Buses and Trains: Completing the Mobility Trifecta?

NSR, An Analysys Mason Company, recently identified that RVs are the “true” satellite opportunity for broadband connectivity for “anything with wheels”. With satellite operators still trying to work their way into the huge vehicle market more generally, and the aero market continues to see huge growth, we continue to get asked: how can satellite operators translate the success of aeronautical satcom to buses and trains?

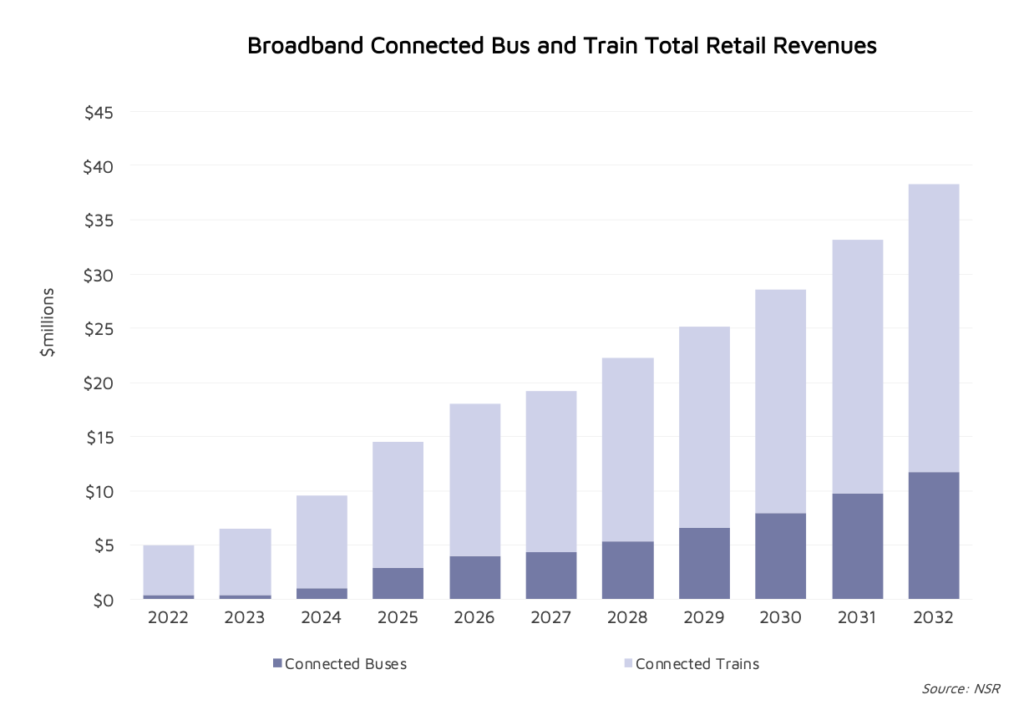

NSR’s recently released Connected Vehicles via Satellite report, found that broadband connected trains and buses combined will generate just under $40 million in retail revenues annually by 2032, weighted heavily in favor of trains. With the overall connected vehicle market expected to generate $677 million in retail revenues that same year, why is the share for trains and buses so comparatively small, for a market that seems “so obvious” to some?

Considering the cost of appropriately configured satellite terminals cost tens of thousands of dollars for trains, most railway operators (with a notable exception of Renfe in Spain) are continuing to take a “wait and see approach” for satcom connectivity, with an eye on prices, terrestrial network buildouts, and Starlink. And even still with Renfe, the MNO Telefonica has installed terrestrial network towers along over 1500 km of railway track, indicating that this continues to be the preferred mechanism for passenger connectivity. While Capex is greater, the benefit to reliability, capacity availability and lower OPEX tips the scales in its favor.

For potential intercity bus satcom connectivity, the challenge is even greater. Some satellite terminals can cost more than the bus itself, and bus operators are less likely to have engineers ready to deal with long-term maintenance and support – making this more challenging than connected trains. Furthermore, with only 20-30 passengers per bus on average, compared to typically hundreds on trains, this vastly changes the pricing dynamic.

One bright side is that when passengers first alight intercity buses and trains, operators find that customers always ask “what’s the Wi-Fi password?”, indicating that there is in fact underlying demand for connectivity.

Willingness to pay – not so much

Especially when vehicles typically pass through cellular network coverage from time to time, except in the most remote journeys, which changes the value proposition of connectivity immensely, away from the “all or nothing” experience in aviation.

While the challenges are huge, there is change ahead. Existing installations are typically using FSS Ku-band, but longer-term, through larger players Starlink and OneWeb, will provide an opportunity for growth, which will benefit through lower terminal pricing through mass scale of mobility terminals. In fact, this is already starting to happen, with Lithuanian railways announcing a pilot program to test Starlink on one of its trains, as well as Ukraine’s Ukrzaliznytsia railway corporation. All eyes will be on these operators in the coming months.

The Bottom Line

Buses and trains present huge challenges for broadband connectivity. Technical challenges are one thing, but from a strategy perspective, it’s all about terminal pricing. This is especially the case with much lower cash flow seen by bus and train operators compared to airlines, and a “race to the bottom” on fare pricing often the case.

With the only way to get to terminal pricing to anything remotely palatable is through scale, this means this is an almost entirely reserved for LEO-HTS operators. While technically this means Starlink and OneWeb will in time help complete the mobility trifecta, with land mobile passenger connectivity being the final piece, together with maritime and aviation, the end result is somewhat void of satisfaction, knowing that satellite will always be an ‘edge case’ for intercity buses and trains.