Month, demand elasticities will be unlocked.

How Large is the Asia Fixed VSAT Market?

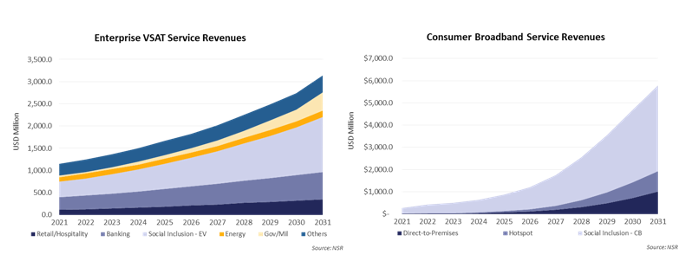

Undoubtedly, there are a wide range of trends governing the Asia satcom market. How do these translate to the cumulative market opportunity in the region? NSR’s VSAT and Broadband Satellite Markets, 21st Edition report estimates Asia fixed VSAT service revenues to be $43.6 Billion during the 2021-2031 period. Despite price declines, Enterprise VSAT revenues are projected to grow at a CAGR 10.6%, and Consumer Broadband is estimated to grow at an astounding 35.9% CAGR. The Consumer Broadband segment is projected to witness growth acceleration starting in 2025-2026

as more satellites such as Viasat-3, Kacific-2 and other HTS capacity both in GEO and Non-GEO are added into the market. Also, the impact of reducing regulatory barriers will start up thrusting the market during the same period.

Clearly, most of the Asian market is extremely price sensitive and hence government programs such as BharatNet in India, Bhakti in Indonesia and others are expected to drive the majority of growth for both Enterprise VSAT and Consumer Broadband markets. HTS capacity will most certainly play the key role in the penetration of service in the region.

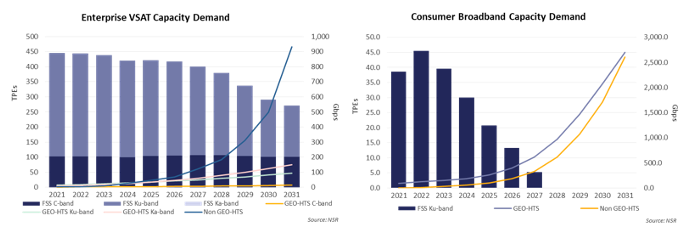

HTS capacity demand is forecasted to ramp-up to 6.5 Tbps by 2031 with >80% demand from Consumer Broadband use cases. Comparing GEO Vs Non-GEO-HTS, Non-GEOs are projected to play an important role as Starlink is expanding in the region and Bharti plans to deploy OneWeb services in the region soon. Other Non-GEO additions are expected during the mid-to-long terms. The overall capacity demand for GEO and Non-GEO will be similar as NSR expects prices (capacity & service) to converge in the long term. FSS for the Enterprise VSAT market will continue to remain relevant during short and mid-terms as ramp-up in demand per site counters the churn to HTS or terrestrial networks.

The Bottom Line

So, what does it take to unlock Fixed VSAT demand in Asia? Undeniable demand exists in the market as a large part of population in the region is still unconnected. Although demand existed in the region, the market capture has been significantly lower. Despite being one of the largest continents both by geography and population, the region contributes only 7% of subscribers in the Consumer Broadband segment and 24% active sites in the Enterprise VSAT segment. The major reasons for low capture in the region have been because of regulatory challenges, scarce HTS supply and a fragmented market. However, the scenario is changing as regulatory barriers are relaxing and with added supply coming in, prices are likely to align with the end-users’ affordability.

Analysing different trends and opportunities that are key strategic imperatives for Satcom Stakeholders in the region are:

- Target key markets in the region such as India, Indonesia and the Philippines. For example – target various government driven programs in the near and midterms.

- Build country specific strategies to address regulatory, supply chain and pricing challenges.

- Optimise the cost of offering services as the market is likely to become highly competitive in the coming years.

- Identify gaps in the capabilities and markets. Address them through regional partnerships.

- The focus should be on arriving at an appropriate pricing and addressing the demand. To achieve this, the strategy could be multi-orbit, GEO-centric or Non-GEO focus as end-users generally care about the service quality, not the orbit.

Overall, NSR predicts the untapped opportunity in the Asia region will eventually increase competition in the next few years as more capacity is added over the region. This will translate into Asia evolving as one of the highest revenue opportunity regions by the end of the ongoing decade.