Navigating the Satcom Connected Car

NSR previously identified the pivot of Land Mobile from narrowband revenues to broadband revenues. With massive bandwidth requirements (and potentially terabytes of data) due to highly sophisticated software systems, Connected Cars are one component of this new revenue growth, and with a huge addressable market, it’s no wonder satellite operators, ground equipment manufacturers and service providers are all keen to enter the fray and carve out a piece for themselves. After all, with tens of millions of cars sold per year, penetration into a small percentage of cars sold would lead to enormous revenues, right? The reality isn’t so simple, with challenging use cases, pricing issues, and installation problems all creating barriers to widespread implementation. How should companies adapt to Connected Car realities?

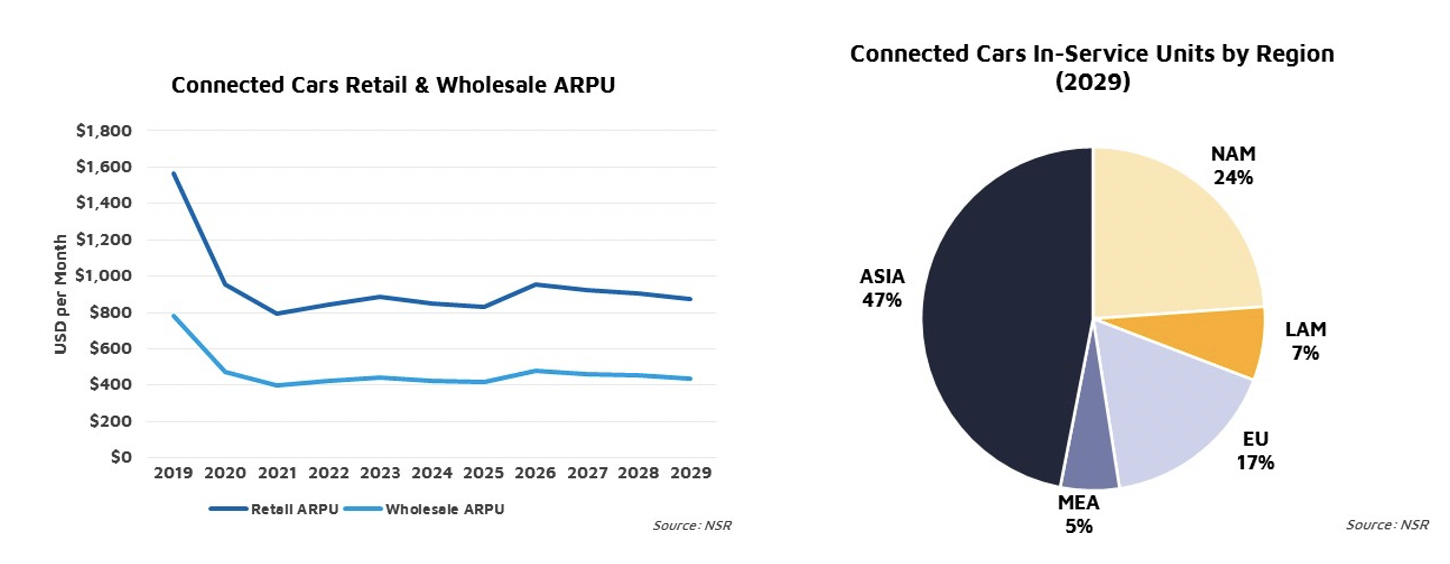

NSR’s recently published Land Mobile via Satellite, 8th Edition report, found the broadband Connected Car market (excluding connected buses and trains) will reach over $1 billion in 2029, up from a negligible amount today.

Revenues generated are mostly from first responder type vehicles – fire services, ambulances and police. Even in places like Japan, where there is significant terrestrial connectivity, emergency responders are actively keen to install satellite connectivity to increase reliability and reach. Luxury vehicles will also be expected to incorporate satellite connectivity in some models after 2025/2026, once vehicle designs incorporating a flat panel antenna are locked in in the near future.

However, with automotive market research company Jato identifying that in 2018, 86 million cars were sold in the top 54 world markets, NSR expects a penetration rate, even in 2029, to be well below 1%. Substantial new revenues will be generated from this relative niche; however, NSR is not expecting further penetration of the consumer market given the number of challenges more broadly.

High(er) Growth Challenges

- For consumers, there isn’t yet a key must-have application that demands connectivity 100% of the time. Connected Car use cases to date are solved via terrestrial means, derived through a third party device such as a smartphone, or are simply unconnected, and so far, there is not a real pressing problem that requires solving through satellite.

- Safety and emergency calling does not require a broadband connection and could be supported by a store and forward type L-band solution, or even a nanosatellite terminal – much like Europe’s terrestrial eCall service.

- Getting ARPUs down to terrestrial network pricing (or slightly above) will be challenging – as it risks cannibalizing pricing in far more lucrative markets – COTP, connected trains, buses, maritime and aeronautical markets. Starting in 2017, OnStar has offered a 4G LTE unlimited data package for $20 per month. While pricing doesn’t need to get quite this low even for a download limited package, anything higher than $50 per month will severely limit the number of private cars with satellite connectivity.

Given these challenges, it will be the first responder and ‘professional vehicles’ that must be targeted to have a shot of success.

Kymeta’s recently announced (but yet to be released) u8 terminal and service by comparison, will cost subscribers a total of $999 per month (terminal included) with a 36-month contract. This is expected to see some traction in the market, in addition to other enterprise and government/military applications; however, in no way can this represent a mass market product, especially at the moment on GEO satellites. The ability to connect to LEO-HTS constellations in the future is critical to spur usage on land mobility, given the line of sight issues with GEO services on highways and urban areas. Further, LEO-HTS Ka-band connectivity must be added to achieve the levels of penetration that NSR forecasts given the development of this frequency band by constellations. Perhaps the $85 million funding round led by Bill Gates will complete this ecosystem?

However, having the technology, which is continuing to improve and match the connected car use case, is only one part of the equation. Companies such as Kymeta will need to work with car manufacturers to become a service provider to end users – much the way GM’s OnStar service is today, and deals will need to be established across major territories – United States, Canada and European Union. Kymeta’s recent acquisition of Lepton Global Solutions, indicates the company’s interest in doing this. With the land mobile market generally underdeveloped when it comes to broadband satellite communications today, Kymeta found themselves having to develop the service provisioning or acquiring the capacity to close the deal on their terminal. However, NSR believes this deal will only be relevant to enterprise and government/military users, as there remain too many barriers in other markets.

Another company, Geely, announced a new constellation targeting connected vehicles. Geely plans to cut through the value chain and establish vertically connected connectivity chain in alignment with its own car manufacturing – in effect, becoming a service provider. This will greatly simplify implementation of the connected car and will result in an earlier product for end users. However, the cost of such a launch will be huge, and will require selling capacity to other car manufacturers, as well as to other applications to achieve a return on investment. Given Geely is based in Zhejiang, China, political considerations will also need to be considered for broader geographical penetration.

Bottom Line

Given the challenges of the broadband Connected Car market, satellite companies trying to target this market will need to be crystal clear about their objectives. Before autonomous car sales become widespread, targeting only the highest value customers is a must (the rest will use terrestrial only networks, if any), and be complete with an end-to-end service platform. Attempting to target the broad consumer market will only waste years of effort, with a platform with mismatched consumer technology rather than focused enterprise and first responder features, and a go-to-market strategy to match.