EO SAR: Trick or Treat?

It’s that time of year again. Autumn leaves, and children in costume, candy and ghosts around every corner. In our business, many days feel like Halloween, in a way. Companies emerge from stealth mode, try on different business cases, and venture forth seeking market validation. Market trends come and go, but the most popular, the scariest yet most exciting theme, is disruption.

In the satellite-based Earth Observation business, disruption has been cited as both necessary and impending, especially concerning the synthetic aperture radar (SAR) market. With imagery capable of viewing at night, and seeing through clouds, SAR reads like the ghost hunter’s story of satellites that offers more useful tasking opportunities than its optical counterpart.

Recent announcements from new companies in this space show the promise of disruption; from EOS Data Analytics and Umbra Lab announcing constellations to offer very high resolution SAR data at significantly lower prices, to companies such as Capella Space, Synspective, and Iceye aiming to disrupt the market with higher revisit, SAR monitoring services.

Their main premise: SAR stands a chance at toppling the optical dominance and providing huge returns. Given these announcements, should optical players be frightened, and as the market develops, are investors in SAR in for a trick or a treat?

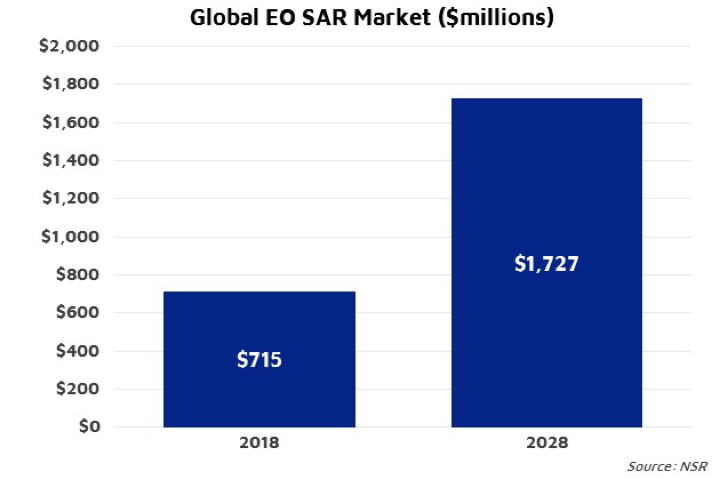

NSR’s Satellite-Based Earth Observation, 11th Edition report forecasts significant growth in global revenues from the sale of SAR data and derived products, from $700M in 2018 to over $1.7B in annual revenues by 2028. Imagery sales and Information Products will dominate, responsible for 63% of SAR revenues in this timeframe. While a traditionally gov’t/mil-focused market, that dominance will drop to 42%, diversifying among other verticals, with financial and insurance Services growing the fastest, at a CAGR of 14%.

The Trick

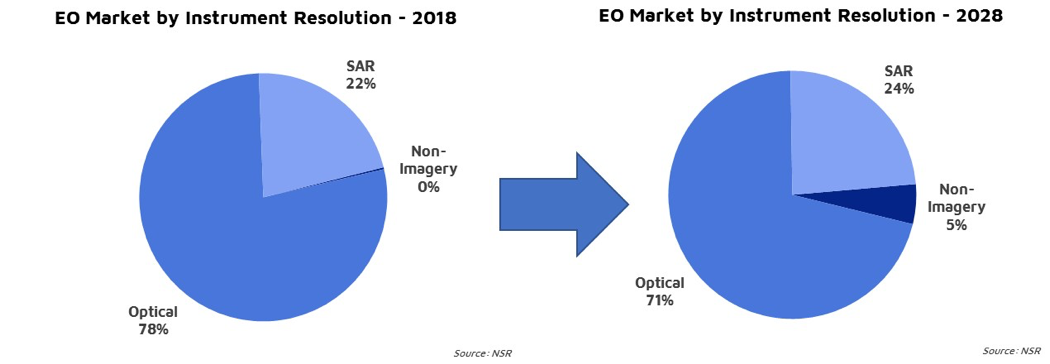

However, these trends are also affecting optical technology, products, and services, and NSR’s report finds that SAR’s global marketshare barely budges over the 10-year forecast. Putting aside the established and highly competitive optical market, there are several challenges facing SAR data and analytics suppliers.

SAR satellite missions have been traditionally more expensive than optical, involving an active sensor and larger platforms. Expensive missions often result in expensive imagery, with NSR finding that current and recent historical SAR prices ranging 3-6x that of similar resolution optical imagery. This expense creates a barrier to entry, limiting market potential.

Similarly, analysis of SAR data has not been cheap, requiring more time, expertise, and computational tools. Industrial image organizing and processing software was originally developed to suit the human eye, optical not radar, leaving SAR lagging behind and more expensive. Coupled with higher data prices, SAR data users has remained fewer, all looking to cut costs any way they can, even seeking out lower resolution or free imagery.

Finally, Sentinel’s freely available, 10m imagery, with its 6-12-day revisit, has proven quite satisfactory for the existing ecosystem of SAR data users. While this has helped grow the Big Data analytics opportunity by lowering the barrier to entry, it has limited the data sale opportunity.

The Treat

The good news is that it is changing. Similar to optical almost a decade ago, SAR payload and satellite technology is becoming smaller, and somewhat cheaper, and the idea of providing high-resolution global monitoring via SAR imagery is becoming more feasible, as a result. Iceye’s recent sub-meter resolution data demonstrates that high and very-high resolution imaging is possible on a smaller satellite platform.

On the ground, image processing technology, such as artificial intelligence and machine learning, is lowering the time and cost of analyzing satellite imagery. This is of growing importance especially to the commodity trading, insurance, and reinsurance sectors, which are finding increasing utility in satellite data. As a result, NSR forecasts that the revenues from downstream SAR services, i.e. Information Products & Big Data Analytics, will exceed $1B in annual revenue by 2028, growing at a combined CAGR of 13.2%.

Bottom Line

The SAR market opportunity is growing. Satellite manufacturing trends are allowing for smaller and cheaper platforms, lowering the investment requirement and barrier to entry. Coupled with rising technological standards for SAR imagery processing, the demand for and utility of SAR data is growing and diversifying. However, challenges will remain, and the field ahead will not be smooth.

Harvesting the market opportunity will require more than simply building the technology. Testing of SAR sensor technology on aerial platforms prior to launch will prove very useful in reducing later costs and noise issues. Current and prospective customers will require education on the utility of the imagery, and data pipelines must be developed to best meet the needs of analytics players. As always, success ahead will require players to vigilantly investigate every opportunity and challenge, or as with today’s theme, every trick or treat.