Enterprise VSAT Strategy: Exploration or Exploitation?

The interplay between Exploration and Exploitation is critical for the long-run performance of a solution, company, or sector. Enterprise VSAT market revenues have plateaued with long exploitation of the conventional satellite connectivity offerings and hence, the industry had been in exploration for next-gen technologies, products or solutions to push the segment’s topline on the growth trajectory again. Luckily for the segment, COVID-19 has accelerated the exploration process with increased digital transformation across enterprises to optimize processes and reduce costs, thereby initiating the exploitation of next-gen technologies for possibly sustainable positive gradient growth. Following are the key technologies or solutions, which are likely to impact the long-term sustainability of the enterprise VSAT market:

- SD WAN: Software-defined wide area network (SD-WAN) decouples the networking hardware from its control mechanism, simplifying the operation and management of WAN. It solves the challenges related to high latency, packet loss, bandwidth limitations, and network congestion. In recent trends, SES Networks expanded partnership with regional ICT player with SD-WAN improving end-user experience and Gilat Telecom enhanced its SD-WAN systems unlocking huge network availability and bandwidth capacity across Africa.

- Cloud: Cloud usage across enterprise networks will be a key driver for increased bandwidth usage, as COVID-19 accelerated the trend of enterprises migrating applications and processing, which was/is typically hosted at the local network, to the cloud. Key partnerships, such as Microsoft’s Azure Space with SpaceX, SES KSAT, ViaSat, Kratos & others, are being executed in order to exploit the upcoming industry demand.

- Data Analytics: Undoubtedly, the industry is moving towards data-driven process optimization and decision-making. Data Analytics and intelligence will govern long-term success for all players in the value chain, from optimizing space and ground segments to enhancing operational and cost efficiencies of end-users. According to the NSR’s Cloud Computing via Satellite report, 52 exabytes of data is expected to be channeled via satellite by 2029. Energy, banking, and retail end-users will be the key demand drivers from the enterprise VSAT market for data analytics solutions.

- Edge Computing: Edge computing is critical where large datasets need to be analyzed for a latency sensitive operation. In such cases computing power closer to the operational site is used for execution. Integrated Satellite and edge computing solutions have been in use for a long time, such as SCADA, M2M/IoT etc. However, the requirements are evolving fast as enterprises are investing increasingly on digitization and automation.

- 5G: Wireless network upgrade in a region results in the stepped increment in satcom capacity demand. Even during COVID-19, many satellite operators witnessed up to double-digit ramp up in capacity demand from service providers incrementing networks from 2G to 5G. Wireless backhaul will be the major segment driving demand growth across regions with G-upgrades during the next decade.

- Private LTE: These are independent networks and hence do not have challenges from the congestion in cellular networks. The technology is well-suited for enterprise customers with critical applications, such as hospitals, airports, governments etc.

Among these next-gen solutions, the Enterprise VSAT market has entered the exploitation curve for SD-WAN, Cloud, Data Analytics, Edge Computing and Private LTE. 5G is in transition from the exploration phase to exploitation phase. NSR estimates that starting 2022, the exploitation of these technologies will gain momentum with multiple offerings from key stakeholders – in turn vectoring the capacity demand and industry topline on a growth path for the long term.

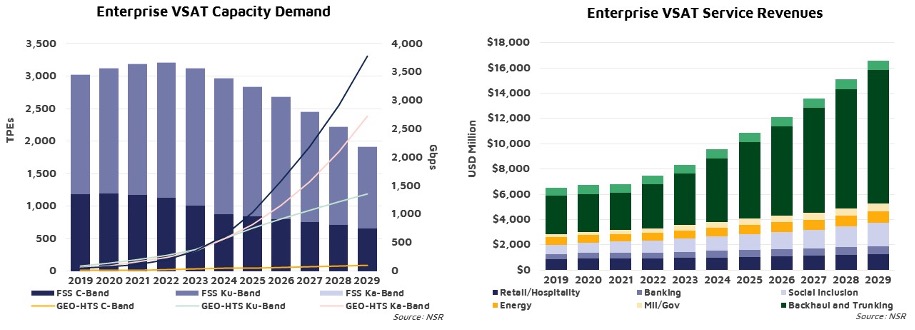

According to NSR’s recently published VSAT & Broadband Satellite Markets, 19th Edition report, GEO HTS capacity demand is expected to grow by 26x; i.e., from 161 Gbps in 2019 to 4.2 Tbps in 2029, generating a massive opportunity for the satellite operators. For Non-GEO players such as SES-O3b/mPower, SpaceX, Kuiper, and others – the Enterprise VSAT market will be one of the most attractive segments with a 53.7% CAGR and 3.8 Tbps capacity demand by 2029.

Conventional wide beam FSS capacity is expected to witness stable demand till 2022-2023 but post that with the infusion of next-gen technologies, the industry is likely to witness more migration to HTS owing to flexible offerings in terms of price and bandwidth by HTS based solutions. HTS capacity pricing (Ku & Ka bands) is expected to drop to $200-$300/Mbps/Month by 2029 for most regions and applications. Although it restricts per Mbps revenue generation but with increasing Mbps demand, lower pricing unlocking demand elasticities and the infusion of next-gen solutions are expected to drive both capacity and service revenues. NSR forecasts service revenue to grow from $6.8 Billion in 2021 to $16.6 Billion in 2029 at CAGR ~12%. Backhaul, among the Enterprise VSAT segments, is expected to contribute to >50% of the total cumulative revenue with the execution of network upgrades (3G, 4G, 5G), Cloud and data analytics integration. Conventional Enterprise segments, such as Banking, Retail/Hospitality, Social Inclusion & Energy, are estimated to generate >$4.6 Billion service revenue by 2029, with SD-WAN, Edge Computing, Cloud and Data Analytics driving growth. Revenues from Military/Government sites are also expected to turn-around with growth projected at CAGR ~12.2%.

Bottom Line

The industry is ready, in terms of technology and end-user requirements, to catapult the stalled Enterprise VSAT market on a growth trajectory of $113.6 Billion during 2019-2029, exploiting next-gen technologies and solutions. COVID-19 has been one of the key accelerators to end-users shifting gears to accelerate digital transformation, process optimization and automation. Other accelerators are dropping capacity pricing, key partnerships between Cloud service providers and satcom players, and overall technological advancements (software & hardware). The industry stakeholders across the value chain must quickly switch from the Exploration phase of “What’s next for better ARPUs” to exploitation of “Next-Gen solutions – SD-WAN, Cloud, Data Analytics, Edge Computing, 5G and Private LTE” for the long-run performance of the Enterprise VSAT vertical.