RVs Lead Connected Vehicle Market

For years the “connected car” has been the holy grail of broadband land mobile connectivity, with operators left and right trying to solve the market puzzle to get flat panel antennas (FPAs) on anything that moves. However, in 2023, this market has now finally become “real”, but not in line with the plethora of announcements of passenger cars over the past years, but rather, due to demand from recreational vehicles (RVs).

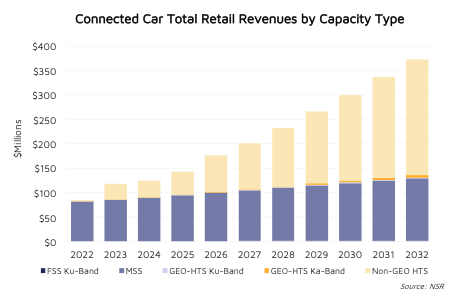

NSR’s recently released Connected Vehicles via Satellite report – the first into a deeper dive in this land mobile market – found that RVs are by the far the greatest driver of satcom connected cars, with $245 million in annual retail revenues driven by broadband connected cars in 2032, out of a greater (broadband and narrowband) $372 million car market.

Starlink’s market entry has singlehandedly accelerated connected vehicle development, with its recently announced (and then rebranded) service for RVs for much lower pricing than competitors, leveraging production at scale for terminals, as well as subsiding costs to attain higher market share. This is combined with a simpler sales process for end users, not to mention high levels of media visibility.

By comparison, Kymeta has offered its u8 terminal for some time for RVs amongst other applications, with terminal pricing at ~$30,000 plus hundreds or thousands of dollars per month for connectivity – providing limited opportunity for mass market non-enterprise users without clear problems to be solved.

NSR has long repeated the fact that there is no “key application” for regular passenger cars. RV users, by contrast, have clear and simple connectivity requirements – no proprietary OnStar type offering is being sought after, and no complex value chain and negotiations are needed. Further, with Starlink letting RV end-users pause and start service on demand, rather than mandating 24+ month contracts, there is more incentive for RV users to try the service than ever before. This is working extremely well for Iridium with its consumer handheld product line and is driving the company to new subscriber records.

Development of satcom connectivity for passenger vehicles, by comparison, is being hobbled by auto makers who want to control the passenger experience, providing locked down and locked in services to extract a cut of connectivity revenues, much like the mobile phones of yesteryear. This is most recently demonstrated by GM’s recent spat with Apple and Google on in-car services.

Instead, partnering with existing service offerings is the best strategy for RV and car makers. Thor Industries, for instance, following a finding that 74% of surveyed US RV owners found that high speed internet connectivity is extremely or very important for future RV purchases, announced that Starlink terminals will be integrated into their RV line-up as an option for new vehicle sales across Future Airstream, Jayco, Entegra Coach and Tiffin brands. Expect many more players to follow in their footsteps, especially as ‘work from home’ is turning into ‘work from anywhere’ for many.

The Bottom Line

Pent up demand, combined with lower terminal pricing has resulted in tens of thousands of terminals flying off the shelves and onto RVs in the past 12 months – clearly demonstrating that this is the only satcom consumer car market – no SiriusXM type partnership or contract required. Thus, unless you are laying the long-term groundwork for 6G and connected autonomous vehicles, the key strategy for satellite operators and service providers is to focus on the RVs over passenger connected vehicles, for now at least. And if reducing prices for mobility terminals is all too challenging, high-end enterprise markets are the next best thing.