Non-GEO Satcom- From Transition to Affirmation

The Non-GEO satcom market has been highly speculative over the past decade, especially with the upcoming constellations – Starlink, Kuiper, Telesat, OneWeb and others. But in 2020, against COVID-19 odds, the segment has transitioned to a significant level of affirmation with multiple players achieving key milestones with their developments and contract awards. Although there have been delays, Chapter-11 and market exits owing to the challenges to subsequently raise funding for the program, such as Leosat market exit and OneWeb Chapter-11 filing, the overall market vectored towards market positivity. The key milestones improving the picture for Non-GEO markets in 2020 include:

- SpaceX opening Starlink’s public beta-testing with 900+ satellites in orbit at $499 equipment price and $99 per month service cost. The offered network to the beta-testers could achieve ~100 Mbps speed and ~20 millisecond latency. NSR expects the bandwidth and equipment price likely to be revised once the service is rolled-out commercially. Also, subsidies over equipment pricing are likely to be key for end-user affordability for the next 2-3 years at the minimum.

- SpaceX secured $885.5 million broadband subsidy under the U.S. Rural Digital Development Fund (RDOF) in the Phase-1 auction. The subsidy will be paid in installments spread across 10 years. Under this funding, SpaceX will provide broadband connectivity, with ~100/20 Mbps bandwidth, to 643,000 sites/subscribers in 35 states.

- Canadian Government signs $600 million (CAD) agreement with Telesat for affordable broadband connectivity using LEO constellation, to remote and rural areas.

- OneWeb emerged out of bankruptcy with new investments from the UK government and Bharti Global. Additional $1 billion is invested in the company to offer broadband services using the LEO Constellation of 650 satellites.

- Amazon disclosed the design of its phased array antenna for the project Kuiper. The key features are maximum speeds up to 400 Mbps and antenna size close to 12-inch in diameter. The company intends to make this antenna affordable to broadband access users with the smaller size and bulk production.

These key advancements are likely to set-up a pace for Non-GEO markets, especially in the fixed VSAT segment, driving both service and equipment revenues in the mid and long term. So, what is the estimated quantum of impact?

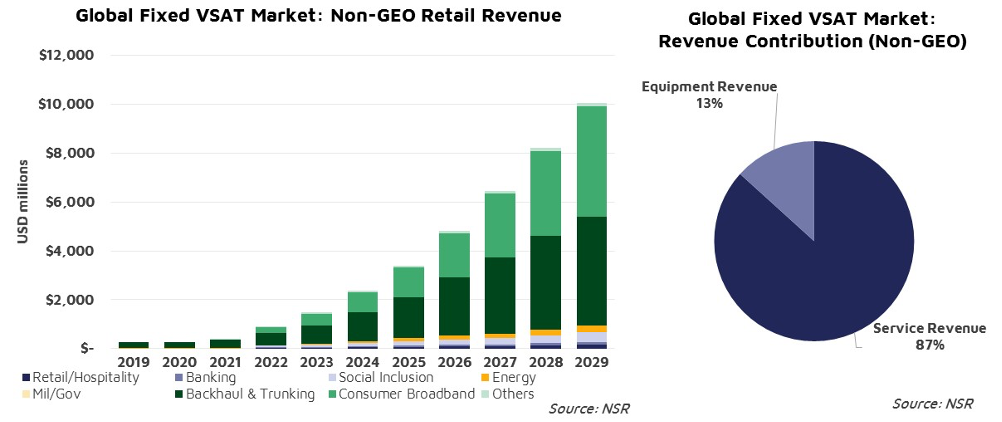

According to the recently published, NSR’s VSAT and Broadband Satellite Markets – 19th Edition report, the Non-GEO retail revenue (service + equipment) is forecasted to aggregate to $38.6 Billion at 44.3% CAGR during 2019-2029. Major growth acceleration is expected during 2022-2029, with 11x retail revenue growth, primarily driven by the roll-out of consumer broadband services and 5G backhaul demand. The Backhaul & Trunking and Consumer Broadband segments are forecasted to contribute 88% of the cumulative forecasted revenue. Consumer Broadband markets will witness maximum growth post 2022 with >50% CAGR, driven by the massive addressable market and government subsidies for rural connectivity. Among typical VSAT enterprise users – Retail/Hospitality, Banking and Energy segments – the Energy segment is expected to witness increased number of new installations and migration to Non-GEO services. In addition, given higher ARPUs, the segment size is forecasted to grow to $255+ million retail revenues by 2029. Comparing service and equipment revenues, service revenues with increasing bandwidth demand per site and recurring revenue – 87% of total retail revenues will be from Services. However, equipment pricing will remain key for penetration of non-GEO services, especially in price sensitive regions and applications.

Bottom Line

The Non-GEO Satcom market is transitioning from the speculation phase to the affirmation phase given the ongoing industry developments and new contracts. 2021 & 2022 will be key as the segment progresses towards service rollouts in the larger opportunity markets such as consumer broadband. In the near term, the government subsidies will be the major driver for the service penetration as the industry is still 2-3 years away (or maybe more) from achieving an affordable and competitive commercial price point for phased array antenna, which is around $300-$500. For example, $885.5 million broadband subsidy to SpaceX for connecting 643,000 users – approximately translates to $1,377 per site/user will be a major allowance for the service provider’s planned implementations. And similarly, for Telesat with $600 million (CAD) subsidies for the rural connectivity in Canada. It is worth noting that currently, the key developments are focused on North American region. However, NSR estimates that Non-GEO services in the Fixed VSAT & Broadband markets will gradually penetrate to other developing regions such as LAM, MEA & ASIA, either with new subsidies by governments in these regions or service providers offsetting equipment pricing in the monthly subscription packages. The rate of service penetration in these regions will continue to remain a function of pace at which the industry achieves a competitive market pricing for Non-GEO equipment and services.

Overall, NSR remains positive on Non-GEO-HTS market growth, achieving $38.6 Billion in fixed VSAT revenues during the 2019-2029 period.