EO Markets Prove Resilient

This has been a very hard year for a lot of industries, including the satellite industry. From grounded flights and shored-up cruises, bankruptcies and layoffs, COVID-19 has strongly impacted the entire satellite industry. However, while most of the market is experiencing a downturn, consolidation, and restructuring thanks to the pandemic, Earth Observation has demonstrated strong resiliency. In fact, in some cases, the market is growing.

Initially, experts noted an increase in tasked satellite-based data and imagery, in order to track and understand changing behavior on a global scale. Government demand has not wavered in the slightest, with agencies expressing support early and often for Earth Observation products. Finally, investment has continued, especially for EO satellite constellation development.

But is it a fluke, or a bubble? How will this sector develop as the larger satellite industry adjusts, and what is driving the business of Earth Observation?

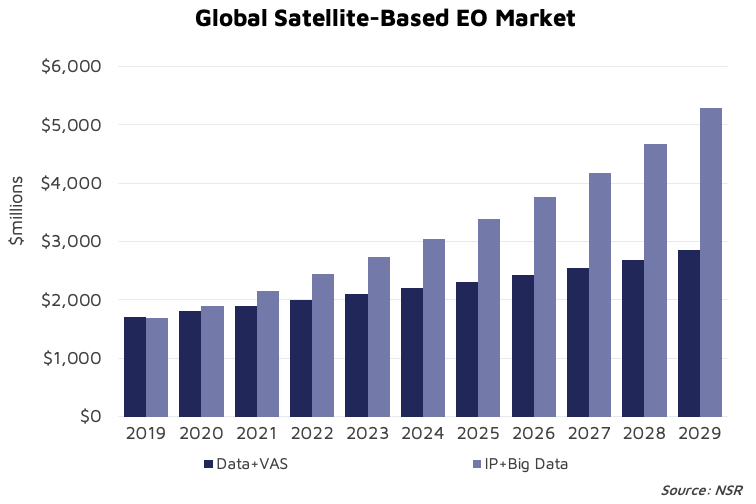

NSR’s Satellite-Based Earth Observation, 12th Edition report forecasts annual revenues to grow over $300 million in 2020, and from $3.7 to $8.1 billion by 2029, at a CAGR of 9.2%. Currently, downstream, insight-driven applications generate slightly more than the sale of imagery, as the industry has been hard at work to streamline data delivery and add value through analysis. This gap is expected to widen considerably, with Information Products & Big Data analytics earning almost twice that of Data and Value-Added processing Services by 2029.

The entire EO industry has been moving toward becoming a more efficient and competitive solution, compared with traditional terrestrial options, and has created strong momentum, which has carried it through even this year’s challenges. Through its research, NSR identified satellite constellations, persistence, and subscription models as the key driving trends behind this industry.

Constellations

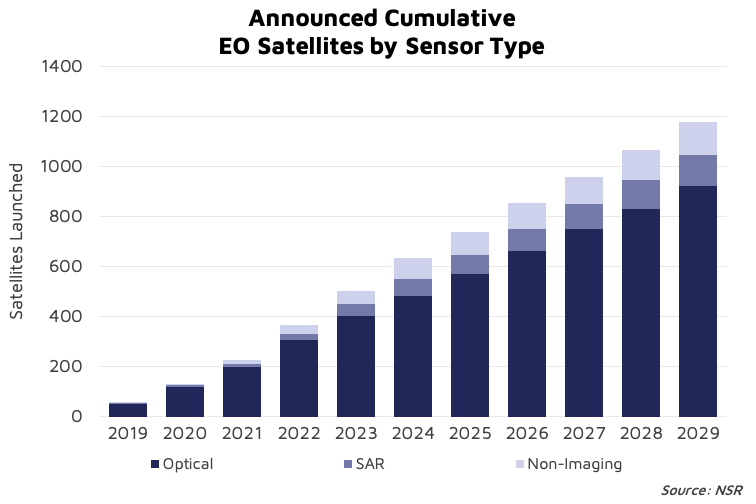

Improvements in satellite manufacturing & launch costs, cadence, and competition, alongside this industry’s inherent focus on infrastructure, continue to drive the development of constellations for EO. Currently, over 1,000 Earth Observation satellites have been announced to launch over the next 10 years, 99% of them as part of constellations, with a strong focus, 76%, on optical imagery. Since 2019, almost $500 million in investment in EO has focused on satellites, with downstream application development lagging just slightly behind. It is no secret this industry favors infrastructure, as a similar trend has been seen in the communications sector. However, while the EO opportunity is expected to grow, there is considerable competition from established players, many of whom are also planning next generation constellations. Strong use cases and strategic business plans will be vital to meeting the growing demand ahead.

Persistence Props Up

Revisit has been a strong EO driver for some time. Improvements and investment as noted above, combined with a growing need for timely data, have driven many business plans on the premise of providing higher revisit. Now, as demand is expanding to include larger coverage areas, in many cases global, revisit has combined with coverage, making persistence the key driver. From government and military applications, through disaster management, environmental and agricultural monitoring, and consumer traffic tracking, customers are seeking persistence in their Earth Observation products. This is not only driving sales, with a strong focus on volume-based purchasing agreements and platforms, but also on monitoring and analytic solutions. As such, NSR forecasts high and medium resolution imagery to be especially buoyed by this trend, responsible for 73% of global EO revenues by 2029.

Subscriptions Streamline

As a result of the drivers above, much of the effort on the ground has been focused on streamlining the satellite-to-solutions pipeline. Improvements in data storage, processing, categorization, and delivery, have continued in both dedicated centers and in the cloud. Customers are less likely to seek individual images, and more strongly favoring bulk purchasing agreements and ongoing subscriptions. However, standardization has proven a considerable challenge. Every provider features different persistence, resolution, and value-added services, which make comparison between offerings difficult, if not impossible. As a result, the majority of the industry has shifted from time-intensive, bespoke, one-off purchases of imagery to similarly-intensive purchasing via subscriptions. For these reasons, NSR’s forecasting of imagery pricing, and the growth of SAR revenues especially, remain conservative, particularly in the near-to-midterm.

Bottom Line

The resilience of the Earth Observation industry is not a temporary occurrence. While demand has been stronger recently, given the need to operate more remotely, the industry is driven by strong demand and increased capabilities both in space and on the ground.

Customers demand more coverage and persistence, not less, and constellations seek to meet that demand. As a result, the industry continues to shift toward subscription models that should prove more financially predictable and resilient, and push the development of standardized, efficient, product offerings and business models. Challenges will continue, but it will be the players who best respond to the drivers of persistence, constellations, and subscriptions who will prove resilient.