Space for the Cloud: Data from Orbit

Cloud services ranging from IaaS and edge computing to virtualization and SaaS applications are not new to the IT industry; they have been well-known for years and are traditional concepts in most sectors. Not so in the satellite sector though, where a surge in the adoption of cloud-based technologies is underway, with established and newspace players targeting new-age business models that leverage the cloud. The fact that business agility and IT flexibility are key drivers of cloud migration in the satellite industry has been established earlier. What then, are the key underlying assumptions driving this growth and what is the revenue opportunity here?

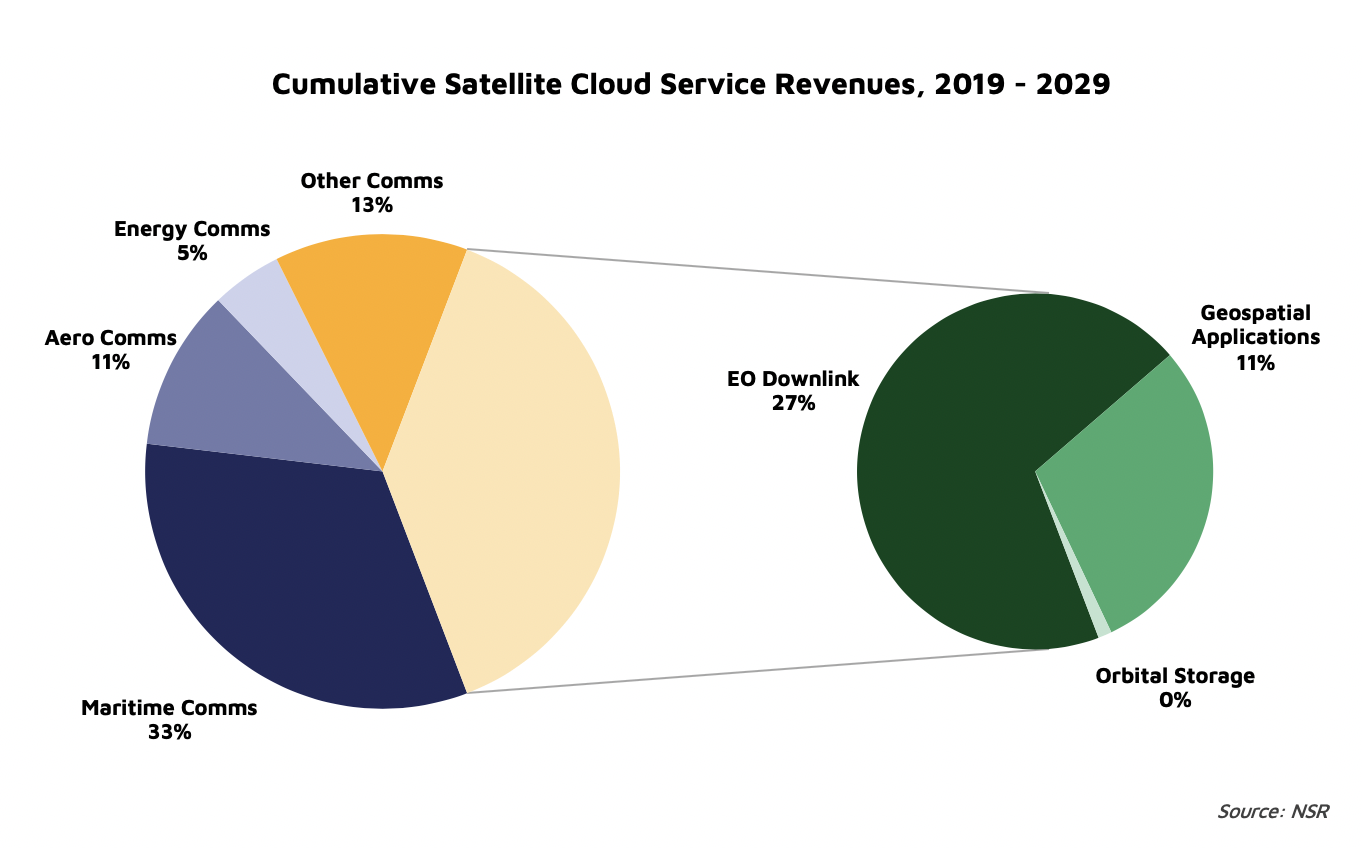

NSR’s Cloud Computing via Satellite report Is an Industry-first that dove deep into these questions and forecasts upwards of 52 Exabytes of cloud data traffic transported via satellite in 2029. The 2019 to 2029 period is expected to present an opportunity for $16 billion in cloud service revenues cumulatively.

Even before the COVID-19 pandemic, enterprise digitalization across industries was a major concern, leading to cloud migration strategies to ensure market competitiveness in a cloud-native future. The pandemic has helped to accelerate this movement, despite negatively impacting some of the same industries. Whether such businesses are partners or customers, adapting to the cloud will be essential for satellite players too, as it replaces heavy CAPEX investments with reduced OPEX, allowing them to co-operate with cloud service providers and deploy their applications much more effectively.

Communications

The maritime sector is the largest driver of cloud services via satcom, generating $5.2 billion over the next ten years. In 2019, D2IQ delivered real-time microservices to one of the largest cruise ship fleets on the open seas, while optimizing usage of the limited 300 Mb satellite connection for its guest services. More recently, Rignet’s predictive analytics offering was upgraded to a Microsoft co-sell ready status and is now optimized to run with Azure, helping customers realize exceptional operational savings. Inmarsat’s maritime (I)IoT platform provides a number of dedicated partner applications, ranging from fleet optimization to quality assurance. Passenger cruise and offshore energy data requirements are the primary drivers, with cruise passenger cloud data traffic forecast to accelerate once non-GEO HTS systems come online.

While the “high value, low volume” nature of cloud applications is not different in the Aero segment, the COVID-19 pandemic has impacted it the most with cloud service revenues in 2020 down by 38% from 2019. In the long-term however, with the influx of capacity, pricing pressures (for both equipment and services) and the gradual adoption of the free-service model for In-Flight Connectivity, the Aero segment is projected to grow to reach nearly $1.8 billion in 2029. Here too, cloud migration strategies will be a key driving factor, as in the case of Gogo’s AWS migration in 2019.

Onshore energy (land-based Oil & Gas, mining and utilities) is in transition as an industry, with most majors eyeing digitalized integrated operations. Real-time data intensive video intelligence, crew welfare applications and smart grid solutions are expected to drive cumulative revenues in this segment to nearly $800 million through the next ten years. In the post-pandemic world, the current shift to remote and automated mining is only expected to accelerate.

Data Downlink

Last month, the largest cloud service provider launched a new business segment dedicated solely to accelerate growth in the aerospace/satellite industry. No surprises here, given recent activity surrounding AWS Ground Station. This cements the arrival of a new paradigm in the satellite data downlink market, one that was up until now the forte of a few major incumbents. This evolving Ground-Station-as-a-Service market is driven by both the rise of cloud-enabled services as well as virtualized ground networks.

For the Earth Observation market, data is downlinked from satellites on the open market either to private data centers, hosted centers or directly onto the cloud of EO operators. With current trends in hyperspectral, SAR and HD video capabilities, the volume of data downlinked is expected to increase, driven by improvements in sensors and instrumentation. Despite pressures on data downlink traffic from edge compute/optical downlink technologies, NSR forecasts $4.2 billion in cloud service revenues for EO data downlink through the next ten years.

Big Data Analytics

The downstream market comprising geospatial solutions providers are cloud customers, using cloud capabilities to develop applications and platforms for satellite data end users across a variety of sectors, ranging from transportation and financial services to energy and managed living resources.

Geospatial intelligence is fast becoming a key component of traditional BI tools and big data applications. With a very diverse set of applications forming the ecosystem, the benefits of the cloud are expected to be much greater here. NSR forecasts a cumulative revenue opportunity of ~$1.8 billion through the next decade. However, scalability is a concern in this segment, as companies weigh the benefits and costs of using private/public clouds due to the sheer volume of data being stored or processed.

Orbital Infrastructure

Players in this segment essentially launch satellites as cloud service infrastructure, providing storage and compute capabilities in space. While comparatively a very nascent and emerging market, high visibility cyber-attacks from recent years (NotPetya, for instance) have spurred interest in such solutions, with potential customers willing to pay a high premium for protecting/storing their data in space-based cloud services. Next generation in-orbit processing capabilities, data security and effective partnerships will be key here. In-space cloud storage is forecast to present a revenue opportunity of nearly $22 million by 2029, growing at a high CAGR of 43% from now till then.

The Bottom Line

The cloud computing via satellite market is communications-centric, in terms of both data traffic and service revenues. This is driven largely by demand in the Maritime, Aero and Energy segments, and further by direct cloud connectivity partnerships between satcom and cloud service providers (CSP).

Additionally, virtualized ground networks (again, in partnership with CSPs) enable the “cloudification” of the EO and analytics industries, bringing value closer to the end user efficiently. Orbital storage and compute solutions further blur demarcations in the traditional satellite supply chain, effectively decoupling satellite hardware and software and thus opening up the satellite/space market to competition from the wider big data and cloud computing ecosystem. All these are helping move the cloud on its way to space.