The Next Step in FPA Evolution

Despite ongoing delays and market exits due in part to COVID-19, flat panel antennas (FPA) remain a hot topic for the satellite industry. It is especially true in the aero market, where almost half of all FPA announcements in the past year focused on government and commercial aviation.

Yet, there is another market that is slowly gaining ground: Enterprise. As FPA manufacturers find themselves stuck between the ultra-competitive aero market and the opportunistic, but challenging to meet, consumer broadband market, the Enterprise broadband market is fast becoming the next step in the evolution of FPA technology.

Recent announcements from companies such as ALCAN Systems, ThinKom, and Isotropic Systems demonstrate positive trends and continued progress in both the technological capability and pricing of FPAs for Enterprise solutions. But given the well-established parabolic-based VSAT market, and upcoming but uncertain Non-GEO HTS constellations, how will FPAs fare here? Will it remain a niche, or will mass consumer markets ever be reachable?

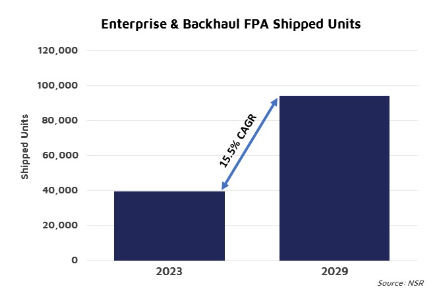

NSR’s Flat Panel Satellite Antennas, 5th Edition forecasts global, annual, shipments of FPAs for Enterprise and Backhaul solutions to reach 94,000 by 2029. While a virtually non-existent market today, NSR expects the first shipments to roll out in 2022/2023, strongly driven by the commencement of SES mPOWER’s operations. However, the market is quite a mixed bag.

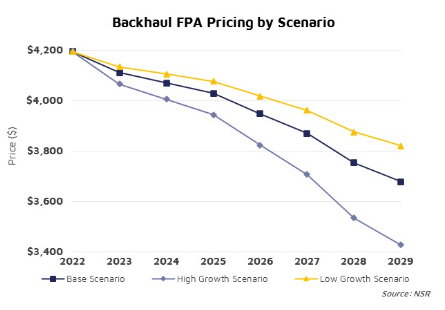

Significantly lower pricing tolerance in both markets results in Enterprise and Backhaul only representing a $167M cumulative equipment revenue opportunity over the next decade, or, roughly half of what FPAs sales are expected to generate in commercial aero for 2020 alone. Yet, the pivot toward Enterprise-like solutions is important, as it represents important strides to wider applications, such as consumer broadband.

Last year, only 8,000 FPAs were manufactured and shipped globally. These focused almost entirely on mobility, with government and commercial aviation representing nearly half of the opportunity. Currently, Enterprise and Backhaul HTS solutions mainly use parabolic equipment, which is generally much lower-priced, and highly performance-competitive, compared with FPA technology. NSR research found that Enterprise solutions exhibit strict SLAs, requiring over 99.5% connectivity, and high throughput. Backhaul solutions on 4G require > 100 Mbps, with terminals capable of at least 3.5 Mbps/MHz efficiency, which is roughly an order of magnitude higher than most FPAs proposed for fixed applications today.

Pricing also represents a significant challenge, with different tolerance across tiers of service. Small to medium Enterprise customers are unlikely to pay more than $1,000 per terminal today, whereas energy, gov/mil, and backhaul Enterprise solutions may be willing to go higher, provided the equipment meets stricter performance requirements.

While not making as many headlines as for aero, several manufacturers have been quietly developing equipment for Enterprise solutions, aiming to provide the scale necessary to cut costs and better serve the upcoming Non-GEO HTS market. Parabolic equipment will still hold sway in most GEO-HTS markets, but NSR expects that the majority of smallcell backhaul and Enterprise solutions for Non-GEO HTS will be served by FPAs. These smallcells aim to provide better coverage, speed, and capacity than macro cells, especially in Latin America, South-Saharan Africa, and Asia for rural connectivity, and to help improve coverage for first responders.

Bottom Line

Flat panel antenna technology, much like the greater satcom business, is undergoing an evolution in both form factor and (expected) performance. Manufacturers, service providers, and satellite operators alike are aiming to move the industry from a concentrated focus on premium, niche, used-when-necessary markets such as aviation, to a more widespread adoption, eventually catering more heavily to the tremendous consumer broadband addressable market.

In order to get there, FPA technology will need to become far cheaper, and prove its reliability in serving Non-GEO HTS capacity. Scale has long been cited as the way forward, but in order to get there, FPAs must strategically balance price and performance to build up the industry. Strategically targeting Enterprise solutions necessitating Non-GEO HTS connectivity, in both higher-end and smallcell capacities, will allow the industry to improve customer distribution channels, manufacturing practices, and be the stepping stones FPAs need to move from the mere thousands sold per year in aero to the millions shipped to consumers.