“Whale-Sized” Disruption by Starlink in Maritime SATCOM?

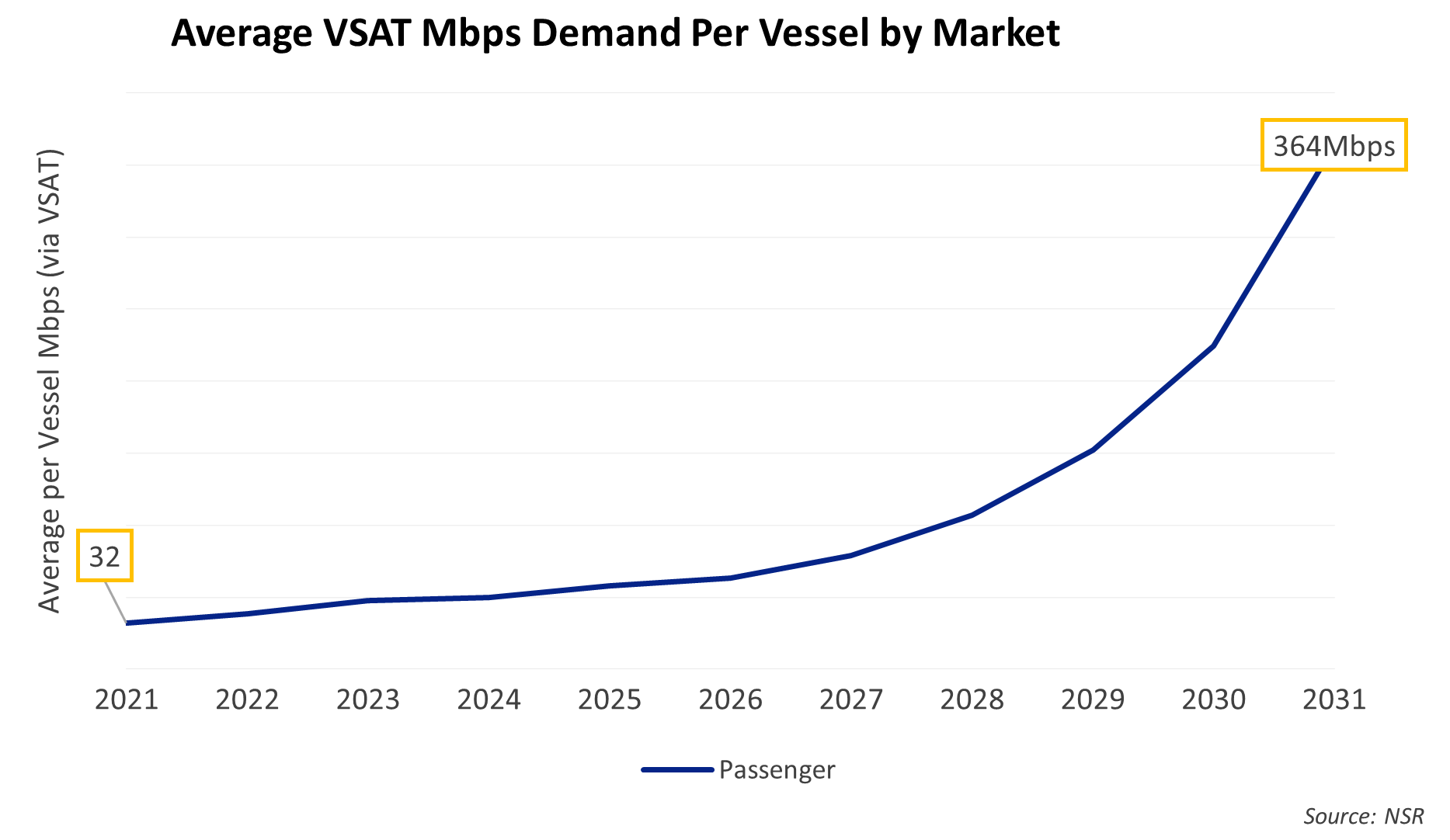

There should be little doubt that ocean cruise ships, ferries, and river ships require a lot of bandwidth. NSR projects that the average passenger ship will increase from an average of 32 Mbps per vessel in 2021 to upwards of 364 Mbps on average of throughput demand by 2031 in its latest Maritime SATCOM Markets, 10th Edition report.

Many ships, especially cruise ships like those owned by Royal Caribbean which recently announced will use Starlink services onboard, will have significantly higher provisioning rates. Driven by the rapid ‘return to cruising’ and the fundamental shift in passenger data demands, the cruise industry faces an almost insatiable demand for connectivity. Starlink, with near global coverage today and plans for full global coverage soon, focusing on the cruise sector came as no surprise. It was not an “if”, but a “when.” Royal Caribbean Group as the end-user to launch these services specifically, should come as even less of a surprise to the satellite communications sector. In short, the ‘first customers’ for Non-GEO connectivity in the maritime sector are amongst the highest-end vessels afloat.

In 2012 the cruise industry was another ‘early adopter’ of a radically disruptive satellite communications service. This solution promised higher throughput with much lower latency via a network of satellites that were also not in geostationary orbit, from a company that had almost no history as a maritime connectivity provider. That was called O3b. Royal Caribbean Cruises was that partner. The ‘real difference’ between then and now? While the 2012 announcement only mentioned the at-the-time largest cruise ship in the world the Oasis of the Seas, the August 2022 Royal Caribbean Group announcement is for providing coverage across the entire fleet of 64 vessels. That is not only an acknowledgement of the disruptive capabilities of Non-GEO connectivity, but a significant bet on Starlink’s capabilities by Royal Caribbean Group.

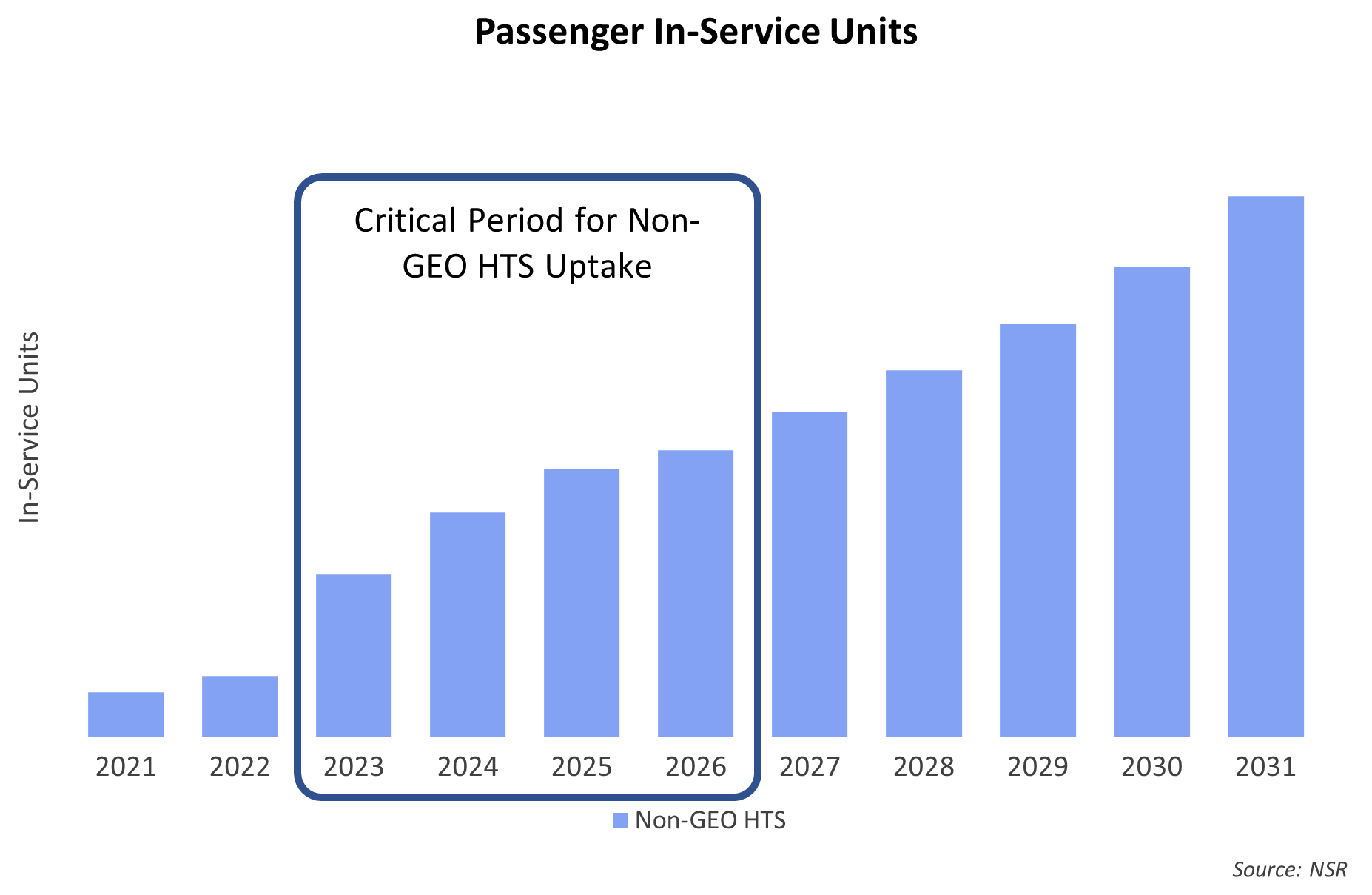

Those details are all less important however, than what it means to the ‘rest of the maritime connectivity value-chain’. In NSR’s Maritime SATCOM Markets, 10th Edition report, our assumption was a slow roll-out of Starlink Maritime connectivity solutions amongst high-end customers, with 2023 – 2026 being the ‘critical time period’ to undergo the usual lengthy demonstration to contract RFP period within the maritime markets. Should the full Royal fleet be rolled out by the end of 2023, it will accelerate Non-GEO HTS uptake within the passenger segment by 2 to 3 years – more vessels connected, greater bandwidth demand, and higher revenue generation. The question – will Starlink wins translate into more revenues across the industry, or just shifting in spending from one provider to another?

Should it turn out to be true that Starlink will replace the existing Non-GEO service from SES, this will be the maritime version of what consumer broadband players are already feeling – Starlink is a viable competitive solution. However, maritime vessels are not a ‘one-pipe’ solution and instead rely on a complex network of layered connectivity to ensure optimal guest connectivity and connectivity uptime. That difference is key to understanding if this is a Blue Whale, Orca or a Narwhal-sized disruption.

To quantify how NSR see’s these whale-classed scenarios:

- A Blue Whale Disruption – Starlink completely replaces all existing SES O3b/mPower services and deploys to other Non-O3b vessels in the Royal Fleet. It further reduces or eliminates GEO services.

- An Orca-level – Starlink replaces most-to-all O3b services and deploys to other Non-O3b vessels. It does not replace GEO utilization but might reduce it.

- A Narwal Event – Starlink is used alongside all existing services. It likely reduces future growth on incumbent services by capturing ‘passenger+crew demand growth’. Existing solutions focus on “operational data” growth.

What is less clear is just how disruptive this is downstream into the service provider layer – a dilemma NSR discussed as far back as 2017. Just as maritime vessels typical use multiple connectivity pathways, high-end maritime customers require more service and support than consumer broadband markets. Everything from managing onboard wireless access points to terrestrial IP traffic routing to flying service technicians across the world are ‘in-scope’ for Maritime service providers. How many of these ‘downstream services’ will Starlink do? What will be the relationship between end-user, a ‘service provider’, and Starlink? Can Service Providers fully move from ‘Mbps providers’ to ‘bit monetization’ strategies? In short, disruptive technologies in the maritime sector pose the same set of questions today as in 2017 – and still further questions for who wins in the next 5 to 10 years.

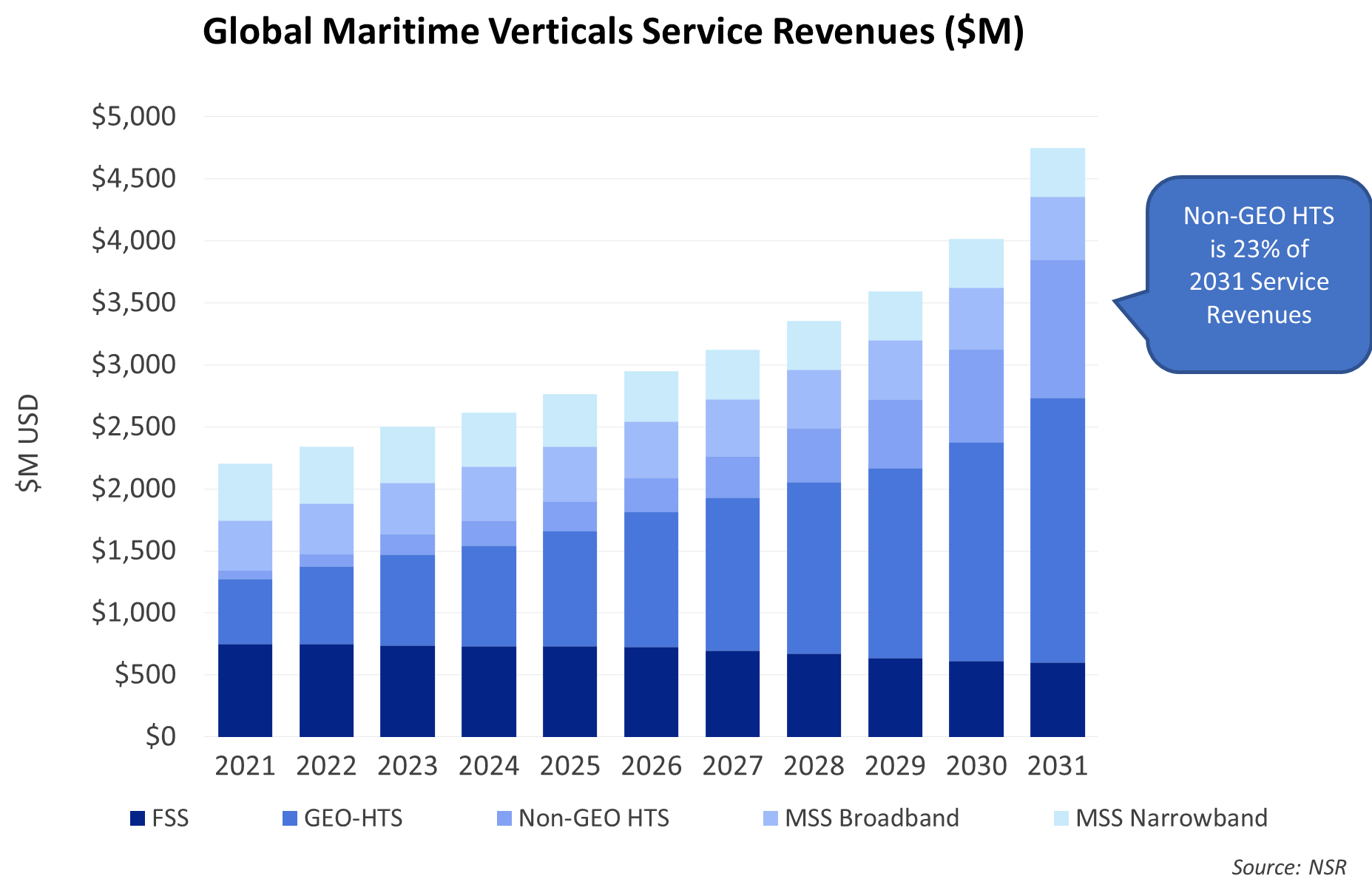

All is not lost to this potential killer whale – NSR’s Maritime SATCOM markets, 10th Edition study still finds that most revenues will come from GEO-based services, with only 23% of service revenues by 2031 derived from Non-GEO HTS players such as SES mPower, Starlink, OneWeb – and other potential entrants. Service and Support play key roles in meeting the full-needs of maritime customers, and redundancy is part of the ethos of maritime end-users. Additional downstream value-added services such as onboard IT monitoring/support, crew connectivity management, etc. – all ‘bit monetization strategies’ – will become key to building and retain customers. “Big pipes” alone are unlikely to satisfy the complex set of requirements maritime customers are looking to solve.

Bottom Line

While more details continue to emerge, NSR views the Starlink + Royal Caribbean Group as a likely Orca-level event. There is likely to be a period of multi-illumination amongst many GEO and Non-GEO services as Starlink is rolled-out across the fleet and Starlink is unlikely to ‘do everything onboard’ (and cruise companies are unlikely to pick-up these requirements immediately). In the longer term, should this go well, Starlink will likely capture more onboard traffic. For Service Providers those adopting ‘bit monetization’ strategies including software defined networks, value-added services, and superior service/support will have a winning chance of countering these new and emerging constellations.