FPAs: The Key and the Barrier to Satcom Growth

The ultimate goal for satellite connectivity is to transition from what is sometimes considered as a complementary backup, to a necessary part of global communications. However, achieving this goal is not straightforward, and many non-GEO HTS Constellations projects promote themselves as essential to becoming this key part of the communications landscape. Yet their success remains uncertain, to the point of two recent exits this year alone.

Flat panel antennas (FPAs), essential for Non-GEO HTS connectivity, are considered by NSR as the terminal of tomorrow, but their success rate varies wildly, from one market to another. Given the pace of terminal development and adoption, where will we see FPAs “move the needle”?

NSR’s latest Flat Panel Satellite Antennas, 5th Edition forecasts growth of global, annually-shipped units to exceed 628,000 by 2029, at a CAGR of 54.5%. Despite harsh downturn in 2020 due to COVID-19, long development cycles, and strong demand (especially in government markets) will help the equipment market rebound In the mid-term, when constellations come online and certain challenges of terminal production scale have been overcome. Given these developments, flat panels are expected to flourish, reaching commercial land-mobile markets, and breaking into broadband.

Flat panel terminal technology has had to contend with the needs of tomorrow, and the limitations of today. Fleets, militaries, and enterprises are increasingly demanding “always-on, everywhere” connectivity, raising the pressure for multi-band, multi-orbit capable terminals, for the right price.

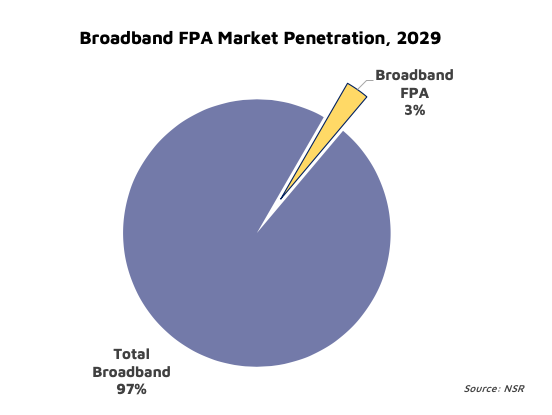

However, despite strong growth, essentially shipping 80 times more units by 2029 than in 2019, FPAs will only represent 3% of the total satellite-connected in-service market. To understand why, we need to look at the Aeronautical and Broadband markets.

Aero: Low Profile and High Demand

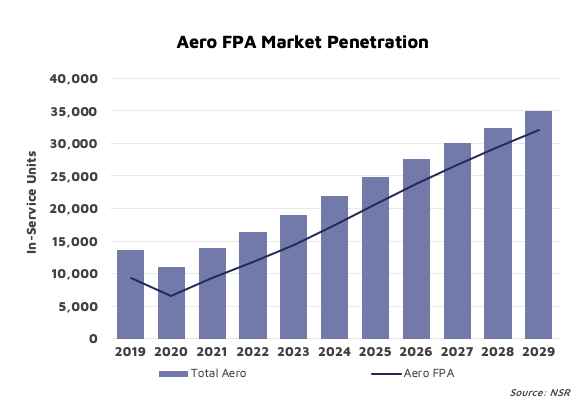

Commercial aero has long been the main driver of FPA adoption, given the necessity for a low-profile, and the strong demand for in-flight connectivity. FPAs make the most sense here, but have taken time to develop, owing to the challenging operating environment, rigorous certification process, and the increasingly competitive landscape. As of 2019, there were over 7,300 commercial aeronautical in-service units flying, cut in half by COVID-19 in 2020, but expected to rebound in 2021 and onward.

In the government sector, aircraft have been able to utilize parabolic systems for some time, especially in unmanned aerial vehicles, but there continues to be a transition to flat panel equipment. The strongest driver is in “future-proofing”, with end-users seeking equipment capable of switching between frequencies and LEO/MEO/GEO connectivity without interruption, something parabolics are incapable of, in small form factors.

With 14 out of the existing 24 FPA manufacturers today targeting these verticals, and given the high costs associated with serving the complexity inherent to this market, FPAs will be responsible for 91% of aeronautical in-service market penetration by 2029, and 83% of all FPA cumulative equipment revenues.

Broadband: Low Price and High Performance

While aero drives revenues, broadband is expected to drive volume. The addressable market for consumer and enterprise broadband is in the millions, compared with the tens of thousands of aircraft.

For many manufacturers, serving broadband markets represents the pinnacle for FPAs, moving from niche applications to widespread adoption, demonstrating a mature market and moving past challenges of scale and price.

However, while NSR’s latest report forecasts strong growth here, especially driven by Non-GEO HTS constellations, FPAs are only expected to represent 3% of consumer and enterprise in-service units by the end of the decade. The short explanation as to why is that enterprise is too performance-constricting and consumer is too price-sensitive.

Medium-to-high-end enterprise markets require over 99% connectivity, defined in their SLAs, and parabolics are very competitive here. Growth will be driven by Non-GEO, as well as an ongoing shift by FPA manufacturers to cater to this market, leading to faster technology progress. Consumer end-users, accustomed to paying less than $200 for equipment, if at all, are not likely to see a price-competitive FPA option in the next ten years. Flat panel technology is complicated, and currently produced at low scale. Recent developments from manufacturers demonstrate strong cost-cutting practices, such as a refinement in the overall architecture, or use of cheaper components, but most manufacturers are incapable of producing at the scale necessary for extremely cheap equipment. However, FPAs need not compete on price alone, and NSR has seen faster development here in recent years. As such, NSR forecasts broadband to be responsible for 91% of all FPA shipped units by 2029.

The Bottom Line

Given their necessity for Non-GEO HTS connectivity, flat panel antennas are both the key, and the barrier, to satcom market growth. The technology and competitive landscape are developing strongly, especially in aeronautical and land-mobile markets, driving revenues and introducing new applications.

However, broadband will remain an extremely challenging market for FPAs to penetrate, given very high price and performance sensitivity. Greater collaboration in the value chain has greatly improved FPA potential here in recent years, but it will take time and effort to scale up and expand its capabilities enough to compete with strongly-established, relatively inexpensive parabolic equipment.