A Land Mobile Satcom Duel to Behold

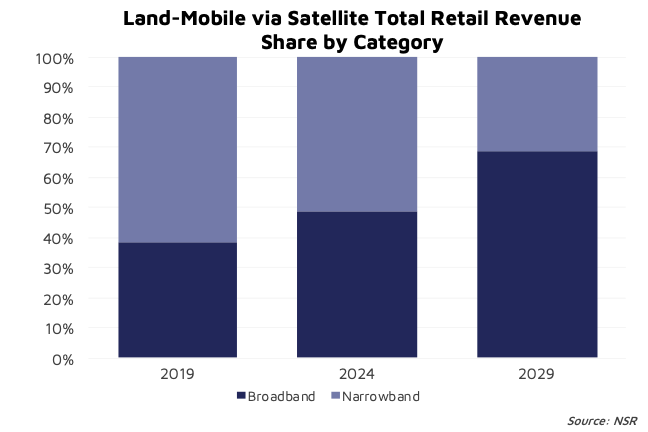

The land mobile satcom market has traditionally been comprised of handheld phones; however, an increasing number of new devices have appeared on the market. Fixed voice, followed by push-to-talk, satellite hotspots, and then consumer handheld devices took hold. While each of these markets will experience steady growth (traditional handhelds aside), prospects and growth trajectories here will remain stable. One trend is noteworthy, however. NSR found the Land Mobile via satellite will reach an inflection point where the change in the revenue mix will undergo quite a profound shift from narrowband technologies to broadband platforms and use cases. So, what does this mean for satellite operators and services providers? Is a major strategy and technology shift required?

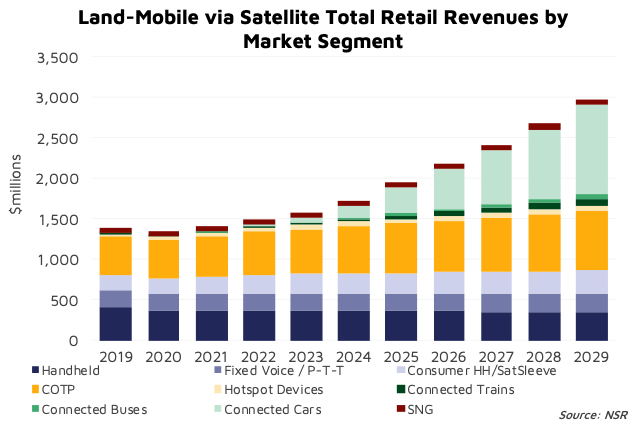

NSR’s recently published Land Mobile via Satellite, 8th Edition report found that total retail revenues will increase from $1.39 billion in 2019 to $2.98 billion in 2029, a growth rate of 7.9% across the decade, despite moderate COVID-19 impacts in the short term. However, this overall growth projection hides the two separate broadband and narrowband markets. And although broadband opportunities are strongest moving forward, targeting both markets will be key to optimizing future revenues.

Narrowband Markets

Narrowband markets will see a slow and steady, but continuous growth over the coming decade, especially as users become more price sensitive. However, handheld usage has declined with customers asking for more versatile form factors. A key representation of this for example, is that Thuraya announced that the Thuraya XT Pro Dual has reached end of life, with the company encouraging future customers to buy the Thuraya X5-Touch instead – the Thuraya android smartphone. A smart strategy, however the increasing consumerization of tech can be risky, with short-term revenues stalling due to travel restrictions and product distribution challenges associated with COVID-19. This is still better than the poor choice of giving up on the market completely which can lead to a decreased sales funnel to other form factors.

With COVID-19 ongoing, consumer discounts must be offered, including Globalstar getting anxious and offering unlimited data for $50 per month for a limited basis after revenue declines on SPOT in 2019. While compelling for end users, this is not expected to lead to long-term customer acquisition given the irregular usage of the product. Discounts for other MSS devices, such as hotspots and push-to-talk services, are not recommended with such a strategy not likely to boost demand for devices in the short term. Recent rate plan increases have had larger impacts to active subscribers, indicating the higher level of price sensitivity to narrowband land mobile applications – both enterprise and consumer.

While pricing options to boost revenues remain limited, dropping these narrowband and discount-reliant products altogether remains ill-advised, and will leave revenues on the table. With greater revenues available elsewhere, a long-term core strategy as a service provider solely serving these markets is thus one that will not pass muster with investors for much longer. Narrowband M2M and IoT, on the other hand (not counted in this data), does remain higher growth and does need to be part of any future strategy.

Broadband Markets

Instead, operators are positioning themselves towards emerging and more lucrative applications – IoT/M2M in particular, but also investing in broadband land mobile applications. Iridium for instance is developing new products and a strong pipeline for higher bandwidth Certus devices. These devices will be much more acceptable to the user in 2024 than today’s devices, which are used more begrudgingly by consumers. A further technology shift on FPAs will also re-think operators strategies to target new COTM applications.

While growth is expected across all broadband land mobile segments resulting in a four-fold increase in revenues over the coming decade, it is the Connected Car that is the standout performer and expected to become a $1 billion market in 2029 – it is this market that will require the largest technology and strategy shift. While the satellite Connected Car has been talked about for years since Kymeta’s deal with Toyota back in 2016, there are now strong signals that from 2024-2025 and onwards, sizeable revenues will start to be generated. No, every car coming off the production line won’t be satellite connected, but luxury and first responder users will be.

And yes, shifting to a service model through car manufacturers for broadband land mobile is more complex and has more components in the value chain than traditional handhelds. But it needs to be done, and the greater value proposition achieves greater revenues and profit margins. Such is the potential for broadband land mobile that new constellations are being planned specifically to target this market, and operators need to watch out. This includes new announcements from Geely for their constellation targeting connected vehicles. Such a vertically integrated model could lock out existing satellite operators from the key revenue generator of the next decade, so it is critical for operators to go hard and early on developing Connected Car tailored offerings.

Further, integrating new FPA technology early on is key for broadband growth, as it takes years for this to be incorporated into the vehicle production line and available to consumers. Taking a wait and see approach will lead to land mobile operators and service providers being stuck offering devices with increasingly outdated speeds and being reliant on terrestrial network investments to secure long term growth, a strategy which is yet to yield dividends for Globalstar.

Bottom Line

While narrowband devices have been the mainstay of land mobile satcom, higher bandwidth and higher ARPU broadband services will see a major land mobile shift occurring in the next few years. Service providers will need to begin to pivot away from traditional core businesses and towards offering newer types of services. This includes preparing to offer Iridium Certus compatible devices, COTP, COTM and connected vehicle services that are all critical to remain relevant longer term. For operators, partnering with and developing a greater array of ground terminals, FPAs in particular, will be required to capture increased interest in broadband land mobile.

This will be a key technology shift over the coming decade – a business model selling handhelds won’t cut it anymore, and being able to offer flat panel antennas, fly-aways, roof mounted antennas and backpackable connectivity must become the norm. Now is the time to pivot to higher bandwidth solutions to ensure a long term and sustainable revenue pipeline, or else risk being outdueled with profit margins, unit sales and ARPUs becoming squeezed over time.