Aero IFC- Near-Term Turbulence but Long-Term Smooth Air?

After a few years of incremental growth in the In-flight Connectivity (IFC) market, COVID-19 has derailed the segment’s momentum for 2020 and beyond. According to the NSR’s COVID-19 survey results, mobility segments including aviation and maritime are the worst hit satcom segments amid the ongoing pandemic. Aviation and related industries nosedived with greater than 50% drop in passenger air traffic in March 2020. The situation persisted in April 2020, with slight but uncertain improvement, translating into mounting survival and future revival challenges across the value chain. The series of recent bankruptcies or exits across the value chain, such as Avianca, Virgin Australia, Intelsat, OneWeb and Phasor is a clear indication of these challenges.

Also according to the NSR’s Aeronautical Satcom Markets, 8th Edition report, despite the U.S. aviation stimulus package relief, the market difficulties are likely to remain for an extended period. This is likely to occur as pandemic progression results in continued grounded aircraft and financial pressures on airlines, OEMs ramping-down aircraft production rates, economic slowdown scenarios, and possible flying hassles & psychological resistance deterring travelers.

What is the Immediate IFC Impact?

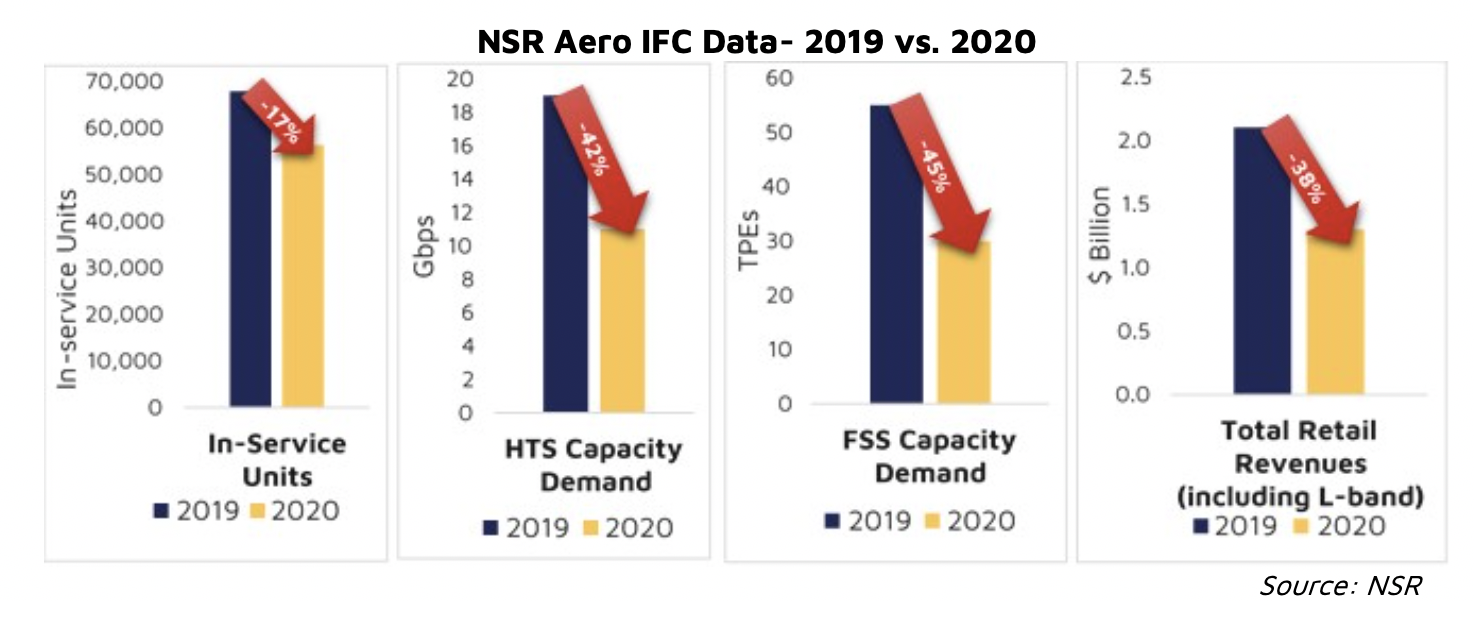

In comparing 2019 and 2020 across satcom forecast variables, NSR estimates a certain descent for in-service units, capacity demand (FSS & HTS) and revenues (equipment & service) during 2020. Satcom IFC in-service units (cockpit + cabin) are expected to reduce by 11,500+ units, primarily owing to the dwarfed operations and grounded aircraft in the commercial aviation segment. Also, irrespective of the contract type, these grounded aircraft are likely to generate little to no ARPUs/ARPAs to service providers. In a recent trend, with only few weeks (out of a quarter) into the pandemic, GoGo witnessed a decline of ~8% in its consolidated revenues in Q1 2020.

NSR Aero IFC Data- 2019 vs. 2020

The IFC market decline is likely to continue in the ongoing and upcoming quarters and as a result, service providers will be forced to (re)negotiate their upstream capacity lease contracts (fixed cost), impacting satcom capacity demand and/or satellite operators. NSR estimates IFC satcom capacity demand to drop by 42% & 45% for HTS & FSS, respectively. On the equipment side – with OEMs shrinking their production rate, the immediate impact will be on line fit equipment revenues. And for the contracted retrofits (upgrades or new installations), the immediate outcome will include cancellations and many executions being pushed to the right in terms of timeline. Overall, NSR estimates total retail revenue (equipment + service) will drop by 38% in 2020.

Certainly, no surprise there, but it is useful to quantify the impact.

But apart from stating the obvious and quantifying losses, the bigger and more important questions are: When will the market recover? And how will it evolve in the mid- and long-term?

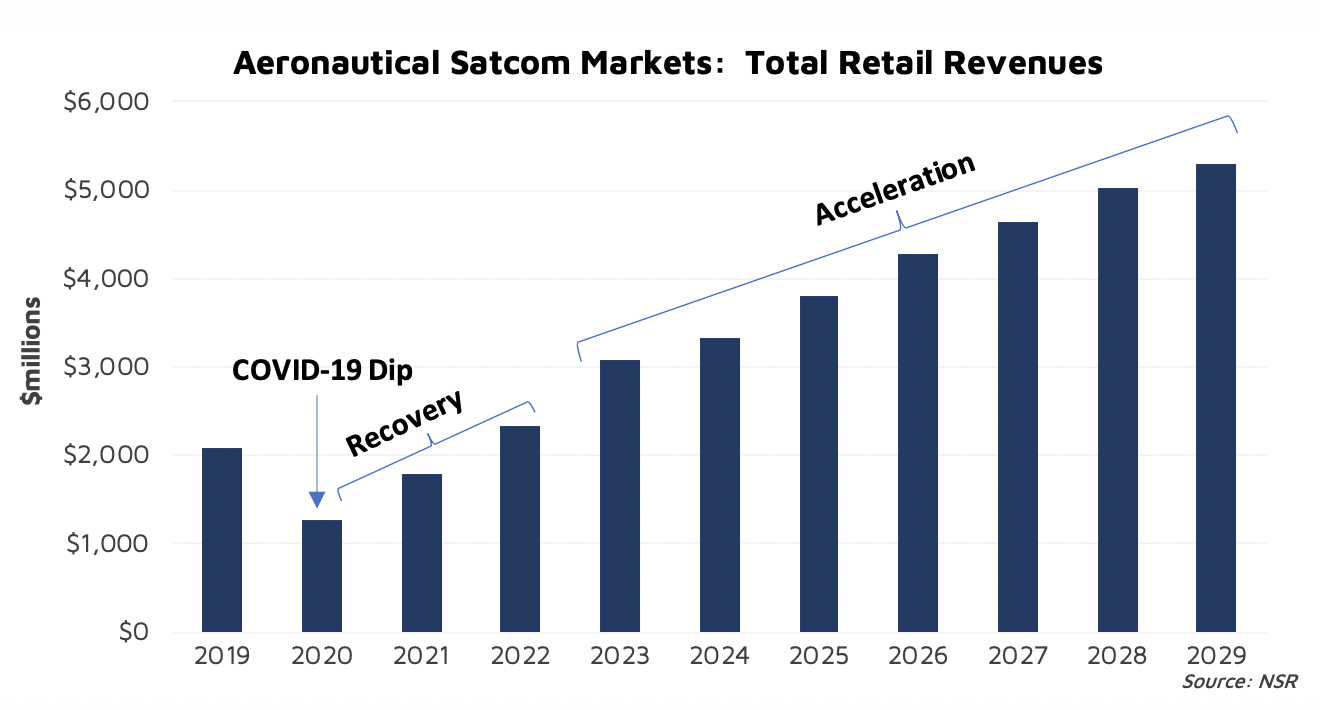

NSR estimates the market recovery period to be approx. 18 to 24 months. The market is expected to return to 2019 revenues (or pre-COVID levels) not earlier than 2022. Already in 2020, the industry has witnessed multiple exits across the value chain, and the trend of market exits or consolidations (vertical and horizontal) is likely to propagate to the mid-term. However, in the long term, the IFC market fundamentals remain strong. For the North American Commercial Aviation segment, GoGo witnessed a drop in take rate from 13.9% in Q1 2019 to 13.3% in Q2 2020. But take rates remained higher than the average take rate of 13.2% in 2019. Granted, aircraft are flying at a fraction of their previous passenger loads, but current usage data validates the market fundamentals: more data per passenger will be consumed but during the pandemic period, the falling load factor will continue to shrink overall revenue. Also, the free-service model (to be delayed) will ramp-up take rates, especially post 2022-2023, further supported by the influx of cheaper per Mbps capacity from efficient satellites like ViaSat-3 and Jupiter-3. As such, once we cross the pandemic impact trough, the industry fundamental of more data consumption and free service models will accelerate market demand and revenues. And hence, despite the COVID-19 dip, NSR forecasts $36.9 Billion in IFC cumulative revenues at 9.8% CAGR during the period 2019-2029.

Bottom Line

COVID-19 is making IFC a bumpy flight, so IFC players need to fasten their seatbelts until the market turbulence has subsided. But it is just that – a bumpy flight, not a market crash that will stop the industry in its tracks.

These are challenging times for the aero satcom market, most certainly where financial pressures on airlines will cascade to the IFC value chain players’ topline. The COVID-19 impact is SEVERE for aviation and related verticals, resulting in multiple exits, restructuring and consolidations, especially in the short and mid-terms. No link in the value chain will remain immune to the pandemic impact in the IFC market.

But in the mid- to long-term, the industry will witness demand acceleration, resulting in rapid revenue growth. So, what is the strategic imperative for IFC satcom stakeholders now? The aviation industry is transforming and will further transform both at macro (i.e.: Avianca & Virgin Australia bankruptcies) and micro levels, catalyzed by the pandemic. It will become more price sensitive than ever and seek more flexible solutions/contracts. For a longer growth trajectory, IFC satcom stakeholders must accordingly align their products/services to maximize value to end users, i.e. lower cost per Mbps and high bandwidth solutions, through either system/network level innovations or consolidation (vertical/horizontal) or both. In the mid-to-long term (i.e. 2022-2029), the industry fundamental resonating with large capacity supply will result in a massive opportunity of 16x growth in HTS capacity demand. Ubiquitous, reliable, flexible, and cheaper solutions layered onto the aligning HTS capacity and low-drag, power efficient & high throughput hardware could be an ideal go-to-strategy for a mid-to-long term sustained success.