The Future of Satellite-Based Earth Observation

As we start a new decade, now is the perfect time to consider the future of the satellite industry, starting with the Earth Observation (EO) business. Traditionally, the EO business mostly consisted of a few satellite operators catering optical imagery to government and military customers. However, technological improvements in every sector have greatly expanded the business. Satellites and payloads have been miniaturized, rocket launches have become more available, and the volume and capacity for storing and processing imagery has ushered in the era of Big Data analytics.

The market ecosystem has diversified greatly, and focus has begun shifting downstream. New investments, companies, and platforms are announced every day, with the promise of making EO data cheaper and more accessible.

Will these trends continue? How does the future of satellite-based Earth Observation look over the next decade?

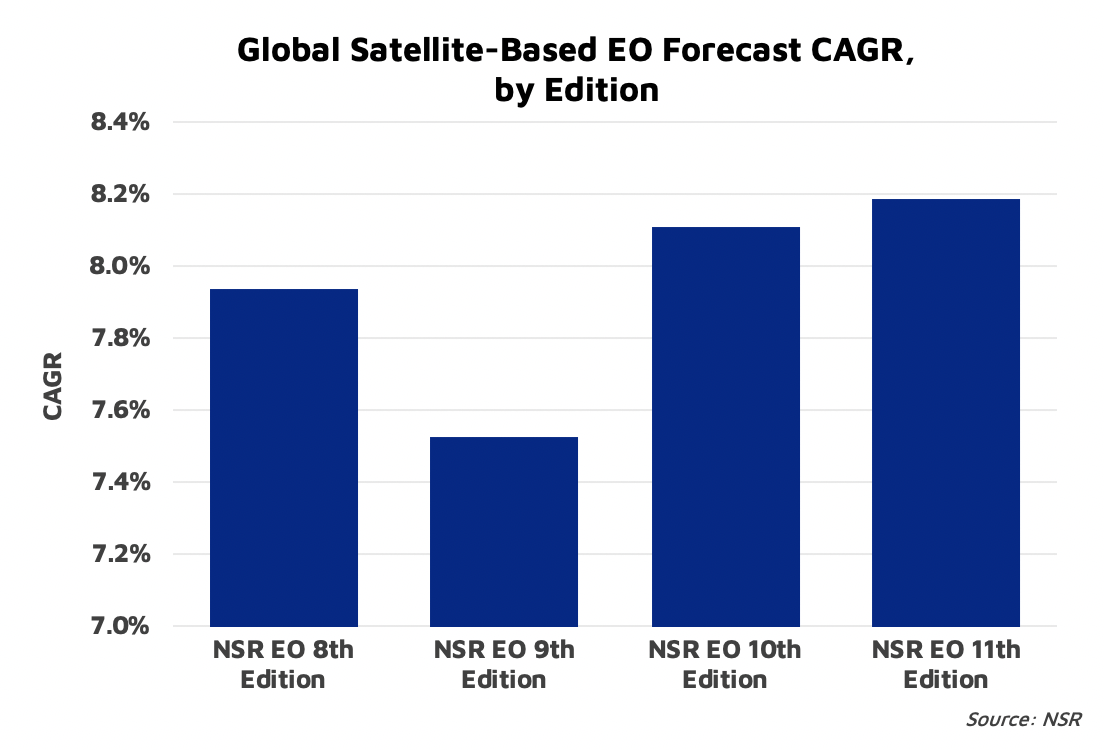

NSR’s Satellite-Based Earth Observation, 11th Edition report forecasts global annual revenues from the sale of satellite EO data and derived products to grow from over $3.3B last year to $7.2B by 2028, at a CAGR of 8.2%. This rate of growth, itself, has been rising slowly over NSR forecasts, driven by the trends noted earlier. However, market growth has shifted, back and forth between the rising commoditization and value of satellite data. Closer examination of EO supply and demand reveals a market that is sure to grow, but not without challenges.

Supply

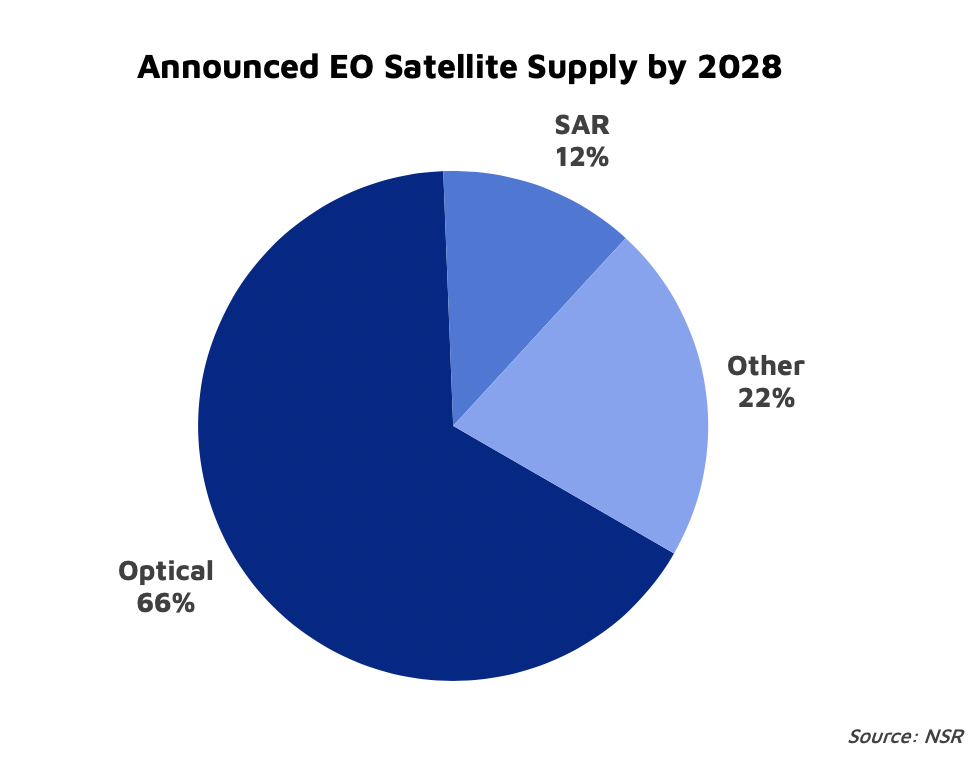

Over 1,100 satellites for commercial EO have been announced to launch by 2028. Optical continues to lead, but disruption comes primarily from the “Others” category. Consisting of non-established datatypes, NSR has seen investment and potential growing in recent years. Persistence and a diversifying market are the key drivers behind EO satellite supply. Constellations of satellites are planned to provide global monitoring, and new players are seeking ways to monetize innovative datatypes, such as greenhouse gas emissions and radio occultation.

However, not all satellites are expected to launch, and the threat of integration looms. Maxar’s merger of Digital Globe and MDA drove the company to 85% of North American market share in 2018, and while there remain challenges here, the pressure of integration will continue. NSR expects the future of EO to bring new players and products, but for constellations to severely pressure smaller fleets, and integration to consolidate the efforts of many players.

Demand

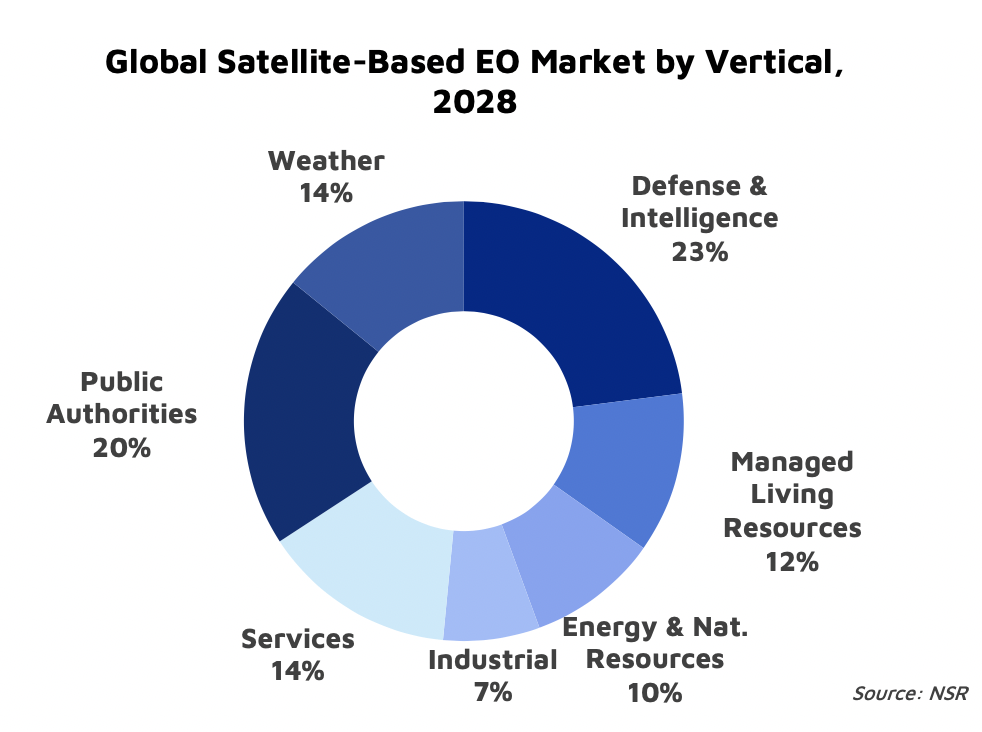

Government & Military (Gov/Mil) have been, and will remain, the largest customers. Responsible for over 43% of annual revenues throughout the forecast, Gov/Mil drives the market through large budgets, established relationships, and a growing need for both high-resolution imagery and actionable analytics. Furthermore, government support has been responsible, time and again, for encouraging new opportunities in this market.

However, said opportunities are finding avenues outside of Gov/Mil, especially downstream. The Services vertical, mainly financial and insurance, is forecast to generate more revenues from Big Data analytics in 2028 than government and military combined. This vertical represents the mass market, where access to data must be easy and inexpensive, and value shifts toward the industrial insights derived from it. However, while the threat of satellite data commoditization and market transition to Big Data remains, NSR has seen these trends slow in its recent forecast, owing to the persisting high value of satellite data, and the challenges of scalable analytics. In short, access and analytics will continue to grow, diversification of products and demand will continue, but high value imagery and deeper Gov/Mil pockets will drive demand.

Bottom Line

The future of the EO business looks bright, with revenues growing in all verticals and regions, driven by strong demand and technology rising to meet and innovate on the supply of satellite data. Technology is enabling diversification, allowing for more players, more products, growing ease and ubiquity of access, and more revenues. Given the established nature of the market, the main challenge ahead lies not in deriving revenue from a stifled market, but rather establishing a clear path of monetization from supply to demand, delivering products and generating revenues, rather than simply demonstrating a technology. The EO market is ready for disruption and innovation, but not at a breakneck pace, and players must be ready for the entrenched and persistent trends of competition and customer demand.