A Slow(er) Wave of Recovery for Maritime SATCOM Markets

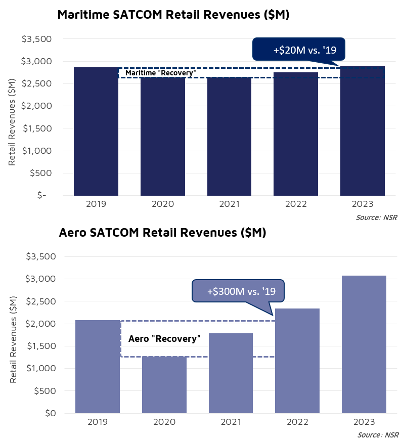

While there is no doubt that COVID-19 has impacted the Maritime market, the “COVID-dip” is significantly less pronounced for Maritime than Aeronautical SATCOM markets. Unlike the Aeronautical sector, which my colleague Vivek discussed last week, vessels continue to have crew aboard for the most part, and in a many instances continue to operate at sea. As such, with fewer “sites” idled, the revenue dip in 2020 is expected to be significantly shallower for the Maritime SATCOM sector compared to Aero. However, what we do expect to see is a slower ‘bounce’ in the recovery phase for Maritime.

Looking at data from NSR’s Maritime SATCOM Markets, 8th Edition, and NSR’s Aeronautical SATCOM Markets, 8th Edition Reports, it’s easy to spot the trends – a slower, sustained dip for Maritime Markets, and a sharp dip for Aeronautical Markets followed by a stronger/quicker recovery.

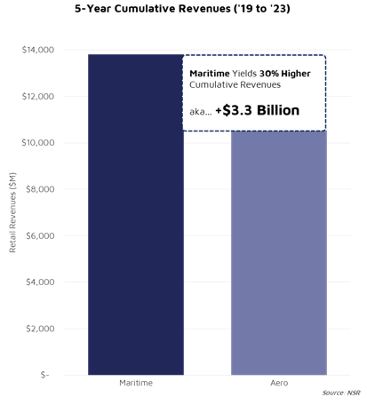

Key players have already noted as much in their recent earnings releases. Inmarsat in its most recent earnings calls have called Maritime one of its more “resistant markets”, KVH noted their Q1 2020 airtime revenues were up 5% over the prior year, and other players have reported that at least the first quarter of 2020 had signs of improvement over previous years. What is not as easy to spot – Maritime SATCOM Markets will yield higher cumulative revenues over the next five years than Aero.

Maritime Markets will yield 30% more in cumulative retail revenues compared to Aeronautical over the next five years (2019 to 2023), or, $3.3 Billion more in retail revenues. While Q2 and Q3 2020 are where we expect to see the most impact from COVID-19, compared to the uncertainty around passenger air transport, it seems as though Maritime is weathering the COVID storm better than Aero. So, why the slower recovery if some of the fundamentals for Maritime Markets appear to be on ‘solid ground’?

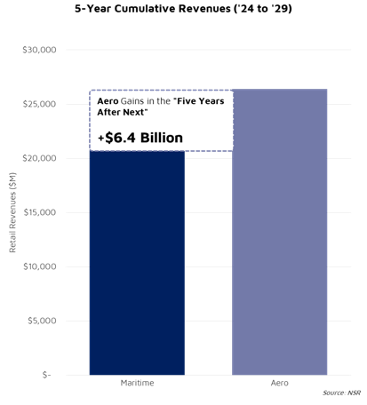

Simply, unlike Aero which can quickly ground planes and ‘right size’ itself to changing market conditions, the Maritime sector is much slower to adapt to changing micro and macro-economic conditions. Fuel prices are cheaper, which makes it more economical to run older ships. Scrapping markets are facing challenges due to closed borders, and shipyards are facing their own challenges delivering newbuilds. For the Passenger Maritime segment, that means launching newbuilds that are ‘social-distanced’ vessels take time, if new vessels are even required. The Offshore segment is facing unstable crude pricing – and, those sites take an even longer amount of time to shut down as we saw in the last pricing crisis. However, these near-term strengths also limit the future revenue growth for Maritime SATCOM Markets as the ‘five years after next’ strongly favor the Aeronautical sector – to the tune of $6.4 Billion in Retail Revenues.

As Vivek explains in his piece last week, an emerging class of “Free” services enable strong growth prospects in the aero markets. The transformation of Maritime MSS BB vessels to VSAT vessels continues, but that is not a ‘N-th level increase’ in revenues – rather a slower migration towards higher per-vessel ARPU rates and reallocation of connectivity revenues from MSS players to VSAT. Significant numbers of under and un-connected vessels will adopt satellite solutions over the next ten years, with another large number of newbuilds and existing MSS customers adopting or migrating towards VSAT-based solutions. However, just as the inertia of maturity will enable the maritime satcom sector to ride out the near-term ‘COVID-dip’ better than its aero counterparts, it will remain on the slow(er) path to revenue growth. Overall, the Maritime Markets will yield “only” $34.5B in cumulative revenues from 2019 to 2029 compared to the Aero markets $36.9B.

Bottom Line

Social distancing and a ‘return to normal’ are the buzzwords today. Already, Ocean and River Cruise operators are making announcements of a near-term resumption of cruises – many with fewer passengers and crew aboard, and focused on shorter, out/back trips rather than extensive country-hopping itineraries found in 2019. For Merchant and other segments, ships continue to face a changing macro-economic environment – yet, still have crew aboard. Overall, in the face of an uncertain future, the Maritime SATCOM Markets seems to be weathering the storm slightly better than other Mobility SATCOM Segments, yet ‘slow and steady’ remains the name of the game in the ‘five years after next’.