Satellite Big Data: An Evolving Ecosystem

The Satellite Big Data market is still in its infancy, with the landscape of players ever evolving. The COVID-19 pandemic threw geospatial applications into the spotlight this past year, when most of the world’s workforce went remote, and multiple industries looked towards digitizing their operations. Moreover, geospatial analytics in environmental and pandemic monitoring enjoyed a short-lived boost when the airlines, shipping and all kinds of travel industries basically went to a standstill, driving interest for analytics across many vertical segments.

Map-based information products and geospatial platforms have been in existence for a long time, spearheaded by powerhouses such as ESRI, and the rise of visualization tools that leverage GIS, WebGL and other frameworks to present derived insights in an easily digestible manner.

Growth & Fragmentation

While the mainstay of the satellite “data” industry focused primarily on data feeds, the value of insights derived from pixels and bits has gained more importance over the years. Cloud computing has eased barriers to entry in this market, and customer adoption has increased. Leveraging services from cloud service providers and other major tech platforms for automation and machine learning tools combined with geospatial know-how has led to the growth of a highly fragmented downstream analytics market.

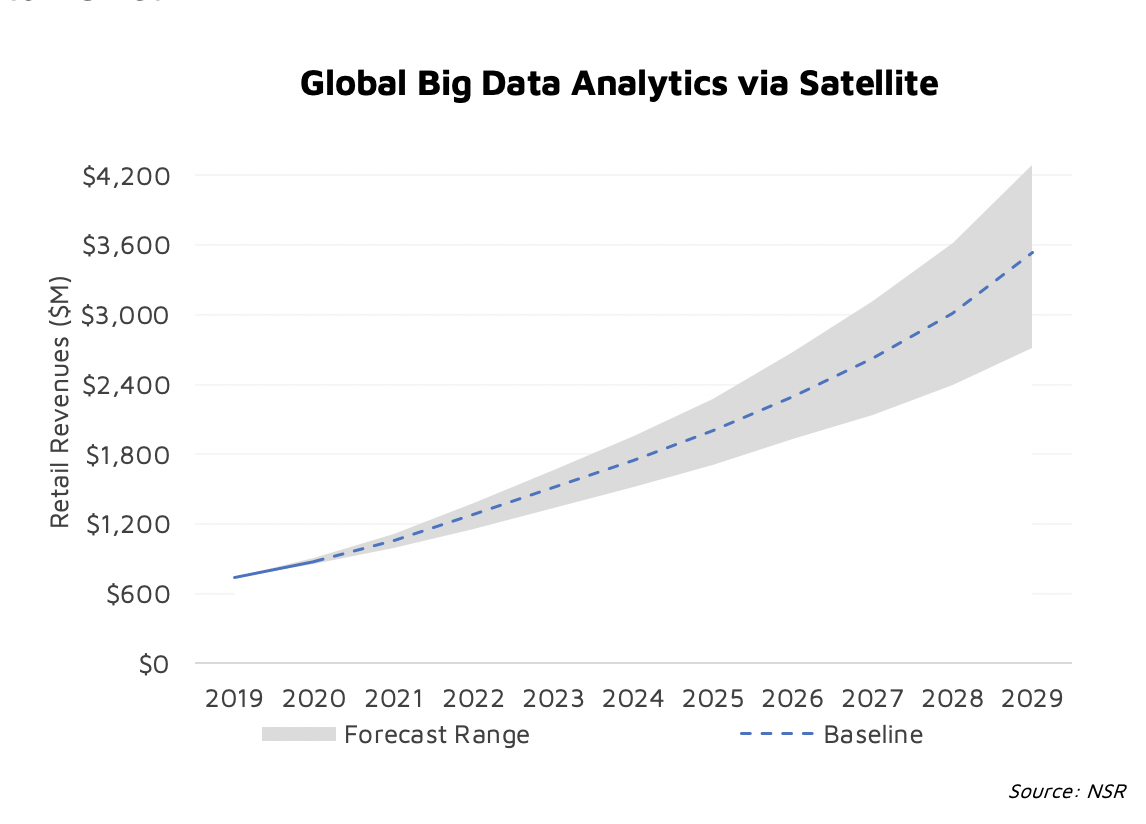

NSR’s Big Data Analytics via Satellite, 4th Edition market research report delves into the dynamics of this change and identifies some of the largest and fastest growing verticals as far as Satellite Big Data is concerned. Unsurprisingly, government-related use cases lead the way, alongside transportation as the largest users of satellite-based data analytics solutions. The entire market is expected to drive upwards of $20.7 billion in cumulative revenues over the next decade, and this is limited primarily to solutions built on top of satellite imagery and satellite connected M2M/IoT sensors alone.

Bringing It All Together

Vertical expertise, machine learning, and the cloud computing stack are three key components that enable the solution delivery process. Each vertical, whether it is Transportation, Living Resources or Energy, has its own specific types of distribution networks and market ecosystem. There has traditionally been no “one stop shop” solution that could cater to all kinds of customers across verticals.

This has most recently given rise to a middle layer of platforms in the form of satellite data and analytics aggregators/marketplaces, with players such as UP42, Arlula and Skywatch. In addition to these is the entry of well-stablished platforms such as those offered by AWS and Microsoft Azure, which are poised to use their new business units to further solidify their stake in the satellite data market.

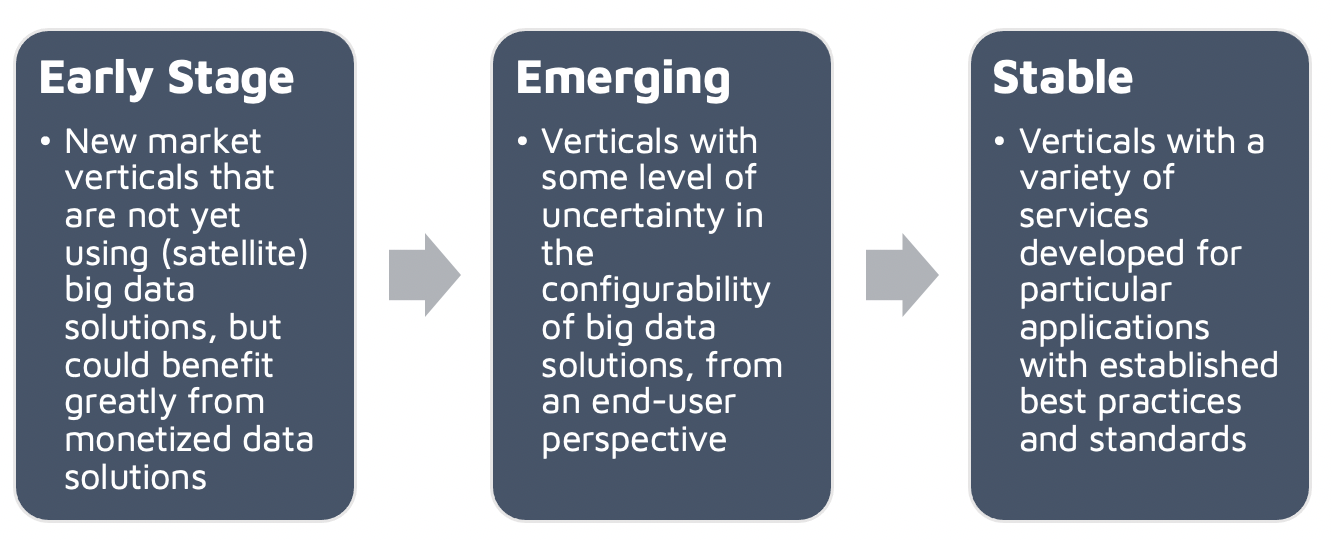

The success of this layer will be a key factor in determining the impact of Satellite Big Data in capturing the addressable market from the Early Stage and Emerging vertical segments, as shown in the figure. The Services vertical, is an Emerging segment that promises greatest gains, as the larger financial industry looks toward deep tech and business innovations to gain competitive advantages. Growing at a high 32% CAGR over the next decade, funding within the Services vertical is abundant, especially where securities and financial instruments are concerned.

The emergence of non-imagery satellite data and derived products is expected to provide yet another growth axis to this market. Radio occultation, greenhouse gas emissions and RF monitoring present novel challenges when it comes to downstream services, and readying ground processing algorithms for data fusion across such myriad datasets will be the next bottleneck, if the case for Satellite Big Data solutions is to be made. Add to this the complexity of dealing with ingesting Satellite Big Data “on-demand” into existing data processing pipelines, and the problem becomes non-trivial.

The Bottom Line

Demand for satellite data analytics, be it Earth Observation, communication or location related information, continues to rise across different verticals, giving rise to newer business models as the satellite data analytics value chain expands. The development of standardized, efficient service offerings and business models at different tiers will ensure the Satellite Big Data market is well-positioned to capture the addressable revenue opportunity from new and emerging vertical markets.